The £100m Trinity Mirror Pension Plan’s second attempt at a communications exercise to encourage additional contributions, to make up for the employer's decision to reduce payments, resulted in a 60 per cent take-up among the 1,000 members targeted.

The publisher closed its defined benefit scheme in 2003, replacing the final salary scheme with a defined contribution scheme, and gradually decided to lower contributions.

“When the Trinity scheme moved from DB to DC – we are talking about the Maxwell legacy here – the company decided to make the move gradually,” said Laurie Edmans, a trustee on the DC scheme. “They said that when DB was closed they would offer people three different levels of contributions.”

Two years ago, the 7,500-member scheme had to tell its highest-contributing group that company and employee contributions would each go down by 1 percentage point.

After a further two years, this was reduced again. “The fact that the employer reduced their contribution didn’t mean that the employees had to reduce theirs,” said Edmans, pointing to the possibility of making additional voluntary contributions.

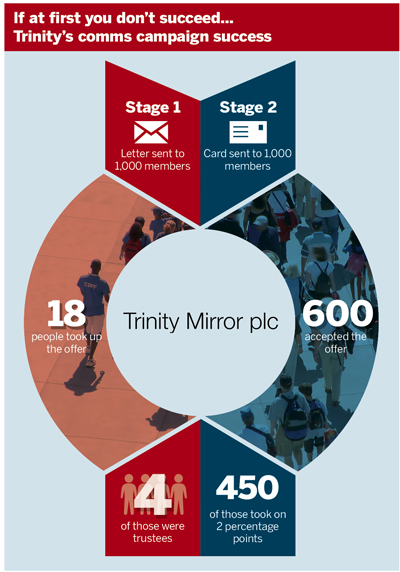

Trinity’s comms strategy

The first round of reductions was communicated to members, telling them their contributions were going down and they could pay into AVCs. Only 18 did, and four of those were trustees.

The second round of reductions took place in March this year. “At first it seemed obvious to do the same thing, but then the penny dropped, so we were trying to borrow some of the inertia and auto-enrolment school ideas,” said Edmans.

A card was sent to members in the top contribution group. It stated that if they signed a letter due to arrive in the near future, their contributions would remain at the same level. The letter in addition suggested that they could put in the extra percentage point the employer used to pay by ticking a box.

Of the 1,000 in the top contribution group, nearly 600 signed and about 450 decided to pay the employer’s percentage point as well.

A cooling-off period for those who had opted in gave them the opportunity to reverse their decision, via a further letter.

“We didn’t send out all the guff with the card or the letter, they got it after they were in,” Edmans said.

The scheme had stopped short of a pure opt-out exercise but made opting in simpler by saying that with little effort, members could keep contributions unchanged, instead of emphasising the change and contribution reductions.

Brian Henderson, partner and UK DC and savings leader at consultancy Mercer, said the key message should be straightforward, simply put and broken into “bite-sized morsels”.

Henderson said engagement could be better achieved “in an emotional way rather than through hard facts”.

He added schemes should, for example, suggest something conveying the end result of workers’ decisions. “If you contribute, you will end up somewhere nice in retirement and not under Tower Bridge,” he said.

Trevor Rutter, consultant at communication agency Like Minds, named the first rule in member communication as, “Don’t mention pensions when you’re in pensions”.

Schemes should instead emphasise what pensions might mean to members, such as “a change in their life and a benefit to look forward to”. He too said schemes should speak to emotions, rather than about tax relief.

And, he added, they should do so through the use of images. “Use images and ideas around them rather than bore people to death with words,” Rutter said.

Of the 1,000 in the top contribution group, nearly 600 signed and of those around 450 decided to pay the employer’s percentage point as well.

A cooling-off period for those who had opted in gave them the opportunity to reverse their decision, via a further letter.

Brian Henderson, partner and UK DC and savings leader at consultancy Mercer, said the key message should be straightforward, simply put and broken into “bite-sized morsels”.

Trevor Rutter, consultant at communication agency Like Minds, named the first rule in member communication as: “Don’t mention pensions when you’re in pensions.”

Schemes should instead emphasise what pensions might mean to members, such as “a change in their life and a benefit to look forward to”.

He added they should do so through the use of images. “Use images and ideas around them rather than bore people to death with words,” Rutter said.

Sandra Wolf is deputy news editor at Financial Times service MandateWire Europe