From April, savers will be faced with tough choices when it comes to drawing their pension: take the entire pension upfront, remain invested throughout retirement or buy a guaranteed income through an annuity.

Workplace pension schemes must reconsider their derisking strategy. No longer will schemes be able to move default investors into bonds on the assumption most will buy an annuity.

The solution is to derisk the workplace pension over five years, moving default investors from their growth investments to cash. The two complement each other well. I’ll explain why…

We will see a mix-and-match approach to retirement by many retirees. This is a sensible approach to taking a sustainable income and will serve many retirees very well.

Many providers are creating several default investments: members must choose which default based on whether they wish to take a lump sum, remain invested or buy an annuity.

This is sensible, but still requires two things: to dramatically increase staff engagement with pensions and provide a default investment for those who make no decision whatsoever.

The solution is to derisk the workplace pension over five years, moving default investors from their growth investments to cash

Cash can be that default…

Cash does the one thing we all want when we approach retirement; it avoids the catastrophe of an asset class correction when close to retirement.

This does not solely concern investment in shares. With gilt yields at record lows, an increase in interest rates could see anyone trying to shelter their pension pot here before retirement sorely let down.

Undoubtedly it will be more popular to remain invested during retirement, but defaulting pension savers into this environment is a step too far. Doing so normalises income drawdown, when it should be a strategy used for those happy to take the extra risk with their pension in retirement.

In addition, the idea of a ‘semi-retirement’ – where employees go part-time and draw only a small amount of income from their pension – may become the norm.

Retirement will not occur at a set point – decisions will be made when it suits each person based on their lifestyle, which could include not finishing work at all.

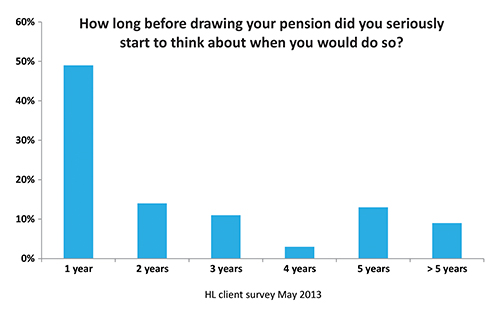

Our research, conducted prior to George Osborne’s Budget, showed almost half of retirees did not think about retirement until a year before taking benefits (see graphic below), while the Pensions Policy Institute found staff are unlikely to engage with retirement until two years before.

With improved financial education we can expect to encourage savers to engage with their choices five years from retirement, especially as pensions are becoming more interesting.

I recently overheard a conversation on the bus between two middle-aged men talking each other through their retirement strategy in quite some detail. Until recently this would have been social suicide.

The day may come where employees think about retirement 10 or 15 years prior to retiring. For now, a five-year derisking into cash suits this new landscape.

Nathan Long is head of corporate pension research at Hargreaves Lansdown