From the blog: As fixed income markets show signs of nervousness after a multi-decade long rally, institutional investors face critical choices.

How do you control the risk profile of a portfolio while delivering positive returns to investors?

This is particularly challenging at a time when implied volatility of fixed income is on the rise, money markets are delivering negative returns and equities are expensive or fairly valued.

At this stage of the cycle, hedge funds are an attractive alternative to traditional asset classes.

But, despite their strong fundamentals over the long term, the hedge fund industry has been under pressure in recent years.

Its performance has actually lagged behind traditional asset classes since the end of the global financial crisis, which has led to a significant downward adjustment in fees.

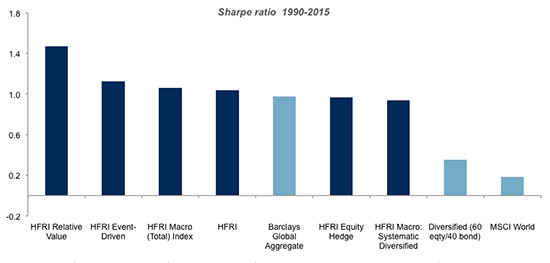

But the long-term track record is strong…

Source: Lyxor, Bloomberg, HFR, Datastream. Note: Sharpe ratio calculated using the 3m interest rates as the risk-free rate.

However, as the beta-driven bull market rally is coming to an end, the environment for alpha generation by hedge funds has improved.

Historically alpha generation has been highly influenced by volatility, correlation and dispersion regimes.

For instance, a low-volatility environment is negative for alpha generation and has damaged hedge fund performance during the time the US Federal Reserve System tamed volatility with its quantitative easing programme.

But more recently, the upward trend in volatility since mid-2014 has bolstered alpha generation.

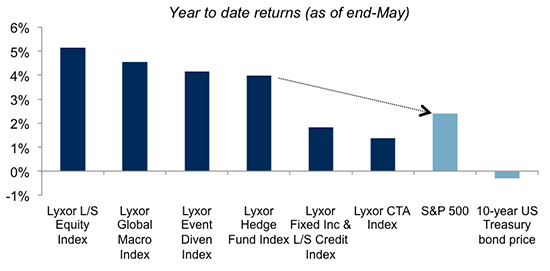

Traditional markets have underperformed hedge funds ytd…

Source: Lyxor, Bloomberg, Datastream

As of end-May, our hedge fund index is up 4 per cent year to date, versus the S&P 500’s total return of 3.2 per cent. Meanwhile 10-year sovereign bond prices are in negative territory both in Europe and the US.

Informed by a few conservative assumptions, we estimate that hedge funds could deliver excess returns in the range of 5-6 per cent a year (over the risk-free rate) with low volatility.

Several scenarios for market developments and their influences on hedge fund returns have been made.

A scenario in which the Fed tightens faster than the market expects would boost hedge fund returns.

Meanwhile, a scenario in which the US economy faces secular stagnation, leading to continued monetary easing, would be less supportive.

Hedge funds have demonstrated their ability to protect portfolios against wide market fluctuations, a scenario that we cannot exclude as the Fed turns the screw.

Philippe Ferreira is head of research for Lyxor’s managed account platform