The number of FTSE 250 executives taking taxable cash supplements instead of pensions has risen, according to a survey, as the way high-earners receive benefits has changed in light of lower lifetime and annual allowance limits.

Industry experts expect this to continue as changes from the Budget come into effect next year. Suspected further changes in pensions tax legislation, including another possible decrease in lifetime allowance, could transform the way high-earners save for retirement.

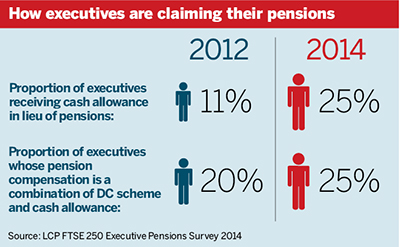

The report from consultancy LCP found the proportion of executives opting for cash in lieu of pensions rose to 25 per cent in 2014 from 11 per cent in 2012.

The report from consultancy LCP found the proportion of executives opting for cash in lieu of pensions rose to 25 per cent in 2014 from 11 per cent in 2012.

“That is very much triggered by the fact that we’ve got these new, lower annual and lifetime limits on pension compensation,” explained Mark Jackson, partner at LCP. While he expected this trend to continue, Jackson acknowledged that pensions still have a role to play in retirement savings.

“Those companies that are willing to put a little bit more effort into maximising their tax efficiency are the ones that are offering a combination of pension contributions and cash,” he said.

LCP’s survey found the proportion of executives who receive a combination of a defined contribution scheme and cash supplements rose to 25 per cent from 20 per cent. This change is largely attributed to the limited, but tax efficient, nature of DC schemes under the new legislation.

However, experts agreed there could be significant changes to pensions tax still to come, particularly with the prospect of a new government in 2015.

Looking ahead

Andrew Lewis, senior associate in law firm Hogan Lovells’ pension team, said a number of clients are looking ahead to further reductions in the lifetime allowance.

He added: “Some of the political parties have already started talking about more radical changes in areas like pension tax relief for higher earners, and employers and trustees will want to keep a close eye on how the policy debate develops over the next few months.”

There is a consensus that further reductions in the lifetime or annual allowances would see higher-rate earners moving away from reliance on pensions schemes and exploring flexible savings alternatives.

But Danny Wilding, partner at consultancy Barnett Waddingham, said reductions in allowances would have to be extreme to affect a widespread drop in scheme membership.

“As long as people are within the pensions tax relief limits, then pensions are still the single most tax-efficient savings vehicles… But as soon as people start to get caught by the limits, then yes, it would be natural for some of the current pensions savings to go into other vehicles in future,” he said.

Among the changes proposed are pensions minister Steve Webb’s call for the lifetime allowance to be scrapped, along with a flat tax relief rate of 30 per cent. The idea behind the proposal is to give less tax relief to higher-rate payers than they currently receive, and basic-rate earners would receive more tax relief on their contributions.

However, Jackson pointed out that there are incentives for higher earners.

He said: “They’ll get the extra flexibility and the extra scope to accumulate more pension savings if there’s no lifetime allowance.”

As the LCP report pointed out, a change in the flat rate of tax relief to 25 per cent could also be used to recover around £5bn for the Treasury.

But the political legacy of such a move may well focus on allowing higher-rate earners to amass large amounts of wealth in their pension funds.

Rosalind Connor, partner at law firm Taylor Wessing, said: “It can be quite an emotive thing, because it seems like a vast amount of money in one place, because people don’t tend to think of it as the money you’d need to fund the rest of your life.”

She said it may therefore be that the pensions reform which gains most traction is also one that is less disruptive, and does not affect the current combination of lifetime and annual allowances.

“My suspicion is… that if someone wants to mess with the taxing of pension schemes, they’re going to start taxing the tax-free lump sum, which you get at retirement,” added Connor.

She argued the sum, which was renamed the pension commencement lump sum in the Finance Act 2004, does not fit with the UK’s policy of taxing pensions on the way out, rather than during accrual.