Trinity Mirror Pension Plan has carried out a consultant review ahead of an appraisal of its defined contribution default fund, spurred by the introduction of the freedom and choice reforms.

The end of the effective requirement to buy an annuity at retirement has sparked debate about the ideal investment strategy for DC defaults, as optimising for annuity purchase is unlikely to be suitable for large numbers of retirees.

However, lack of information about likely choices is hampering progress and many schemes are waiting for further detail on member behaviour before embarking on a review.

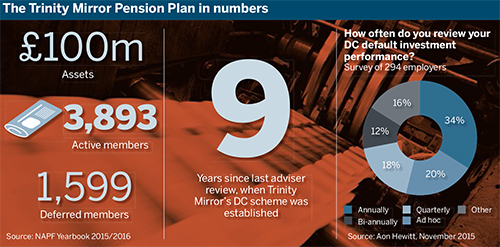

Laurie Edmans, chair of the Trinity Mirror scheme, said the scheme had not reviewed its advisers since it was first set up nine years ago.

Trustees realise it’s probably as risky not doing anything as it is doing something

John Reeve, Premier

“The results will be out soon. The main reason [was] we felt, after nine years, good governance says you should review your advisers,” he said.

“The first big job once we’ve got that is to review the default options for auto-enrolment. We’ve been deliberately slow because we need to understand how the world has or hasn’t changed.”

Edmans added that any changes would focus on the default investment strategy rather than support offered to members. The sponsor already pays £750 for independent financial advice to members leaving the scheme aged 55 or older.

Data released last week by consultancy Aon Hewitt, which surveyed 294 employers on workplace benefits, showed the majority review the investment performance of their default option at least once a year.

Source: Aon Hewitt

The study also found that 33 per cent of respondents had not changed the default option or funds within it in the last year, versus 29 per cent who had.

Annuities no longer the goal

John Reeve, senior consultant at Premier, said every DC scheme he is currently dealing with is reviewing its default.

“But it is very complicated to think about what you want to do,” he added. “It does depend on what you think members are going to do when they get to retirement. A lot of schemes are doing some kind of segmentation.”

Siemens re-engineers DC lifestyle funds towards greater growth

Siemens, one of the world's largest electrical companies, aims to give its UK defined contribution scheme members more potential for growth while reducing costs by adding a pure equity phase to its DGF-heavy lifestyle options.

For example, Reeve said, members who were likely to accrue a large pot over the course of their career might be better off not being moved out of growth assets as quickly as they would be in a traditional default fund.

Reeve added that paying for financial advice for members was becoming increasingly important with the disappearance of a fixed retirement age and the difficulties that presents for employers moving employees into retirement.

Michael Chatterton, director at professional trustee company Law Debenture, said analysis of membership in a scheme he worked with showed the existing default to be unsuitable for many.

He said: “In one case we saw nearly all members would have less than £10,000 [in their pot at retirement]. In that case we changed the default to [aim] for cash.”

Chatterton added: “You need to have a good sense of your membership.”