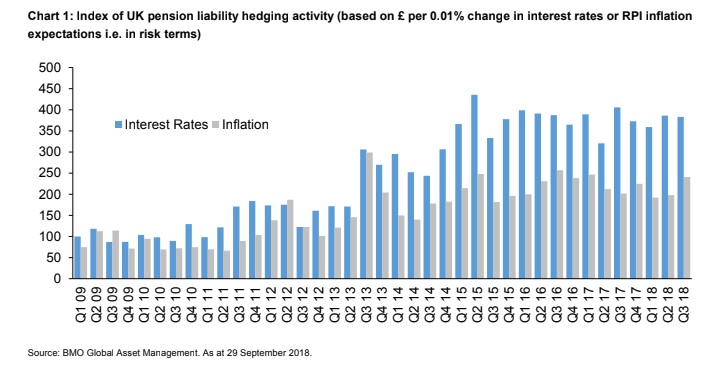

On the go: Inflation hedging has seen a sharp rise with activity up by 22 per cent in the third quarter of 2018, to around £24.2bn. Total interest rate hedging activity was around £29.2bn in the third quarter, a 1 per cent fall according to the BMO Global Asset Management.

Its Q3 2018 LDI survey, which polled 14 investment bank trading desks on the volumes of quarterly hedging transactions, revealed the main theme of the quarter was a high level of buyout activity, which led to switching from gilts to swaps.

New outright hedging by pension funds tended to be implemented via leveraged bonds.

Rosa Fenwick, LDI portfolio manager at BMO Global Asset Management, said: “The buyout activity highlighted an interesting point for pension schemes. Most schemes value their liabilities using gilts.

“While insurers will usually accept gilts as part of a bulk annuity deal, this is simply because they are more fungible than swaps. An insurer’s discount curve is explicitly linked to Libor, so the insurer will subsequently switch from gilts to swaps.

“This in turn supports the argument that schemes should be agnostic between hedging using gilts or swaps.”

Latest figures from the Pension Protection Fund showed that funding levels of pension schemes improved over the period, with the average funding ratio at 97.7 per cent as at the end of September compared with 94.9 per cent at the end of June.

Inflation expected to fall

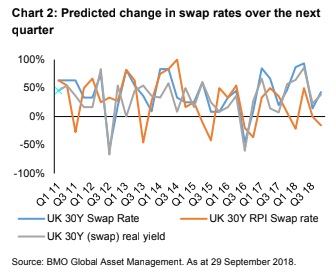

Investment bank derivatives trading desks were also questioned on the likely direction of key rates for pension scheme liability hedging. More bank counterparties expect long-term real and nominal rates to rise rather than fall whereas more expect inflation to fall rather than rise. The House of Lords Economic Affairs Committee inquiry into the use of the retail price index as a measure of inflation has the potential to have a significant impact on pension funds, whether in terms of the assets that they hold or in the benefits they will pay out.

Bank counterparties were polled on their views on how this process may pan out. The majority believe improvements will be made to RPI so that continued publication is supported, combined with increased usage of the consumer price index and consumer price index including owner occupiers’ housing costs, known as CPIH.

Around a quarter think there will be no change to RPI, and none believe there will be a restatement of RPI as CPI plus a spread, or a cessation of RPI publication and a wholesale switch to CPI or CPIH. “The arguments against the cessation of RPI publication are many and varied. Such a move would likely lead to legal challenges and market disturbance, particularly as the CPI and CPIH markets are not sufficiently developed or liquid to take the burden of RPI supply and demand overnight,” Fenwick said.

“It appears more likely that the House of Lords committee may suggest improvements to the formula in combination with encouraging a gradual shift towards CPI and CPIH usage.”