Here's your guide to an eventful day for the UK workplace pensions industry.

The FCA sets levy framework

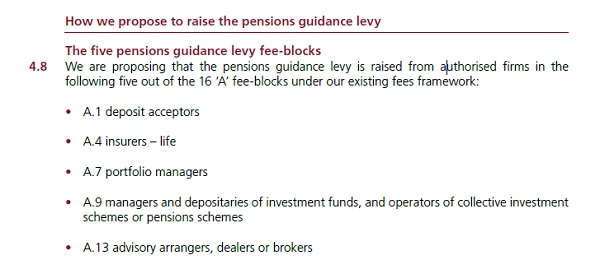

The Financial Conduct Authority has given further detail on how to split the tab for its pension guidance levy, with those holding the money for longer, if savers turn their back (further) on annuities by April 6, having to pay for the privilege.

Source: FCA

Advisers are the big winners from the changes: "In chapter 4 we are therefore proposing to consult on an equal allocation across the five pensions guidance fee-blocks with a 50 per cent reduction for A.13 to reflect that financial advisers have less potential to benefit than the product providers in the other four."

But it inevitably did not please everyone. Trust-based schemes are left out of the mix, at least through this mechanism, given the FCA's regulatory scope: it cannot levy them, whether it wanted to or not.

Calling out the main mastertrust providers John Lawson, head of corporate benefits policy at Aviva, tweeted in response to the news: "Would be even lower if @nestpensions@NowPensions and @PeoplesPension paid their fair share."

But watch this space. The FCA has passed on to the government responses that suggested the Pensions Regulator and the Department for Work and Pensions should pay towards the guidance from a general levy on trust-based schemes.

The FCA sets levy framework

The Financial Conduct Authority has given further detail on how to split the tab for its pension guidance levy, with those holding the money for longer, if savers turn their back (further) on annuities by April 6, having to pay for the privilege.

Source: FCA

Advisers are the big winners from the changes: "In chapter 4 we are therefore proposing to consult on an equal allocation across the five pensions guidance fee-blocks with a 50 per cent reduction for A.13 to reflect that financial advisers have less potential to benefit than the product providers in the other four."

But it inevitably did not please everyone. Trust-based schemes are left out of the mix, at least through this mechanism, given the FCA's regulatory scope: it cannot levy them, whether it wanted to or not.

Calling out the main mastertrust providers John Lawson, head of corporate benefits policy at Aviva, tweeted in response to the news: "Would be even lower if @nestpensions@NowPensions and @PeoplesPension paid their fair share."

But watch this space. The FCA has passed on to the government responses that suggested the Pensions Regulator and the Department for Work and Pensions should pay towards the guidance from a general levy on trust-based schemes.

Source: FCA

As reported by our colleagues at FT Adviser, the FCA also revealed it would publish a consultation in due course on the rules of requirements of at-retirement products – with drawdown and uncrystallised pension fund lump sums top of the agenda.

Big and messy: TRW buyout

The buyout market continues to grow as insurers focus on those parts of their pensions business that can still be relied upon, such as employers' desire to get rid of their defined benefit exposure.

But the £2.5bn buyout announced today of the TRW Pension Scheme was fiendish in its complexity, tying together a pension increase exchange exercise, an enhanced transfer value exercise, winding-up lump sums, a pensioner buyout and the dreaded equalisation of guaranteed minimum pensions.

I've sat down with providers in the past that have turned their nose at some of the smaller derisking transactions, questioning whether they are worth the expense given the complications they build into liability structures.

Perhaps it demonstrates providers' willingness to take on the complicated deals to secure the premia in what observers suggest is becoming an increasingly competitive market. For schemes, it shows that the ETV-Pie-buyout jigsaw puzzle can be put together.

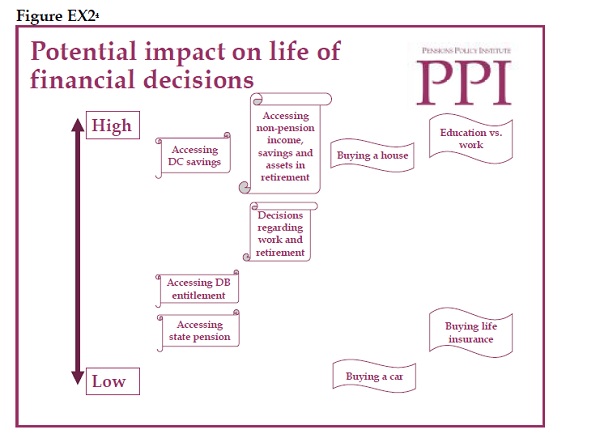

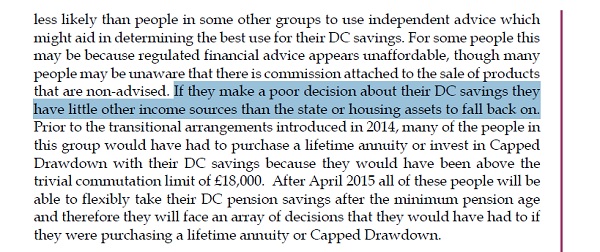

Are you in the DC danger zone?

If you have between £19,400 and £51,300 in your DC pension pot and no DB scheme, you could be at high risk, according to a report released today by the Pensions Policy Institute in association with provider Fidelity Worldwide Investment.

Converting that pension will be one of the toughest life decisions you have to make:

Source: PPI

For these savers, the stakes are high:

The PPI concludes, not unsurprisingly, that the aforementioned guidance guarantee is going to be crucial in getting DC savers to good retirement, and sees big questions around "what the take-up of the guidance may be, whether the guidance will be able to meet the level of need and the complexity of the different individual and household circumstances, and the likelihood that individuals will follow up on the guidance they receive with timely and appropriate actions".

That guidance guarantee better be worth the money.