High street bookmaker Ladbrokes Coral Group has appointed a single trustee board for its pension plans following a company merger, a move experts say can improve efficiency and consistency.

Companies with more than one scheme are increasingly seeking to make scheme management more efficient: Lloyds Banking Group merged the trustee boards of three of its defined benefit funds in 2016.

You just double the work if you’re negotiating with two trustee boards

Richard Butcher, PLSA

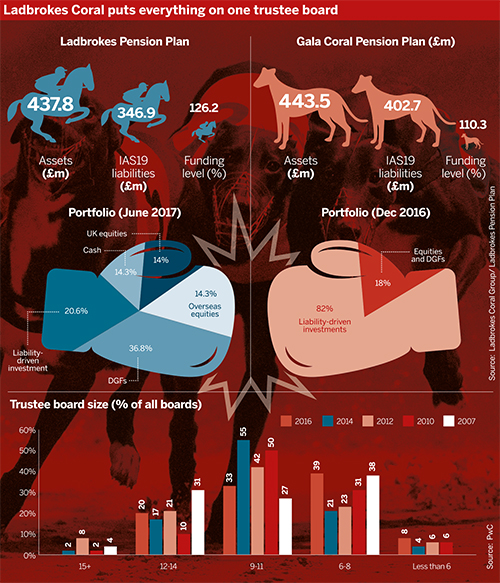

The merging of the Ladbrokes Pension Plan and the Gala Coral Pension Plan was driven by a change of sponsor. In November 2016, Ladbrokes merged with certain businesses of Gala Coral Group. The group has since agreed to be bought by online gaming company GVC Holdings.

Merger prompts trustee board changes

Following the merger, the company decided to appoint a single trustee board to oversee the governance of both defined benefit schemes.

A January newsletter for members of the £440m Ladbrokes Pension Plan said: “As a consequence of the corporate changes, there has also been considerable change on the trustee board.”

A combined member-nominated director policy, dated January 2018, explains that “this will enable the members of both plans to benefit from having a larger trustee board with the resources and expertise to manage the running of the plans”.

A trustee company, Ladbrokes Coral Group Pension Trustee, will act as trustee for both schemes.

The new board is made up of six trustee directors, including one independent professional trustee who acts as chair, three company-appointed trustee directors and two member-nominated trustee directors.

Consistent and efficient

Richard Butcher, managing director of professional trustee company PTL, could see two advantages to having a single trustee board.

“One is consistency, and the other is efficiency,” he said, adding that “you just double the work if you’re negotiating with two trustee boards”.

Multiple trustee boards reach different conclusions. Having a single view is important when considering the strength of the employer covenant, for example. “It’s a more consistent approach,” he said.

Butcher added: “There is a theoretical conflict of interest, which is that you could favour the funding of one scheme over the other”.

However, he said that in practice, the fact both schemes will be represented on the board means individual conflicts will tend to cancel each other out.

Sometimes, creating a single trustee board for multiple schemes can be a first step towards merging the pension plans – a move that would further improve efficiency and could be a step in the direction towards consolidation.

“Once you’ve unified the governance function, you can look at unifying the advisory and service provider functions, then you can look at unifying the funding process,” said Butcher.

Single board can secure sponsor engagement

Alan Pickering, chairman of Bestrustees, said that when merging two trustee boards into one, “you don’t want to double the size of a trustee board”.

Pickering said it might be sensible to reduce the number of company-nominated trustees immediately and to have a staggered process for member-nominated trustees – reducing the number over time to end up with a manageable board.

HP sets up trustee company in simplification push

The Hewlett Packard Limited Retirement Benefits Plan changed the structure of its trustee board to a trustee company, in a move to simplify processes while increasing scrutiny of trustee actions.

The chair of trustees has an important role in making sure there is a “degree of togetherness”, Pickering noted. He suggested a training event for trustees of the multiple schemes “so that they can each understand the differences and similarities” of each scheme.

With a single trustee board, “you get the economies of scale” and “it just makes the whole operation slicker, and will hopefully secure the continued engagement of the plan sponsor and senior people within the plan sponsor” Pickering said.

He added: “The slicker you make the whole governance operation, the more likely it is that the plan sponsor will remain engaged and will be willing to pay contributions, knowing that a greater part of those contributions are going to pay benefits and to pay running costs, because the running costs are being reduced because of efficiency.”