Defined benefit funding levels have not improved over the past years as gilt yields have fallen, the latest edition of the Purple Book shows, with industry figures hailing partial transfers and scheme consolidation as possible solutions.

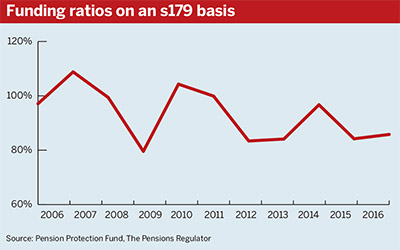

The Pension Protection Fund and the Pensions Regulator’s Purple Book 2016 tells a story that is yet to come up with a happy ending: Schemes’ overall funding level on a section 179 basis stood at 85.8 per cent in March, up 1.6 points since last year but 11.3 points lower than in 2006.

Clearly funding remains a problem for schemes

Andrew McKinnon, Pension Protection Fund

The PPF’s chief financial officer Andrew McKinnon said that since March, funding had fallen further, reaching “an all-time low” of 78 per cent at the end of August, to climb back up to 84 per cent at the end of October. “Clearly funding remains a problem for schemes,” he noted.

Schemes have suffered mainly from plummeting and volatile gilt yields, against which liabilities are measured.

Meanwhile special contributions by employers are going up again, according to the Office for National Statistics, to about £10.5bn in the first half of 2016. “Perhaps that’s encouraging”, said McKinnon.

However, “less encouraging” was the fact that over the nine years to 2013-14, recovery plans have not got shorter, being stuck at an average of about eight years.

The PPF’s chief executive Alan Rubenstein said the lifeboat fund had pushed for scheme recovery plans to be no more than 10 years in its submission to the Work and Pensions Committee.

He dismissed the suggestion that the Pensions Regulator might be allowing excessive recovery plan lengths in order to let more people retire before a potential sponsor insolvency, so that more members obtain the right to a full pension from the PPF.

“I think when the regulator looks at things they look at funding in the round,” he said. “Trustees in certain circumstances may be more inclined to think if the scheme continues then more people will be entitled to full benefits.”

The regulator did not immediately respond to requests for comment.

Stressed employers…

How to address persistent underfunding in the DB universe is a question with more than one answer.

Joanne Segars, chief executive of the Pensions and Lifetime Savings Association, pointed to recent PLSA figures that show the mean cost of running a DB scheme has risen by 37 per cent, reiterating the PLSA's conviction that consolidation would help address cost inefficiencies and make DB schemes more sustainable.

She cautioned that consolidation “is not going to be the silver bullet”, but added: “I think it is important we do tackle these issues, not just think, ‘DB is on its way out, let’s just let it die in the corner somewhere’.”

…or greedy executives?

Segars highlighted the cost for employers of running DB schemes, saying that “sponsors are running to stand-still”.

However, Steve Webb, director of policy at provider Royal London, argued against the idea that companies are overburdened by the cost of DB, pointing to the ratio between deficit repair contributions and dividend payments. The regulator's funding statement analysis from May shows median DRCs as a percentage of dividends almost halved to 9.1 per cent, from 17.2 per cent in 2010.

Webb also highlighted that as fewer DB scheme assets are held in UK equities, dividends are not substantially benefiting those schemes.

“The incentive to managers to pay… high dividends… may sometimes have more to do with the remuneration structure of the people who run British industry than the wider interests of the UK economy, employees [and] pension scheme members,” he said.

“There aren’t any free lunches in this space, but dividends is an area that not enough is being done on.”

Partial transfers

As a solution, Webb hailed the idea of partial transfers-out, claiming these would benefit members, pension schemes and Treasury coffers alike.

“Perhaps we need to think a bit more creatively around pension freedoms: did pension freedoms make these [transfer] numbers change dramatically? Not yet. But should they have done, could they have done? I think probably yes,” he said.

However, recent figures for contract-based schemes show transfer requests rose in the first quarter of the year, and consultants said anecdotal evidence suggests there has been significant growth in DB to DC transfers.

Like Webb, Tom McPhail, head of pensions research at retail investor platform Hargreaves Lansdown, was strongly in favour of allowing people to move part of their DB entitlement to a DC scheme.

He said the binary proposition of transfer or no transfer made it difficult to give financial advice to clients. “If there was scope to offer a halfway house – preserving some benefits in the pension scheme, moving some into a flexible pension arrangement – it would make it far easier for financial advisers to engage in that process with their customers,” he said.