Defined benefit schemes are showing increased interest in illiquid alternatives as they hunt greater yield and diversification, but many lack sufficient resources and the confidence needed to execute such investments.

Helen Roberts, lead investment policy adviser at the National Association of Pension Funds, said there is “definitely more appetite” among DB schemes to lock up a greater proportion of their assets in order to gain extra yield.

Roberts said assets “that have any inflation linkage, have a yield that is greater than you get with government bonds and anything that has income-generating growth, all that is very wanted by pension schemes at the moment”.

But she added that while the illiquidity premium was a draw, schemes feel they cannot allocate too much into them as “you’re locking up your portfolio for quite a long time”.

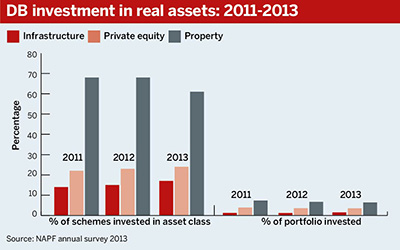

Most DB schemes typically allocate between 3 and 5 per cent of their portfolio to illiquid assets such as private equity, infrastructure and real estate, depending on the scheme’s level of maturity, consultants said.

However, they added that most schemes still have the capacity to invest further in these types of asset classes without facing liquidity constraints.

Tim Giles, partner at consultancy Aon Hewitt, said some trustees “miss the actual cost [of favouring] liquidity” by not adequately considering the illiquidity premium on offer.

People should be thinking ‘What loss of return am I prepared to suffer at the moment to make sure my assets are liquid?’

Tim Giles, Aon Hewitt

“People should be thinking, ‘What loss of return am I prepared to suffer at the moment to make sure my assets are liquid?’,” he said.

Le Roy van Zyl, principal in consultancy Mercer’s financial strategy group, agreed schemes have the ability to invest further in illiquid assets but are held back due to the complexity of accessing investments and insufficient knowledge among trustees. “[For] certain boards of trustees, it takes them a while to make sure they have all the training,” he said.

The London Pensions Fund Authority’s allocation to illiquid assets has bucked the trend, however, and can be anywhere within a 25-35 per cent bracket, a spokesperson from the fund said, though this figure could change depending on the scheme’s ability to meet its liabilities.

“Our position as a long-term investor with stable employer covenants means we have a high tolerance for illiquidity and so can make significant investments of this nature,” the spokesperson added.

Barriers to entry

It can take time for investors’ money to be drawn down and fully invested – for example, in private equity or infrastructure projects – as managers need to wait for suitable opportunities to arise.

LDI v locking in

Pension funds are looking at alternatives to liability-driven investment strategies, as they look to derisk amid a backdrop of historically low yields.

LeRoy van Zyl, principal in Mercer’s financial strategy group, said cost was a significant factor influencing schemes’ migration towards alternative risk-reduction strategies.

“A lot of [LDI strategies are] expensive, or perceived to be expensive,” he said.

MandateWire data from Q2 this year demonstrate that investments in alternative asset classes have been popular with pension schemes, with almost twice as many alternatives mandates were awarded (50) than either equity (27) or fixed income (26).

Nick Horsfall, senior investment consultant at Towers Watson, said: “The economic rationale for those is they’re much more illiquid and/or much less secure”, but he stressed the importance of “assessing what you think your liquidity needs [are]” from the outset.

Horsfall added that because alternatives are best suited to schemes more than 10 years from full funding, interest for these strategies may wane as schemes move closer to this point.

Van Zyl agreed, adding that the flexibility of LDI for schemes closer to legacy makes it a more attractive option. “Even the schemes that are doing alternatives will still be doing LDI as well,” he said.

Frances Hudson, global thematic strategist at Standard Life, said: “Pension funds might have scope for investing in alternatives but it might never invest up to the limit because the opportunities might not be there.”

Some investors have also cited as a barrier the inability to easily construct a benchmark to compare individual managers’ performance, making it harder to monitor investments in alternative assets.

Roberts said the government’s decision to allow transfers from private DB schemes to defined contribution funds could also mean schemes need slightly less long-dated assets as the duration of schemes shortens as a result.

“They may also need cash more quickly to pay the cash lump sum,” she added.

Access points

Giles said infrastructure debt is an area where there are potentially good investment opportunities for schemes.

“But we are still nervous around timing, that there might be better timing to come because of pressures surrounding that market,” he said.

Anthony Fasso, chief executive and international head of global clients at AMP Capital, said smaller schemes and those less experienced in investing in real assets could be more suited to liquid instruments such as global listed infrastructure securities.

“[These are] more closely correlated with equities but they do provide many features similar to infrastructure,” he said.

Additional reporting by Angus Peters