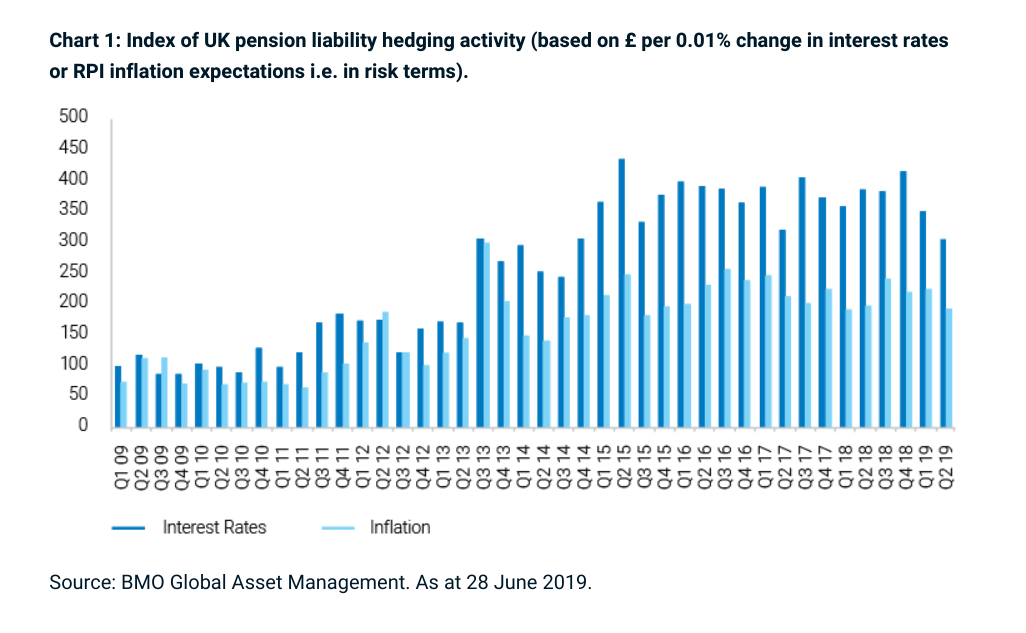

On the go: Interest rate and inflation hedging activity by UK pension schemes saw a dramatic slump in the second quarter of 2019, although experts said this was more likely due to Brexit "frontloading" than a sustained slowdown.

Around £23.3bn of interest rate hedges were put in place between April and July, according to BMO Global Asset Management, a drop of 13 per cent on the previous quarter. Inflation hedging fell by 14 per cent, with total activity of £19.4bn during the period.

According to BMO, uncertainty about geopolitics and their impact on markets has caused the lumpy hedging activity.

Rosa Fenwick, the company's LDI portfolio manager,said: “Geopolitical concerns, including the US-China trade war dispute, Theresa May’s resignation and ongoing Brexit uncertainty have caused a huge shift in market sentiment. This change was reflected in the market with some sharp moves, notably 10-year Treasuries yields dropped 0.40%.

“The decrease in both interest rate and inflation activity is a result of the frontloading of hedging activity prior to the first initial Brexit leave date on March 29. However, the current uncertainty about the route to Brexit has also not aided the markets, with liquidity expected to drop further during the summer months.”

Polling investment bank trading desks, BMO found that gilts and repo agreements remain the most popular hedging asset, despite a pickup of interest in sterling overnight interbank average rate-based swaps. Bulk annuity insurers, by contrast, typically switch into swaps when taking on scheme liabilities. The pause in scheme derisking and continued heavy bulk annuity interest meant gilts underperformed swaps on a nominal basis, BMO said, although it noted that the rising scheme interest in swaps was a sign of the cost of leveraging gilts.

The difference between the retail price index and consumer price index continues to preoccupy liability-driven investors. The change of leadership in government has delayed its response to the House of Lords inquiry into the matter, but BMO said schemes are beginning to wake up to potential mismatches; most have some CPI liabilities but are predominantly hedging using RPI assets.

However, signs of concrete action are still few and far between despite increasing CPI issuance from borrowers.

"The demand is mostly from insurers at present due to the benefit they receive in their matching adjustments, whilst for pension funds the peace of mind from matching their liabilities is offset by the relative expense of the asset," BMO's update said.