What models could have delivered the retirement outcomes Generation X deserves, and could elements of income security rescue future generations at risk of being let down by defined contribution?

Despite efforts being made to cushion the blow of defined benefit disappearance, almost 40 per cent of 'in-betweeners' (straddling generations X and Y) recently surveyed by Old Mutual Wealth had saved less than £5,000.

Generation X now seems destined to retire poorer or work longer, the latter being in the extreme something that even the least paternalistic employer might not welcome.

Australia was held up as the panacea, and when we went out there we found that it wasn’t

Paul Leandro, Barnett Waddingham

What models could have delivered the retirement outcomes this generation deserves, and could elements of income security rescue future generations at risk of being let down by DC?

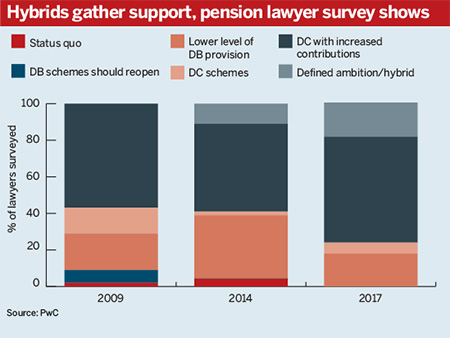

The problem with a DC future

The argument for hybridisation rests on the conclusion that DC in its current form is structurally incapable of delivering wholesale adequate outcomes in retirement. Most industry experts agree that the current contribution rates required by auto-enrolment are woefully low, but point out equally quickly that they will not stay at that level forever.

Australia is often touted as the ideal DC economy. Having introduced compulsory superannuation fund contributions for employers 25 years ago, our antipodean counterparts have been locked into 9 per cent contributions for some time, with increases to 12 per cent in the pipeline.

But Paul Leandro, head of Barnett Waddingham’s DC consulting team in the north and Scotland, says the picture is not as rosy as it seems.

“Australia was held up as the panacea, and when we went out there we found that it wasn’t,” he recalls. Savers were not using their pots wisely, leading employers to conclude that DC “doesn’t necessarily support them into retirement, which is one of my business objectives.”

Australian supers will now be required by government to offer comprehensive retirement income products to members, the Australian trade press reports.

How else can outcomes be secured?

If driving a return to annuity-like products might be seen to fly in the face of the pension freedoms announced by George Osborne in 2014, then income security provided by schemes may yet have a role to play in the UK’s future environment.

Of course hybrid schemes have existed for years. All schemes with a DB and DC section are technically classed as hybrids. But combining DB and DC benefits has historically been much more difficult.

Chantal Thompson, pensions partner at law firm Baker McKenzie, is involved with a DC scheme which, as a quirk of contracting out of the state pension before 1997, has to pay a guaranteed minimum pension. It also underpins a small DB ratio for members transferred in from another scheme.

“Underpins are just really hard work and people don’t really understand the value [of what’s being promised to them],” she says.

Can't fault the ambition...

More recently, the Department for Work and Pensions under Steve Webb floated proposals for defined ambition pensions.

These risk-sharing arrangements included the pension builder model, where a proportion of contributions would be used to buy tranches of deferred annuity, with the remaining funds being invested in return-seeking assets, with a view to funding conditional pension increases.

There’s value in pooling across generations, which allows promises to be made and for the risks associated with them to be shared

Michael Chatterton, Law Debenture Pension Trustees

In defining a shared-risk scheme and collective benefits, the Pensions Act 2015 also paved the way for collective DC schemes. CDC was recently hailed as a “purposeful” solution to the pensions crisis by London Business School executive fellow of finance David Pitt-Watson.

In the end, says Mark Smith, pensions partner at law firm Taylor Wessing, the reason defined ambition propositions have never gained traction was not down to their individual flaws, but rather a broader problem with the ever-changing pensions industry.

People find it hard to trust a system that is constantly meddled with, he argues, and further changes could ruin pensions. “That ‘once bitten twice shy’ mentality might mean that people aren’t going to go for it, particularly when you’ve got things like the [lifetime Isa].”

The problems persist

However, argues Kevin LeGrand, president of the Pensions Management Institute, the current system also leaves people alienated.

“With a plain DC scheme, all of the decision-making and all the risk is with the member, and members by and large aren’t clued up enough to deal with that effectively, and we struggle to find ways of helping them acquire the knowledge,” he says.

LeGrand also questions the common assertion that employers have no appetite for bearing risk: “Some of them actually do, and we know that there’s a tranche of employers who still cling on to their defined benefit obligations.”

I’m not hearing any clamour from any of my clients for having a hybrid DB or DC scheme

Brian Henderson, Mercer

This paternalism among employers, agrees Michael Chatterton, managing director of Law Debenture Pension Trustees, makes the case for further effort on hybrid provision.

He says a small portion of traditional DB benefit, topped up by a DC pot, could control employer costs and provide security for members.

“There’s value in pooling across generations, which allows promises to be made and for the risks associated with them to be shared,” he says; it is the level of DB promises made to date, rather than their DB status, which makes them unaffordable.

Time to drop the focus on pensions?

But for many in the industry, the lack of market interest in hybrids is testament to the opposite.

CDC could refocus industry on purposeful finance

Refocusing the industry on the purpose of finance could deliver huge benefits to UK pensions, a new academic paper has suggested, as calls were lodged for the resurrection of collective defined contribution.

“I’m not hearing any clamour from any of my clients for having a hybrid DB or DC scheme,” says Brian Henderson, leader for DC and financial wellness at consultancy Mercer.

Neither DC’s accumulation or decumulation problems are insurmountable, he argues, and indeed many employers are embracing initiatives that do just that.

A steady transition towards better-governed mastertrusts will improve the quality of DC provision, alongside increasing employer focus on the broad financial health of employees.

With technology lowering the cost of advice provision, companies will look to improve the ability of employees to deal with debt management and other issues, including prudence around DC accumulation and decumulation.

“You’ll find that companies are looking to cater across the workforce in a broad sense rather than a very narrow pensions sense,” he says.