Data crunch: Lifetime mortgage providers are hoping to tap into pension fund capital to fuel market expansion, but a combination of limited expertise, social risks and maturing defined benefit liabilities are holding trustees back.

Lifetime mortgages are the most common type of equity release in the UK, and with pensions adequacy still a major issue for the nation, generating income from housing equity could become increasingly common.

Net new lending reached £1.1bn in the last quarter of 2018, according to insurer Just, a new record for the market.

With the market growing at around 19 per cent annually, “there are strong structural reasons why it should continue to grow”, according to Thomas Kenny, director of pricing and property for Just’s retail business.

On the face of it, providing capital to back these loans should be an attractive proposition for pensions schemes. In particular, the payout profile of lifetime mortgages closely matches the longer-dated liabilities of DB plans. Yields are typically between 4 and 6 per cent, while duration is between 14 and 17 years on average.

Bulk annuity insurers such as Just, Aviva and Legal & General invest in large quantities of these investments, while other bulk annuity insurers also participate in the market to various extents.

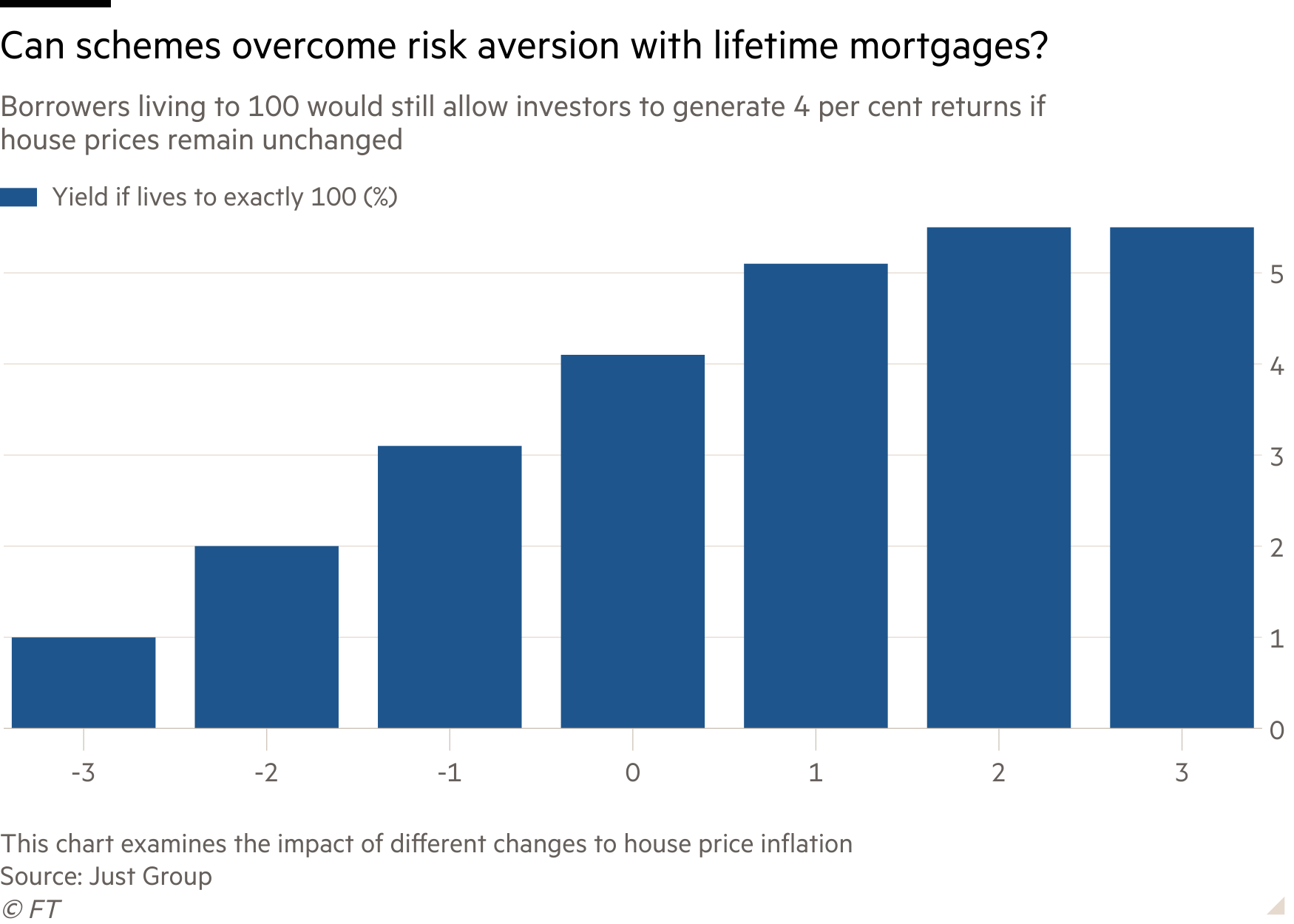

“There is credit risk in the form of the ‘no negative equity guarantee’,” says Mr Kenny. Equity release customers are protected from ever having to pay more than the value of their home against the loan payments they receive.

However, Mr Kenny adds that this is managed carefully: “Even if there’s no house price inflation, the loan-to-value will not reach 100 per cent until the average customer reaches 92 years old.”

Trustees cite lack of expertise

The catch, however, is that few trustees feel they have the expertise needed to effectively run this kind of specialist, emerging asset class. The vast majority of scheme decision-makers feel they do not have the necessary knowledge, according to a poll at the Pensions and Lifetime Savings Association’s annual conference.

A further barrier is one of reputational risk. The no negative equity guarantee on lifetime mortgages stops borrowers from owing anything more than the value of their house to a lender, but if housing is a pensioner’s only substantial asset, they may end up trapped in their house unable to afford social care.

To enforce their lender’s rights, a pension scheme might have to evict relatives of a deceased borrower who have been live-in carers.

You might end up with a part of their lifetime book that they don’t want

Retail DB scheme trustee

A trustee of a publisher’s DB pension scheme tells Pensions Expert: “All of these are terrible personal risks, if you like, and difficult to manage, and very difficult for a pension scheme investing in a bulk way to control.

“Of course, when you originate you don’t know what’s going to happen in the future,” she adds.

Maturity of DB limits illiquid investment

Another challenge for DB pension schemes is their maturity. Almost three out of every four schemes in the UK are now cash flow negative, according to consultancy Mercer.

When the size and sophistication of schemes is taken into account, this means that only 20 per cent of the DB universe are likely to be able to invest in the asset class, admits Just’s head of business development, Rob Mechem. He claims that entering a bulk annuity deal will help other schemes access this asset, despite the fact that plans cannot share in any upside once a buy-in or buyout is signed.

There is also a risk to investing in illiquid assets if a bulk annuity deal is in a schemes future. While all of the UK’s current bulk annuity providers have some investment in lifetime mortgages, it is far from guaranteed that one would accept an in-specie transfer of this asset.

Mr Mechem says the key is “to come early” to discussion with bulk annuity providers, but a trustee of a retailer’s DB scheme with experience in both illiquid assets and buy-ins tells Pensions Expert he is unconvinced.

He says there is a secondary market for these assets due to high levels of demand, but with a sale typically taking around nine months, doing so is tricky with the fast pace of a bulk annuity transaction: “You can get a premium, believe it or not, but you’ve got to wait.”

He dismisses the idea of talking to an insurer early, as most schemes go to the entire market for a quote.

“How do you know which insurer you’re going with?” he asks.

“Maybe you might be lucky and they may take the asset in, but I’ve found that even things like relatively straightforward swaps they don’t like... you might end up with a part of their lifetime book that they don’t want.”