The retirement flexibility brought about by the Budget has left many schemes wondering how to best implement the at-retirement options introduced.

From next April, defined contribution members will be able to forgo annuity purchase and instead opt to take pension pots as cash, which apart from the tax-free lump sum will be taxed at the marginal rate. The announcement was heralded by some as a step forward in the UK pension landscape but was met with derision by many others that claimed members could not be trusted to properly manage their retirement income.

Comment: Lessons from Down Under

In Australia for many years retirees have generally had the choice between a lump-sum payment or a regular account-based pension paid from their DC pot. Lifetime annuities have not been a major feature of retirement solutions in Australia.

The large Australian DC schemes typically offer a number of pre-mixed multi-asset investment choices by risk level, eg ‘capital stable’ or ‘balanced’, and some asset class choice, such as domestic or international shares.

This is in contrast to many UK DC schemes which offer greater asset and manager choice, but generally less choice by multi-asset risk profile.

A benefit of the large-scale Australian DC market is that it encourages innovation by providers as the fixed costs incurred are justified; this comes in the form of improved lifestyling strategies, policyholder communications and tools.

The UK market is more fragmented, though the rapid pace of innovation will inevitably lead to winners, losers and consolidation in the post-Budget world.

Super-providers could offer comprehensive solutions in the pension accumulation and drawdown stages, as well as complementary retail investment and annuity offerings, learning from the lessons from Australia.

Bruce White is head of portfolio strategy, Legal & General Investment Management

As a result, some have been looking to the DC markets around the world for guidance and similarities have been drawn between the US, where buying an annuity is not obligatory, and the proposed UK system.

According to research by consultancy Aon Hewitt, the proportion of US employers that offer DC benefits as a primary means of retirement provision is increasing. In 2013, 77 per cent of employers had a DC plan as the primary offering, compared with just over half in 2001.

Fiduciary manager SEI found that of the employers that only offer DC plans, 39 per cent said the objective of the plan was to provide supplemental retirement income.

Scott Brooks, managing director of DC at SEI in the US, says the DC plan is the primary retirement benefit offered at the majority of companies, with the other primary income source being social security.

“There is the need for education on the part of the plan sponsor to highlight that it is a primary benefit for their workforce and is an under-utilised source of savings for retirement,” he says.

Due to weak economic growth after the financial crisis, companies in the US had been reticent to put in place auto-enrolment and auto-escalation.

However, more plan sponsors are now looking to use such measures to provide sufficient retirement incomes.

“We are now seeing, especially among defined benefit sponsors that are terminating or otherwise getting rid of their DB schemes, that this is the primary benefit,” Brooks says.

Retirement options

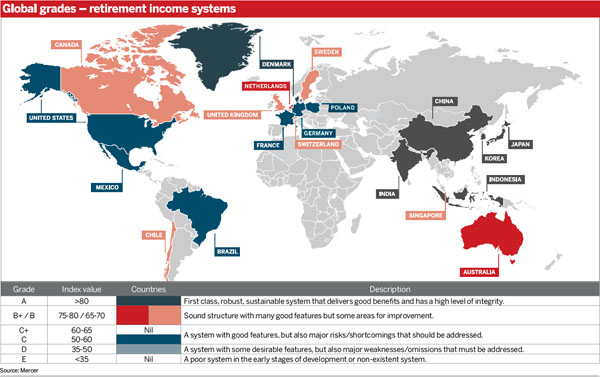

The outlook for DC members around the world is not bright. The Melbourne Mercer Global Pension Index (see graphic) states the most obvious risk to DC members is running out of money.

It also points to another problem of retirees not withdrawing their money quickly enough, as they may be worried about longevity or higher inflation.

The 2013 index report states the need for personalised financial advice for retirees is greater than ever. “Yet, the conversion of DC benefits into adequate and sustainable retirement incomes remains a largely unresolved problem in many countries,” it adds.

Nico Aspinall, head of DC investment at consultancy Towers Watson, says he had spoken with colleagues in the US that are grappling with the issue of income and outcome. “They look at our annuity market with envy,” he says.

Aon Hewitt, which surveyed 400 US employers across a spectrum of plan types, sizes and industries, found 83 per cent of members took a lump sum, 11 per cent installment payments, 21 per cent partial distribution and 9 per cent annuities (these can overlap).

Fredrik Axsater, head of global DC at State Street Global Advisors, says only 19 per cent of scheme members in the US make a withdrawal from their DC retirement pots in the first five years of retirement, as they are trying to figure out their retirement lifestyle.

“They are looking at other types of savings and spending that, and increasingly, many of them maintain some level of employment,” he says.

And for about half of members, the date of retirement is not a conscious decision, something happens such as sickness or being laid-off, he says.

“The goal of the industry should be trying to get more people to participate in the plan, to save early, to save enough, so that their retirement decision is made by them,” says Axsater.