The UK's vote to leave the EU has led to a difficult cycle for real estate, so should trustees be concerned about their UK property holdings?

After the referendum result in June 2016, the only certainty was that the country was due to embark on a period of uncertainty, in the run-up to the March 29 2019 Brexit deadline.

Allocations to international could, and certainly should, increase over coming years

Peter Hobbs, bfinance

Pensions experts were quick to point out that, while the outcome is unclear, trustees should avoid making any drastic investment decisions.

Nonetheless, the UK’s departure from the EU is perceived more and more as an investment risk by defined benefit trustees.

Earlier this year, professional trustee company PTL’s DB survey found that Brexit investment implications rose to second from third in the concerns of trustees, growing to 13.8 per cent of votes from 11 per cent in September 2017.

One particular area of investment uncertainty is real estate. The average pension scheme allocation to property in the UK stands at 3 per cent, according to Mercer.

But with Brexit on the horizon, what does this mean for UK pension funds invested in domestic real estate? And how will pension scheme investment change over the next few years, following the UK’s departure?

A 2017 KPMG survey of 60 real estate investors from 45 institutions across 23 countries revealed that nearly half of respondents intend to continue with the same level of investment in UK property following the triggering of Article 50.

Forty-four per cent said their organisation is likely to slow down investment, while 10 per cent said they expected to stop investment altogether.

UK property yields still low

Peter Hobbs, managing director and head of private markets at consultancy bfinance, notes that the UK real estate market is at a difficult stage of its cycle.

“Yields fell steadily in the years since the financial crisis to reach historic low levels in many sectors and parts of the country,” he says.

“This aggressive pricing exists at a time of heightened uncertainty over the economic and property market outlook, mostly related to the uncertainty over Brexit.”

Hobbs adds that the consensus expectation is for weaker performance over the coming two to three years, due to weak rental growth and a rise in yields.

Beyond this, some see continued potential for the asset class.

Simon Cohen, chief investment officer at Dalriada Trustees, says: “There’s the potential there for a short-term blip around property because of Brexit, but in the medium to long term, I still rate property as an investment as somewhere where pension schemes in particular want to be invested in.”

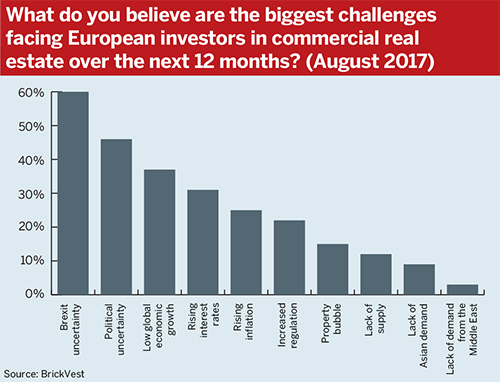

Online real estate investment platform BrickVest found in July that the UK remains the favourite destination of commercial property investors, with 29 per cent preferring it to other countries in Europe.

Phil Clark, head of property investment at Kames Capital, notes that commercial real estate has a relatively low correlation to other asset class returns, “making it a good portfolio diversifier”.

With regard to Brexit, he says that “commercial real estate is typically much less volatile than listed markets, and the lack of over-development in the build up to the global financial crisis means that supply and demand are relatively in balance”.

However, Clark adds that “the structural change in the retail sector to online sales from stores means some secondary shopping centres in particular will suffer”.

At the same time, the industrial sector and distribution warehouses in particular are benefiting from this structural shift, according to Clark.

Some pension funds have increased their exposures to property over the past few years, “attracted by the historically high rental income yield relative to gilts”, Clark notes.

Should schemes go global?

The UK real estate market makes up a small percentage of the investable global real estate market. If schemes are solely invested in domestic property, does this mean they are missing out on a broader opportunity set?

Despite its maturity, real estate has tended to possess a significant ‘home bias’, with many investors historically just investing in their domestic markets, Hobbs highlights.

“But one of the great benefits of real estate as an asset class is international diversification, as real estate markets tend to move in different ways across countries and regions, far more so than public equity markets,” he says.

The benefits of international diversification are starting to be better understood, according to Hobbs, alongside the growth of robust investment platforms increasingly operating on a global basis.

“As always, great care needs to be taken when selecting appropriate managers, ensuring they have the capabilities, discipline and alignment to avoid potential mistakes,” he says.

“The combination of these factors coupled with the uncertainties facing the UK market suggest that allocations to international could, and certainly should, increase over coming years,” he adds.

Clark notes that the fallacy of global investing is that overseas markets require a higher risk premium than local markets, “which in reality is rarely on offer”.

“The key risk is currency, which can be hedged,” he says.

Investors earmark residential investments

There has also been an increased interest from pension schemes in residential property, according to Cohen.

The Investment Property Forum has found that the fundamentals of the residential market, such as a lack of supply, are still seen to make it attractive – particularly against other sectors such as City offices.

IPF research published in January showed that institutional investors have earmarked just over £8bn for residential investment.

Another option to pension funds is real estate debt. “Typically, you’re investing with a manager which is holding other forms of debt within that portfolio,” on a pooled fund basis, Cohen says, predicting that this type of investment will become more popular among schemes.

Jon Rickert, investment director of GAM’s real estate finance team, explains that real estate loans are typically advanced at a level well below the value of the underlying property collateral.

“A decline in property values does not necessarily mean the lender will incur a loss,” he says.

He adds that real estate loans generally pay a fixed rate of interest, whereas income from direct property investments is usually variable.

“If tenants break their leases the income from the property will decline, but the interest paid on a well underwritten loan should remain constant,” he adds.

Rickert stresses that the impact of Brexit is still unknown, but adds that the referendum improved the lending environment, with banks having adopted even more restrictive lending standards.

“Loan-to-value ratios have come down and lending margins have stabilised and in some cases increased relative to 2014,” he says.

“Regardless, a pan-European approach to loan investments is critical,” Rickert says, adding that investments in euro markets are a helpful risk diversifier. “While volumes in the UK have slowed, opportunities in euro markets have increased.”

Property set to grow in DC

Brexit aside, scheme exposure to real estate is likely to grow. Broadridge Financial Solutions research carried out for the IPF found that property investment in defined contribution schemes will grow, but that barriers remain, such as lack of liquidity.

Broadridge forecast that the percentage of DC schemes invested in property will rise from 30 per cent to 40 per cent over the next 10 years.

“DC allocations to property have tended to be low compared with DB plans, mainly due to the relative illiquidity of the asset class,” says Hobbs.

“Although much of the asset class is relatively illiquid, there is an increasing range of liquid real estate options that provide daily liquidity and pricing making them suitable for DC plans,” he says.

“As these options increase, DC allocations are set to rise. This is likely to include traditional UK real estate but also a range of niche sectors such as student housing and healthcare, and increased exposure to global real estate,” he adds.