UK corporate schemes ploughed 20 percentage points more of their assets into alternatives in the past three months than the previous quarter, while cutting inflows into fixed income, investment data have shown.

Private schemes allocated 44 per cent of assets to alternatives during the third quarter of this year, compared with 24 per cent over the previous three months, according to data from Financial Times service MandateWire.

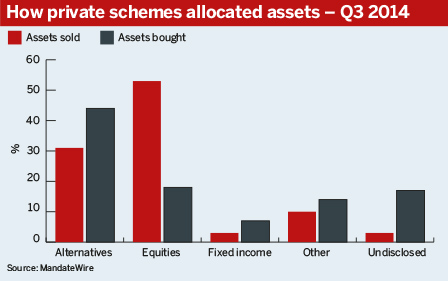

Additionally, equities accounted for 53 per cent of assets sold during the quarter and made up just 18 per cent of assets bought (see graph).

IBM Pension Plan invested £60m in catastrophe bonds as it looked to investments that provide diversified sources of return.

John Belgrove, senior partner at consultancy Aon Hewitt, said the sale of equities and diversification into alternatives is broadly in line with defined benefit schemes’ long-term derisking strategies.

“Pension schemes need return, they worry about their funding volatility and alternatives help to still target returns but in a smoother way,” Belgrove said.

Property was the most popular alternative among private schemes, with nine mandates awarded during the period.

“Where prime… has done very well in property, there’s more looking around outside of that [at] more regional, more developmental property,” he said.

However, there were minimal flows from fixed income, accounting for 3 per cent of assets sold and 7 per cent of those bought by corporate schemes. This is down from the 36 per cent of assets bought during the previous quarter.

Peter Martin, head of manager research at JLT Investment Consulting, said while inflows may have dropped off during the last quarter, in the longer term schemes would continue to diversify their fixed income holdings by investing in assets such as high-yield and emerging market debt.

However, he added: “People were getting concerned over the summer about the additional yield you’re getting on credit getting less, and by how the spreads were getting tight.”

Belgrove said while schemes that have a long-term rule to have more bonds and fewer equities saw 2013 as an opportunity to accelerate some of their bond purchases, they may have put the brakes on this year as prices have risen.

Mark Nicoll, partner at consultancy LCP, said there is a lack of certainty among schemes at the moment over where yield will come from due to the unattractive price of gilts, uncertain emerging markets and European markets looking stagnant.

But he is advising clients to avoid a knee-jerk reaction and alter their asset allocations.

There have also been some schemes derisking this year. However, he said: “They have generally done it by increasing the amount of hedging they’ve got in [liability driven investment] strategies rather than physically putting money into gilts.”

The key for schemes at the moment is to make sure they are not wasting yield and increasing unnecessary costs, Nicoll said.