Siemens, one of the world’s largest electrical companies, aims to give its UK defined contribution scheme members more potential for growth while reducing costs by adding a pure equity phase to its DGF-heavy lifestyle options.

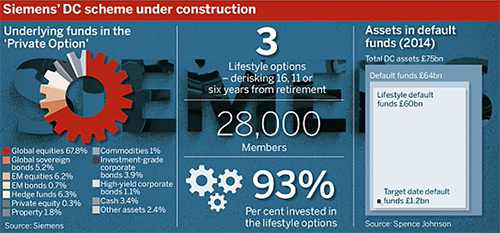

Of nearly 28,000 members in the DC scheme, 93 per cent are invested in lifestyle funds.

The three all target annuity purchase, starting out with a mix – dubbed ‘Private Option’ – of half passive global equities and half diversified growth, to then derisk either 16, 11 or six years before retirement, with the 11-year option being the default fund.

This month, the scheme will change this: members more than 25 years from retirement will soon hold only passive global equities before moving to the ‘Private Option’ and then derisking.

Robert Bennett, senior manager of pension investment at Siemens UK, said the possibility of better returns had led the fund to make this change for younger members.

The fees… are clearly lower than the charge cap anyway but then it’s a reasonable reduction in AMC

Robert Bennett, Siemens UK

“They’re obviously further from retirement so they can tolerate that volatility, and the aim is for that to provide them with the potential for greater real growth in their investments during the earlier years of their membership,” he said.

But the higher costs of diversified growth funds played a role too, according to Bennett: “Obviously there is a cost associated with DGFs in excess of that you get from investing in passive global equity.”

The charges will reduce from their current levels. “The fees… are clearly lower than the charge cap anyway but then it’s a reasonable reduction in AMC,” Bennett said.

Anne Swift, principal consultant at consultancy Aon Hewitt, also said a lifestyle strategy should start with a growth phase.

“If you’re young, you can really withstand a lot of volatility in your investment return because the biggest influence of a future retirement at that point is not so much the investments, it’s the contributions you pay in.

“We then see the multi-asset or DGF phase coming in sort of mid-career, where you are starting to grow a reasonably sized pot of money, and that’s when you start to be able to have much less tolerance of potential shocks in your fund value,” she said.

But Swift said what type of fund a scheme can afford will depend on its buying power and the charge cap, which can mean that DGFs have to be mixed with passive equities, although she conceded there were some lower-cost DGFs available now.

Schemes need to understand the difference between the various DGF products on offer and make sure they have the right one for their circumstances, she said, with more capital preservation-type ones “fitting in quite nicely in the mid-career phase”.

Justin Simler, investment director of multi-asset at Investec Asset Management, said the attraction of DGFs lies in the embedded risk management, active asset allocation and access to niche asset classes they provide.

The lower volatility, he said, “helps to avoid the phenomenon of the discouraged investor – someone who sees a large fall in equity markets in the value of their pension fund and stops investing”.

He said many schemes opted for a mix of equities and DGFs or a pure initial equity phase, but noted that “if cost wasn’t an issue, then DGFs are a better solution”.

Default funds: More than one way to achieve value

The question of whether and how default funds are delivering value for money was debated at a recent event - read the responses here.

Target date funds vs lifestyle

The Siemens UK scheme is also considering what to do in response to freedom and choice.

Bennett said: “We are looking at what options come to market. At the moment I know some managers are starting to launch products; we’ve looked at target date funds as one possible option, but it’s early days.”

Swift noted a lot more target date funds were coming to the market.

“I think in some respects they’re very similar to lifestyle... but of course you’re delegating an awful lot more away with target date funds. You’re delegating the whole glide path design, you’re delegating all of the underlying fund construct, and that’s not necessarily going to be for everybody,” she warned.

“But I certainly think that they can provide quite a bit of flexibility because you haven’t got that administration issue – if you want to make a change… it can all be done within a single fund structure.”