Avon Pension Fund is looking to invest £150m in infrastructure, in conjunction with other local authority funds.

The total size of the investment will be between £250m and £350m. “The main reasons for going into infrastructure are its inflation-linked nature, cash-generating properties and diversification of the portfolio,” says the £3.3bn fund’s assistant chief investment officer Matt Betts.

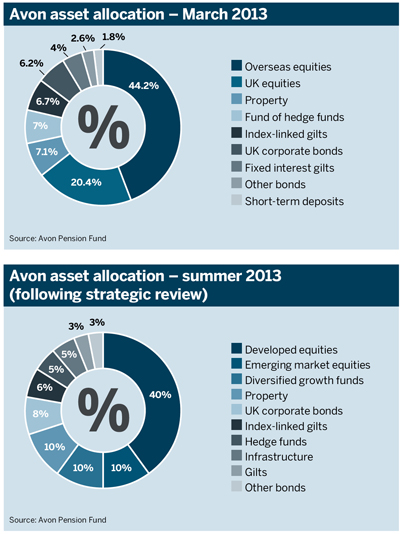

During the summer of 2013, the scheme reviewed its investment strategy, which led to a number of changes in its asset allocation.

The overall spread between growth and ‘stabilising’ assets remained the same, at 80 per cent and 20 per cent, respectively (see graphs).

It added a 10 per cent allocation to diversified growth at the cost of equities. Equities, which consisted of a UK and overseas portfolio, were divided into a developed market and emerging market equity allocation.

The final step was to fill the new 5 per cent allocation to infrastructure.

Over the past year, institutional investors have increasingly turned their attention to infrastructure to diversify their investment portfolios. However, the glare of the spotlight has exposed certain issues, particularly regarding the structure of investment funds.

In response, some schemes have started to look for alternative ways to invest. Avon joined forces with the £1.9bn Dorset County Council Pension Scheme and the £1.2bn Swansea City & Council Pension Fund to look for infrastructure managers. “The joint procurement brings down the cost of procurement, for starters,” says Betts.

Each scheme will contract individually with selected managers, depending on their needs. There is a potential added perk of co-investing, because “if certain funds decide to invest with the same manager, we might have better negotiating powers regarding manager fees”, he explains.

The main problem pension funds face in the infrastructure market is the way investment funds are structured, according to Adam Michaels, investment partner at consultancy LCP. He says: “Investors commit funds, but don’t actually see what they are buying.”

“There is a danger that asset managers who have a lot of committed capital to invest can lose their discipline and buy assets too expensively,” Michaels says.

Additionally, infrastructure funds are often structured like private equity, which can lead to higher fees. Hymans Robertson’s head of manager research John MacDonald says: “Returns from core infrastructure assets are relatively low, so it is often difficult to justify going down the fund of funds route.”

Pooling investments is an effective way of reducing the high costs involved. MacDonald sees cooperation between several pension schemes or investments via the Pension Infrastructure Platform as a step in the right direction.

LCP’s Michaels agrees: “Essentially, the Pip grew out of a group of pension schemes, which didn’t like the typical fund structures and wanted to construct something better. So we’re regarding this with a great deal of interest.”

High fees and prices could potentially lead expected yields to evaporate, certainly now that infrastructure is a hot topic. Nevertheless, because it is linked to inflation and has a long-term horizon, infrastructure remains a viable alternative to low-yielding inflation-linked gilts.

“Another attractive way to access infrastructure is via a listed route, to invest in quoted equity of infrastructure companies,” Michaels says. This type of investment gets around many of the negative aspects of the private equity structure. Funds can have a better insight into what’s in their portfolio, the fees may be more reasonable and, importantly, they can exit more easily.

Hymans Robertson also finds direct infrastructure investment easier to recommend. MacDonald urged caution, though, as these assets are rather richly priced at the moment. “It is important to get a good price, because what funds pay at the outset defines what they will get at the end for core, operational infrastructure. And this is becoming increasingly difficult in the UK.”

Furthermore, Michaels says listed infrastructure assets are more subject to the fluctuations of the stock market, adding that private equity-style vehicles may not be as stable as they seem.

“An area that is currently less developed is infrastructure debt funds, which could be ticking all the boxes for pension funds, especially if they are inflation-linked,” he says.

A middle ground between the listed and unlisted vehicles is slowly emerging: the open-ended fund. It operates like a property fund, where investors can jump in and out fairly quickly, depending on illiquidity.

Both MacDonald and Michaels agree that the competition in the infrastructure market is good. Managers are pushed to do better as schemes, like the Avon Pension Fund, look for alternative ways to gain exposure.