The majority of the 2.8m defined contribution savers eligible to access pension freedoms have not yet done so, new research has shown, as low financial confidence and high risk aversion stalls the freedoms.

Like many predictions about consumer behaviour, forecasts of the response to pension freedoms have not played out in practice.

Far from the rush on the coffers many anticipated, two-thirds of the 2.8m DC savers eligible to access pension freedoms are still investigating the new landscape, according to a recentreport from the Pensions and Lifetime Savings Association, ‘Pension Freedoms: No More Normal’ – a market-wide survey of who did what and why in the first six months of the pension freedoms.

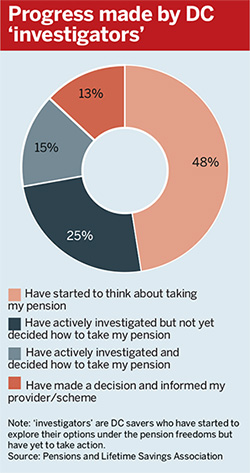

Nearly half (48 per cent) of this group, labelled the ‘investigators’, have started to think about how to access their pension but may struggle with their decisions as two-thirds lack financial confidence.

Despite this, in the course of assessing the options, just one in 10 have made use of the government’s Pension Wise guidance service.

Employers across the UK must be ready to guide their workforce through the complex new terrain; more than a third (36 per cent) of ‘investigators’ plan to turn to their employer for guidance.

No more normal

HM Revenue & Customs figures released this week on the number of flexible payments from pensions, which show a downturn in volumes paid out during Q4 – falling to £800m to 67,000 individuals, from £1,170m to 81,000 individuals in Q3 – but provide no breakdown on how individuals accessed their savings.

The PLSA report provides more granular detail on how savers have accessed freedom and choice, categorising the 2.8m individuals in the DC cohort according to their response during the first six months of pension freedoms:

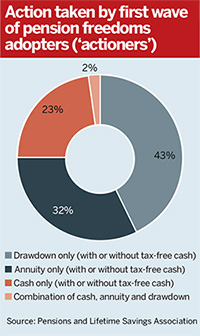

Actioners – 400,000 people have accessed their pension savings

Investigators – 1.75m people have not taken action but are assessing their options

Inactives – 630,000 have not taken any action

Compared with the larger ‘investigators’ group, the 400,000 ‘actioners’ have DC wealth well above average, access to other pensions already in payment and, in many cases, experience of self-invested personal pensions and income drawdown, but confusion persists within the group.

Speaking at the launch of the report, Jackie Wells, PLSA head of research and policy, said complex terminology had potentially confused ‘actioners’.

The timing of decisions is highly personal… only the individual knows that about themselves but needs help to understand and articulate it

Yvonne Braun, ABI

“People think they have bought an annuity but they haven’t,” said Wells.

Moving pieces

Yvonne Braun, director of long-term savings policy at the Association of British Insurers, said the current take-up of Pension Wise was “way too low” and a concerted effort to engage people earlier was very much needed.

“The timing of decisions is highly personal… only the individual knows that about themselves but needs help to understand and articulate it,” she said.

Braun said the industry could adopt a strategy similar to the NHS mid-life health check to drive up engagement, adding that the development of a pension dashboard or online portal will be a crucial step towards providing people with a more complete picture of their savings and financial position.

Greg McClymont, head of retirement savings at Aberdeen Asset Management, said the “extraordinary number of moving pieces” emerging in the new environment brought real challenges for the industry – particularly in developing products to meet savers’ needs.

“People are not acting in ways that fit down straight lines or categories. How do we put together a coherent view of what people are doing?” he said.

“We know that what people accessing flexibility want is a guaranteed income and flexibility… that leaves us with a challenge around the structure of drawdown multi-asset products – it’s more about preserving income than growth.”