Local authority schemes have rejected government proposals to mandate pooling assets into a passively managed common investment vehicle, but did see benefits in other suggestions put forward.

Among scheme managers Pensions Expert spoke to, most were against forcing schemes to invest in a common passive investment vehicle but welcomed ideas such as a collective vehicle to invest in alternatives.

The Department for Communities and Local Government’s consultation on ways local government schemes could cut costs and improve efficiency closed on Friday.

This proposed combining the Local Government Pension Scheme’s listed assets into a passively managed CIV to reduce investment costs. Another could be used to access alternative assets but would be actively managed.

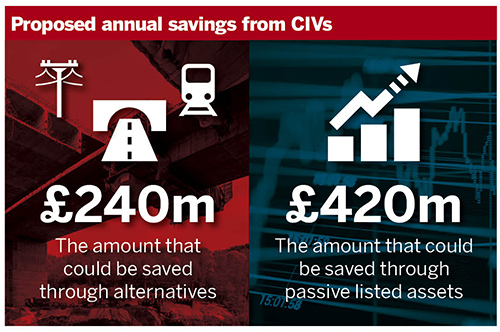

Research into the structure of the LGPS by public sector actuarial consultancy Hymans Robertson estimated the proposals could result in savings of more than £600m a year (see graphic).

Value for money

Chair of Islington Council’s pension fund Richard Greening said it was strongly opposed to the idea that all pension funds be forced to invest passively when some are generating better returns through active management.

“We’re part of the London CIV but before we invest in that we are going to carry out a value-for-money analysis to make sure that if we do move money into the CIV, whether it will actually benefit Islington’s pensioners, employers and taxpayers,” he said.

Schemes of the London boroughs have the opportunity to pool their traditional assets in a CIV. The CIV would be governed by a joint committee made up of scheme representatives.

Greening said Islington manages much of its large equity portfolio passively in-house and it costs very little. “It probably costs us less than the fixed cost of having the London CIV, for example,” he said.

However he said the scheme was interested in the government’s proposals for an alternatives CIV.

“We think that’s one of the most promising areas, we would like to get more exposure to things like infrastructure,” said Greening. “But the cost of doing that, such as due diligence, for a relatively small pension fund like ours is quite high.”

However Michael Johnson, research fellow at the Centre for Policy Studies, said schemes should be mandated to pool their listed assets into a passively invested vehicle.

“If you want economies of scale, what’s underlying the drive towards passive is that costs are controllable and the outcomes are not,” Johnson said.

Liz Woodyard, investment manager at Avon Pension Fund, also said while the scheme has a lot of passive investments, it does not believe schemes should be dictated to invest in this way.

“We don’t think what’s been put forward justifies it,” she said.

Peter Morris, director of pensions at Greater Manchester Pension Fund, said the scheme favoured non-mandatory CIVs.

“We’ll be coming down in the comply-or-explain camp and we’ll be flagging the importance of good decisions,” said Morris.

Risk and accountability

Mike Allen, head of pensions at the London Pensions Fund Authority, said while a small number of passively managed CIVs would create cost savings, forcing schemes to invest in single-asset CIVs could limit their ability to allocate assets in a way that manages risk effectively.

The LPFA instead favours an asset-liability management partnership structure, responsible for making allocation decisions and with access to multiple assets, but with a degree of local accountability built into governance arrangements.

“You could then start to make up asset allocation, you’ll have a clearer understanding what the funds’ liabilities are, you could have clearer data, you’ll have more control over local investments [and] you have a much closer link to local accountability,” Allen said.

Topics

- Alternative assets

- Avon Pension Fund

- Centre for Policy Studies

- Costs and charges

- Defined benefit

- Governance

- Greater Manchester Pension Fund

- Hymans Robertson

- Investment

- Law & regulation

- London Pensions Fund Authority (LPFA)

- Ministry of Housing, Communities and Local Government (MHCLG)

- Passive investment strategies