Official data have shown employers with between 1,000 and 4,999 employees on average contribute more to their defined contribution schemes than their larger and smaller counterparts, as industry experts call for increased contributions.

Data released by the Office for National Statistics last week on membership of occupational pension schemes found these mid-sized employers contributed 6.7 per cent to DC schemes, with employees contributing on average 3.4 per cent.

This is compared with employer contributions of 5.9 per cent for those with more than 10,000 staff, and 5.8 per cent for those with between 12 and 99 employees, with employees contributing 2.7 per cent and 2.8 per cent respectively. However, the data were influenced by employers auto-enrolling at the initial 1 per cent contribution level.

Richard Butcher, managing director at professional trustee company PTL, said the current average contribution was “woefully low”, adding: “Looking ahead, lower earners stand to receive [a better] replacement income ratio [through] the state. For higher earners, current levels of contributions will not provide the desired standard of living if people want to retire in their mid-sixties.”

Butcher said the average contribution metric was skewed by the vast numbers of auto-enrollees currently contributing 1 per cent, but highlighted the area as a potential concern for the future.

He said: “Ultimately more people saving is a positive step forward; once everyone is in we will be in a position to make informed judgments about the average and its movements, and work from there.”

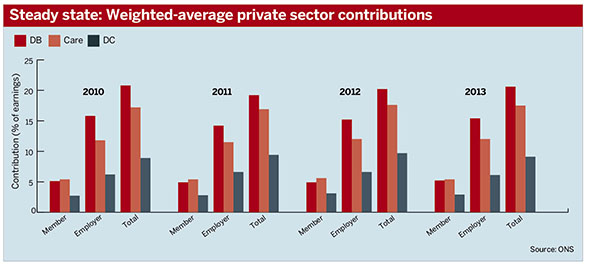

The ONS data found for defined benefit schemes in the private sector, the average contribution rate was 5.2 per cent of pensionable earnings for members and 15.4 per cent for employers [see graph].

Contribution rates to DB schemes continued to be higher than those to DC schemes. The average contribution rate for DC has decreased as membership has increased with the auto-enrolment population.

The number of active members of occupational schemes also increased, rising to 8.1m in 2013 from 7.8m in 2012. The figures reflect the early impact of auto-enrolment as large employers were the first to implement the reform.

Andy Cheseldine, partner at consultancy LCP, said: “With the schedule of phasing-in being an ongoing process, when viewing this data we must keep in the back of our minds that it is representative of a moving picture.”

Additional members enrolled since April 2013 could constitute 4m new members in addition to the increase of 300,000 recorded last year, said experts.

Butcher anticipated that incorporation of these additional members into the data would result in a more pronounced uptick of members and further decrease average contributions. As auto-enrolment rolls out up to 2018, membership will peak at a predicted 8m.

Cheseldine said that as people enter the workplace and move around, there could be up to 300,000 new enrolments every month. “There will be a lot of effort on the part of pension schemes going on behind the process,” he said, adding: “New legislation is presenting ongoing administrative challenges to pension schemes.”

Plans to lower the earnings threshold for auto-enrolment proposed by the Labour Party in May could increase membership further, with the opposition planning to bring an extra 1.5m into pensions saving if it wins the next election.