Utilities provider Centrica has saved £23m on future pension liabilities after a pension increase exchange was taken up by a quarter of retired participants across three of its defined benefit sections.

Pension increase exchanges offer members a higher pension payment up front in exchange for giving up some scheduled increases down the road. This reduces the liability carried by the scheme and, as expenditure in retirement is often highest at the beginning, can work well for both parties.

If a scheme has unusual [pension] increases you might find the cost of insuring those in a buy-in is disproportionately high

James Mullins, Hymans Robertson

Pension increase exchanges offer members a higher pension payment up front in exchange for giving up some scheduled increases down the road. This reduces the liability carried by the pension scheme and, as expenditure in retirement is often highest at the beginning, can work well for both parties.

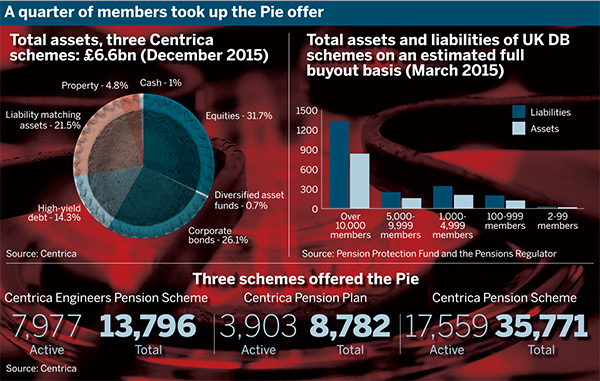

The £6.6bn Centrica scheme carried out the exercise in late 2014 and early 2015, with revised pensions beginning payment on March 1 2015.

Retired scheme members in the Centrica Engineers Pension Scheme, Centrica Pension Plan and the Centrica Pension Scheme were eligible for the option. The company provided independent financial advice to individuals during the process.

A spokesperson for the company said: “Around a quarter of people took up the Pie offer, which involved exchanging some future pension increases in return for a higher immediate pension.”

The option for an increase is now a standard part of the pre-retirement offerings to active members

The spokesperson added: “We provide significant support, through high-quality communications and education, to ensure that people are able to make an informed choice.”

Facilitating insurance transactions

James Mullins, partner at consultancy Hymans Robertson, said: “[Pies] are pretty common these days. There are a number of schemes that have done an exercise or offer exchanges at retirement.”

He added that they were a useful tool for schemes looking to carry out transactions with insurance companies, as they can simplify the risks being shouldered.

“They can make insurance more efficient,” he said. “If a scheme has unusual [pension] increases you might find the cost of insuring those in a buy-in is disproportionately high.”

One example is if a scheme uses the consumer price index for increases to the pension.

“While CPI is common, insurers can’t insure it very easily, there aren’t many assets that match it,” Mullins explained, adding: “Prices will look expensive because they’re having to take some risk because they can’t hedge that.”

He said in such a situation, a Pie could be a win-win: “If you do a Pie in those situations you can have some happy pensioners and a more cost-efficient scheme.”

Balancing act

But Bob Scott, partner at consultancy LCP, said offering Pies was a balancing act between how much to offer and how much the scheme can save.

“The more generous you are [with the uplift] the better the take-up, but then the less savings you get as a result,” he said.

Scott said it was becoming quite common for schemes to offer Pie on a “business as usual” basis, making the option to choose a higher initial income routinely available to all scheme members when they reach retirement.

Incentive exercises are not without pitfalls, but schemes have some resources to turn to. The Incentive Exercise Monitoring Board’s code of good practice, a voluntary code launched in 2012, outlines best practice for schemes carrying out Pies and similar exercises.

While adhering to the code is voluntary, the pensions ombudsman and financial ombudsman service have regard to it, where appropriate, when dealing with complaints that involve incentive exercises.