Five years after the introduction of rules around tendering for fiduciary management mandates, performance from many providers has been “muted” and some are struggling to recover from recent market shocks, according to a major survey of the sector.

Last year, most fiduciary managers achieved their objectives, according to Barnett Waddingham’s Fiduciary Management Investment Performance Review, published this week.

However, longer-term performance was more muted, and many managers have struggled to beat their longer-term objectives “despite equity market tailwinds”, the consultancy group said.

Trustees appointing fiduciary managers to run 20% or more of a pension scheme’s assets have been required to conduct an open tender since a Competition and Markets Authority (CMA) ruling in 2019.

Peter Daniels, partner and head of outsourced investment services at Barnett Waddingham, said: “The findings of this year’s review provide an interesting backdrop for the many pension schemes that will be formally reviewing their fiduciary management arrangements over the coming year.

“We are approaching the five-year anniversary of tender activity instigated by the CMA review. As a result, trustee boards should be reflecting on whether their provider has delivered on its promises and whether their fiduciary management arrangements remain fit for purpose.”

Manager selection ‘key’ amid wide range of return outcomes

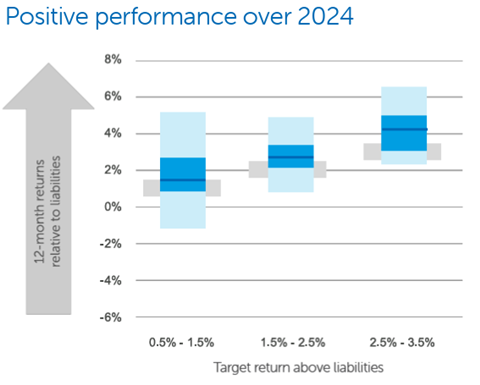

Barnett Waddingham’s report highlighted a particularly wide dispersion of returns among mandates aiming to outperform liabilities by 0.5% to 1.5% a year. During 2024, returns ranged from a more than 5% gain to a loss of more than 1%, a wider dispersion than among mandates targeting higher performance.

The consultancy said there were different objectives within this group – such as those targeting insurance buyout and those aiming to run on for longer – as well as a wider range of investment strategies.

“Accuracy of hedging also plays a key role when return targets are lower,” the report stated.

“Spending time discussing what a scheme needs up front and which fiduciary manager can best meet those needs is vital to align interests and outcomes.”

Sarah Leslie, Ndapt

The report identified significant dispersion of returns depending on provider, which Barnett Waddingham said meant that manager selection was key to the success of an outsourcing arrangement.

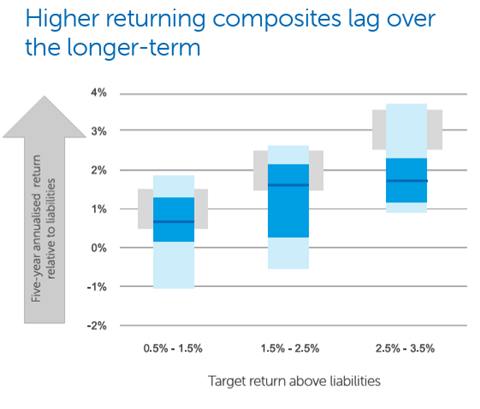

Over five years to the end of 2024, performance was “not outstanding, especially considering the market environment”, Barnett Waddingham reported.

In particular, fiduciary managers with a higher performance target – 2.5% to 3.5% above liabilities – underperformed relative to their objectives. Asset allocation differences, as well as differing approaches to hedging, were the main reasons for the range of returns, the report said.

Sarah Leslie, a professional trustee at Ndapt quoted in the report, said: “It is important to recognise the range of outcomes a fiduciary manager can deliver, and that risk can vary considerably as well as return.

“Spending time discussing what a scheme needs up front and which fiduciary manager can best meet those needs is vital to align interests and outcomes.”

How fiduciary managers handled tariff-induced volatility

Meanwhile, a separate study from Isio has found that fiduciary managers generally “responded well” to recent volatility caused by geopolitical tensions and international trade disputes, focusing on tactical adjustments rather than larger changes.

Half of fiduciary managers surveyed by Isio have adjusted tactical equity allocations in the wake of the US attempting to levy tariffs on imports. A third have downgraded their overall outlook for equity markets.

Instead, fiduciary managers are growing more positive on investment-grade credit, with a third identifying this asset class as potentially providing attractive returns – at least in the short term.

Despite these tactical adjustments, most fiduciary managers were “sticking to their guns” and not making changes to long-term strategies, according to Isio. Most activity was focused on rebalancing activity.

Paula Champion, partner and head of fiduciary management oversight at Isio, said managers had typically “responded well” to recent challenges.

“Against the current backdrop, schemes will be seeking confidence that the [fiduciary manager’s] plan is still the right one to meet their objectives.”

Paula Champion, Isio

“The reduction in equity exposure and growing interest in credit demonstrates a pragmatic response to near-term risks and opportunities,” she said.

“What stands out is the clear distinction between short-term tactical moves and long-term strategic discipline,” Champion continued. “While there may be opportunities to utilise market dislocation, lower equity pricing and widening credit spreads, investor confidence has been damaged, and we can expect volatility to continue.

“Fiduciary managers have proven they are adept at responding to volatility without losing sight of the long-term plan but, against the current backdrop, schemes will be seeking confidence that the plan is still the right one to meet their objectives.”