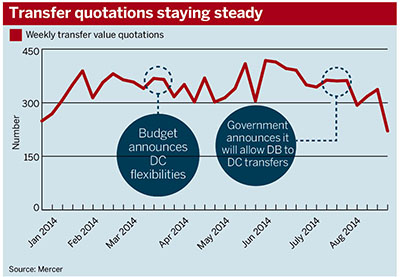

Predictions that the Budget flexibilities would lure members out of defined benefit pension schemes have so far proved unfounded, as data show no uplift in the proportion requesting transfer value quotations.

Data provided by Mercer, covering around 1m savers whose pensions it administers, show requests have remained broadly flat, even after the chancellor’s Budget announcements in March and the resulting wave of publicity (see graph).

The number of weekly requests for a transfer-out quotation hovered above the weekly average of 343 for a few weeks in June, before falling back in July, with August’s summer lull pushing levels to their lowest point since Christmas 2013.

“I thought we might see a bigger spike in activity,” said Alan Baker, head of defined benefit risk at Mercer. “There was a little bit of activity post-Budget but nothing dramatic, and now it has backed off again.”

About half of the DB members in the data set are deferreds, with the rest split between active and pensioner members, weighted towards the latter.

DB members could be waiting until April to transfer, when anyone aged 55 or older will be able to take their defined contribution pension pot as cash. This will be subject to their marginal rate, over and above their 25 per cent in tax-free cash.

Kevin LeGrand, head of pensions policy at Buck Consultants, said the attraction of taking cash should not be understated, adding: “I would expect once it becomes fully [operational] we will see a big increase in the amount of people that are tempted to move across into taking cash.”

Benefits experts have cast doubt over whether in the majority of cases a transfer out of a guaranteed DB plan into DC presents good value, though others have claimed the flexibilities could meet some retirees’ short-term needs.

The government announced in July that it would allow DB members in funded schemes to transfer into DC plans, raising the hopes of employers looking to offload a chunk of their liabilities with departing members. Consultancies have reported as many as three in four clients considering incentive exercises to encourage such moves.

There could be a middle way if schemes opt for partial transfers, if allowed by the scheme.

“A handful of schemes allow this already,” said Nathan Long, head of corporate pension research at platform provider Hargreaves Lansdown.

“If this becomes more widespread, it could allow individuals with one large DB pension who had worked for a single employer for their entire career to transfer some of their accrued benefit to enjoy the new pension freedoms.”

He added specialist advice should be sought before any such transfer.

A spike next year in transfer requests could yet provide an administrative headache for schemes also dealing with the end of contracting-out and guaranteed minimum pension reconciliation exercises.

“If there is a big uptick in [transfers] then that adds to the burden,” said Baker.

The difficulty of the decisions facing scheme members in this regard has increased pressure on the guaranteed guidance promised by the chancellor.

The Financial Conduct Authority plans to publish principles-based standards for the provision of this guidance by late autumn.