The European Insurance and Occupational Pensions Authority has advocated the creation of a standardised framework for risk assessment and transparency in EU pension funds, quashing long-running fears of a shift to more stringent solvency funding requirements.

The UK pensions industry breathed a sigh of relief this week as Eiopa published its recommendations for a common risk management framework for Institutions for Occupational Retirement Provision across Europe, closing a chapter on three years of stress tests and quantitative assessments across EU pension funds.

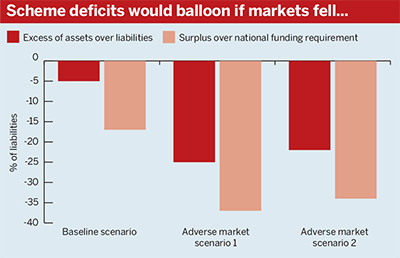

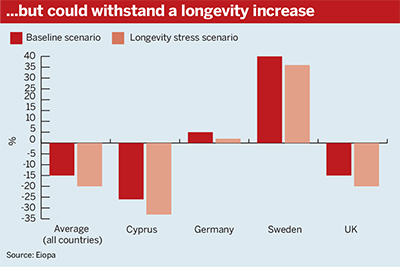

Results from the latest round of stress tests, conducted towards the end of 2015, showed schemes are vulnerable to both a drop in asset prices and an increase in technical provisions liabilities caused by persistently low interest rates, creating fear among industry stakeholders that a move to the dreaded holistic balance sheet and strict solvency requirements was on the cards.

Eiopa figures for the holistic balance sheet show that a move to a solvency-based system would increase the combined deficit of UK defined benefit schemes to €967bn (£770bn) – from €318bn under the current regime.

News that Eiopa is backing away from plans to harmonise capital or funding requirements will therefore be a welcome development, although the proposed standardised risk assessment, used to calculate the impact of common, predefined stress scenarios on pension funds, will be an extra hurdle for trustees and actuaries across the UK.

U-turn

François Barker, head of pensions at law firm Eversheds, said Eiopa has consistently advocated harmonising capital or funding requirements around the holistic balance sheet, and that the move away from solvency funding has put a multi-billion euro question “on the back burner”.

However, Barker questioned the value of the standardised framework favoured by the regulator, due to the variance of scheme size and structure across member states.

It’s another measure of pension scheme risk to add to two or three others – it could make things worse, not better

Francois Barker, Eversheds

“Pension schemes across Europe come in so many shapes and sizes… it may not actually be easy to compare apples with pears,” he said. “It’s another measure of pension scheme risk to add to two or three others – it could make things worse, not better.”

With a plethora of risk measures already at their disposal, schemes may struggle to tackle risk, Barker said.

“Arguably the more measures you’ve got, the harder it becomes to tackle [risk] – anyone can choose any number to suit their purposes.”

Sue Tye, of counsel at law firm Baker & McKenzie, said schemes will have to comply with legal duties handed down from the European regulator to be implemented on a national basis but questioned how they will communicate changes to members.

“The last thing you want to do is alarm members,” she said. “We have already been dealing for a good number of years about the buyout basis for funding of the scheme… but we just want to be clear about the level of prescription… and use of information going out to members.”

Joanne Segars, chief executive of the Pensions and Lifetime Savings Association, said the new requirements would add €210m (£167m) a year to costs and would “cause unnecessary confusion without delivering any benefit to scheme members”.

Brexit scenario

The advent of the EU referendum later this year could add a curveball to the development of Eiopa's regulatory regime, should the UK decide to leave the EU.

Hugh Nolan, director at consultancy Spence & Partners, said the outlook was entirely uncertain but that a Brexit scenario would mark the end of Eiopa’s interest in UK pension schemes.

“It seems to me at the moment they’re concerned that our pension schemes are funded differently,” he said.

“But then no other country has the same DB liability that we’ve got, so it’s unfair to [impose] a different standard when the trust-based system has worked fairly well for us for 100 years.”