The University of Oxford has introduced a defined contribution scheme for new joiners and is making a number of other changes to reduce costs as universities are waking up to their pension deficits. One expert called the education sector ‘a disaster’ in pension terms.

Universities across the nation are in focus this week as academics are going on strike over the proposed closure of the Universities Superannuation Scheme, and the pensions pain in the higher education sector is unlikely to go away any time soon.

The education sector in pension terms is a disaster, there are problems from top to bottom wherever you look

David Davison, Spence & Partners

Some universities that have standalone schemes, mostly for non-academic staff, are already adapting their benefit structure along the lines of the closure proposal by Universities UK, the body representing employers. The University of Southampton recently consulted on closing its defined benefit scheme, for example.

Following the USS textbook

Funding difficulties are also hitting home for the 14,457 members of the University of Oxford Staff Pension Scheme.

“The employers have made extensive changes to OSPS, with the aim of reducing future benefit costs and ensuring the scheme remains sustainable,” trustee chair Nick Sykes told members.

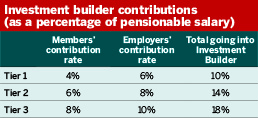

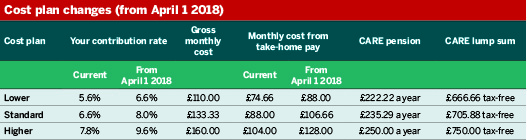

In October 2017, the career average revalued earnings scheme closed to new joiners, who are offered money purchase instead, while members who continue to accrue Care benefits will have to make higher contributions from April this year.

Those who were in the final salary section before 2013 will have their pension calculated based on salary at March 31 this year.

As part of the cost-cutting drive, the scheme also moved away from the retail price index for indexation and revaluation purposes in April last year, taking the unusual step of using an average of RPI and the consumer price index.

The £647m scheme was 80 per cent funded at its last full valuation two years ago, and 79 per cent last March, representing a £170m deficit.

Employers agreed to make extra contributions with the aim of reaching full funding in mid-2027, paying in 23 per cent of members’ pensionable salaries from August 2016 to July 2017.

However, “this level of contributions would not be affordable for the employers over the longer term, so it was agreed to reduce it to a more affordable 19 per cent after one year,” according to the scheme. In the year ending March 31 2017, employers contributed £29.6m.

Education schemes marked down

Pension schemes of universities tend to be modelled on the USS, and therefore Oxford’s changes are not surprising, said David Davison, owner and director of consultancy Spence & Partners.

The move to DC-type solutions for the Local Government Pension Scheme, charities and universities is consistent, he said, although it has taken longer than in the private sector, partly because of a more paternalistic attitude.

But the delay in universities following this trend is also down to other factors. Davison said employers in the education sector are “constantly complaining it’s difficult to get the information they need – the valuation is a shock every three years because there is not a mechanism for keeping people updated more regularly”.

Funding gaps do not happen overnight, said Davison; more monitoring and communication of the funding position would allow employers and schemes to address any issues earlier.

Southampton uni’s DB closure proposal poorly timed, experts say

The University of Southampton is consulting on the closure of its defined benefit scheme for non-academic staff, a move experts have said is not well timed given current scrutiny of senior pay packages at universities.

Davison’s verdict of the sector as a whole is damning. “The education sector in pension terms is a disaster… There are problems from top to bottom wherever you look,” he said. Ultimately, “it ends up coming off our kids’ education costs”.

But Kirsty Bartlett, partner at law firm Squire Patton Boggs, said things are changing. “There’s definitely a move towards keeping an eye on funding more regularly, trying to see off problems… as they develop,” she said.

Bartlett was more empathetic with the financial demands on universities, saying that “mentally we often put them in the public sector box, but the covenant can be quite different”. They are not tax-raising bodies but are “at the whim” of tuition fee levels set by government and of international commercial pressures, she said.

Precisely this has however led some to conclude that universities have not suffered as much from austerity as other public service institutions, thanks to higher tuition fees and a removal of a cap on student numbers. They say this is partly what is angering employees when faced with low wage growth or reduced pensions.

Universities not spared from s75

Monitoring and communication has not been the only issue when it comes to university pension schemes, said Davison.

“The other big problem is the section 75 regulations. A lot of employers in these schemes would have taken the decisions for themselves to stop accruing, but can’t because of s75 debt,” said Davison.

He gave the example of an employer in the USS. The scheme was not able to give a precise s75 value, making it impossible to get a clear idea of the costs of leaving.

A USS spokesperson said: “We provide indicative section 75 quotations to employers on request in timescales that are consistent with other pension schemes that offer the facility.”

The Department for Work and Pensions issued a call for evidence in spring 2015 regarding employer debt in non-associated multi-employer schemes, responding two years later in a further consultation and proposed regulations. These would introduce the option of deferring payment of a s75 liability. A response to this consultation is outstanding.

LGPS employers turn to gradual scheme exit

University employers keen to leave a scheme might take inspiration from the local authority sector.

Barry McKay, partner at consultancy firm Hymans Robertson, said a number of admitted bodies, such as colleges and housing associations, “are trying to exit from the LGPS because the costs and the risks have increased over the last three to four valuation cycles”.

To make such a move affordable, some employers leave step by step, said McKay, with a repayment plan put in place. “More and more we’re seeing managed exits over a period of time, and some funds are allowing that.”