The FTSE 100 fell last week on the back of a High Court ruling that parliament must have a vote on the UK’s triggering of Article 50, while the Bank of England revised its inflation expectations upwards.

Schemes were urged to look past the short-term implications of a second ‘Super Thursday’ in less than six months, which included a marked spike in the value of sterling.

The surge was sparked by the news that Prime Minister Theresa May’s plans to enact Britain’s formal exit from the EU by the end of March 2017 have been dealt a blow by the Lord Chief Justice and two colleagues.

This issue of negative real yields isn’t going anywhere any time soon

Matt Tickle, Barnett Waddingham

The fall in the value of sterling over the summer benefited schemes with overseas investments who had not hedged their currency exposure. As the currency has begun to rise again, the corresponding decline in the FTSE 100 will see some schemes’ investments lose value.

Stay the course

James Walsh, EU and international policy lead at the Pensions and Lifetime Savings Association, said such movements would be unlikely to trigger strategic change.

“Pension schemes do take the long-term view, and this is why so many members have told us they are not rushing into changing their investment strategies in the wake of the Brexit vote,” he said.

“But that does not mean they can ignore current conditions; if a defined benefit scheme has a valuation coming up, then today’s market matters hugely.”

While political and economic uncertainty are not helpful for investors, Jon Dadswell, head of UK institutional sales at Columbia Threadneedle, also stressed that schemes should not be fazed by the news.

“Although many pension funds will be invested in FTSE 100 companies, these schemes are investing on behalf of their members for a prolonged period often spanning several decades so are not making investment decisions in response to daily market movements,” he said.

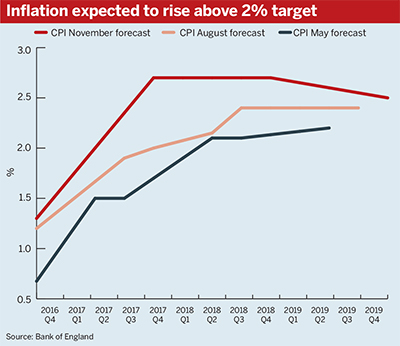

Inflation on the up

Short-term market movements could, however, feed into longer-term economic trends in the form of inflation, which is now expected to pass the BoE’s 2 per cent target by next spring.

“The Bank of England’s upward revision of its inflation forecast could prove to be welcome news for defined benefit schemes with a deficit, as a period of high inflation will help to close the gap between the company scheme’s assets and liabilities,” said Dadswell.

However, he said short-term inflation increases might not necessarily signal a prolonged period of heightened inflation.

Politicians in the driving seat

According to Matt Tickle, partner at Barnett Waddingham, the High Court’s decision on Article 50 had a greater impact on markets during what he called a second “Super Thursday”, in reference to the BoEs decision to cut rates in August.

In recent years, the bank has been largely responsible for stimulating growth in the economy. But there are growing concerns that quantitative easing and monetary policy have reached the limit of their use.

Brexit two weeks in: The legal and investment impact

Video: The UK's vote to leave the EU is having a major impact on markets and has created legal uncertainties. Partner at Allen & Overy Jane Higgins, and senior partner at Aon Hewitt John Belgrove, explain what schemes can do to position themselves well.

“Is there going to be this fundamental shift between fiscal and monetary policy?” Tickle asked.

If that shift does occur, schemes would have to take a considered approach to risk management, owing to the unpredictability of political sentiment and policy.

Chancellor Philip Hammond is known for being a fiscal hawk, but has reportedly told members of the Cabinet to expect a measured package of fiscal stimuli in the Autumn Statement.

Tickle said this approach would be important whatever the impact of last week’s events.

“This issue of negative real yields isn’t going anywhere any time soon,” he said. As such, any schemes leaving themselves unhedged should “take that decision in full knowledge of what that means.”