From the blog: Good governance is the bedrock of a properly functioning trustee board. However, it is evident that trustees are struggling under a governance burden, which stems from the need to comply with increasing legal requirements and ever more Pensions Regulator publications.

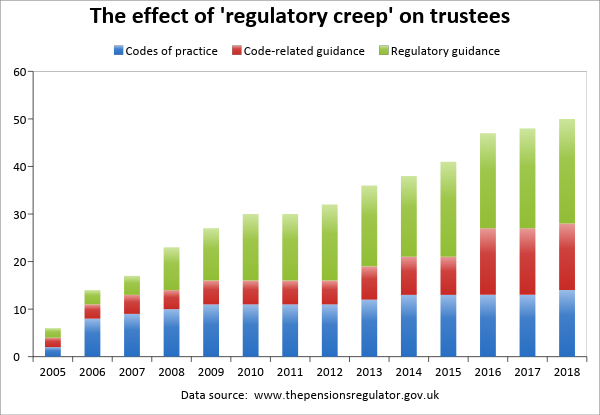

While we regularly get new law and guidance, we rarely see it removed. The table below shows the incremental increase in the regulator’s codes of practice, code-related guidance and regulatory guidance since 2005.

The result, over time, is a ‘regulatory creep’ that has burdened trustees with no fewer than 50 different TPR publications (the table doesn’t even include the regulator’s other types of guidance, quick guides, statements or the trustee toolkit modules).

Trustee board meetings should be strategic. Much of the detail, including compliance steps, can be delegated to sub-committees

This takes already limited trustee time away from the issues that really matter, in particular: strategy, investment and proper engagement with members.

However, trustees can follow a blueprint for easing regulatory overload by making changes to their approach to governance in three main ways.

Demand more from trustee advisers

Are your lawyer, actuary, investment consultant and secretary giving you short, punchy and clear briefing papers? Have the trustee actions been flagged clearly?

Trustees should not get bogged down by badly presented information. Is the information you are getting relevant to your scheme and is it relevant right now? A trustee board meeting is not the best time to sit and listen to lengthy ‘general interest’ briefings.

Trustees should not get bogged down by badly presented information. Is the information you are getting relevant to your scheme and is it relevant right now? A trustee board meeting is not the best time to sit and listen to lengthy ‘general interest’ briefings.

Be strategic

Trustee board meetings should be strategic. Much of the detail, including compliance steps, can be delegated to sub-committees and, where appropriate, advisers.

Give enough thought to the order of the meeting, dealing with the most important issues first, when you have the time and the brainpower to deal with them.

Admin can wait until the end of the meeting. Get your relevant advisers to the strategic sessions too. They can flag the pertinent issues for your priorities early on in the process and help save time and cost in the long run.

Keep a member focus

The pensions world has changed a lot in recent years. Are members clear on what their benefits actually are and how they can take them? Do members know about the pensions freedoms? Are they aware of their transfer rights and the time limits for requesting a transfer? Have you made thoughtful decisions on what you should say to members, and how you should say it?

Just as importantly, have you thought about what you shouldn’t say? I am seeing a number of member complaints based on a failure to provide members with timely, accurate and clear information. This may be a good time for trustees to refocus on their membership.

Stephen Richards is a pensions partner at law firm Stephenson Harwood