Data Crunch: Factor investing has attracted a lot of attention from the UK pensions industry. Defined benefit schemes have seen factors as a way to diversify their growth assets and achieve greater control of risk, while defined contribution schemes are exploring default investment strategies that may offer better value for money to their members.

Factor investing is also increasingly pervasive across Europe. Our data show that the European factor investing market stood at €329bn (£298.4bn) by Q2 2017, having enjoyed annual growth of 20 per cent since the end of 2015.

DB pension funds now represent the largest portion of institutional factor-based assets. Factor strategies have seen a steady stream of inflows as both traditional active and passive equity managers have suffered outflows, particularly from DB schemes looking to derisk.

We have seen evidence of a shift in appetite towards multi-factor strategies

The factor investing universe is complex, and encompasses numerous different approaches. This allows institutional and retail investors alike to select products that can best suit their needs – varying from highly sophisticated active quant strategies to more transparent index-based products.

For many pension funds, factor investing sits somewhere between active and passive investing. For others it represents a means by which the equity portfolio (or the entire asset pool) can be viewed on a top down basis, to analyse the sources of risk and return across asset classes.

Some of the largest institutions, such as ATP in Denmark, have built in-house capabilities and gone so far as to use factors as the basis of portfolio construction in place of the traditional asset allocation approach.

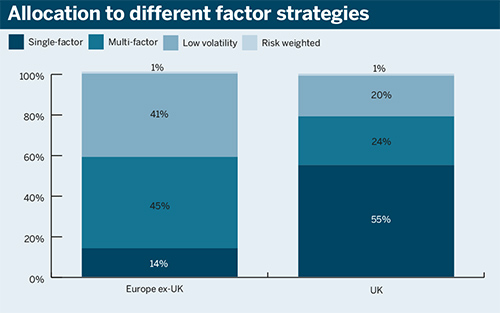

Single-factor still dominates DB

The UK DB market is substantially different to its counterparts in Europe, as can be seen in the first chart below.

The majority of UK DB factor-based assets are in single-factor third-party index strategies, with most of these strategies targeting the ‘value’ factor.

The relative simplicity of these strategies and resonance of value investing have led many to choose these products as a first foray into factor investing.

More recently we have seen evidence of a shift in appetite towards multi-factor strategies, with recent flow data suggesting that DB schemes have actually been moving out of single-factor strategies into more diversified products. Just over €3bn of UK DB scheme assets entered multi-factor equity strategies in the six quarters to Q2 17.

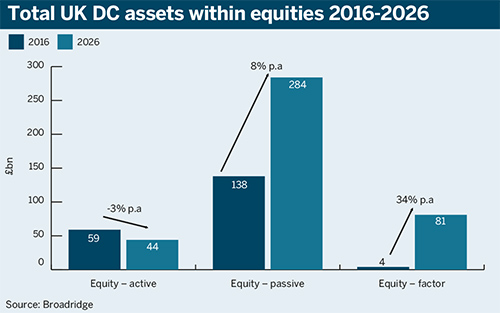

Factors overtaking active in DC

Factor investing is also starting to play a significant role in DC default investment strategies, and we expect this to grow significantly over time.

We expect that the total amount of UK DC assets invested through factor-based equity products will climb from £4bn to £81bn over the next 10 years.

In contrast, assets invested through traditional passive strategies looks set to grow at a slower rate, and the use of active equity investment is likely to continue shrinking.

The charge cap is a key factor behind this, with some schemes seeing factor investing as a means of capturing some of the benefits of active management at a fraction of the cost.

HSBC’s DC scheme moving its entire £1.85bn passive equity allocation to Legal & General Investment Management’s Future World Fund is one example of this trend.

Jonathan Libre is principal in the EMEA insights team at Broadridge