Plumbing products supplier Wolseley UK is working to battle a climbing opt-out rate, reflecting the challenge of keeping new joiners in workplace pension schemes despite attractive terms.

Early auto-enrolment figures showed large employers enjoyed better than expected initial retention in workplace saving, with retailer John Lewis’s 5 per cent opt-out rate a typically low figure. But scheme managers have predicted these proportions would rise as contributions increased and communication campaigns faded.

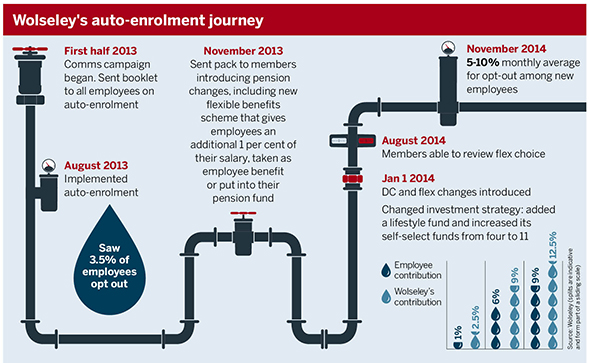

Wolseley originally saw a 3.5 per cent opt-out rate when auto-enrolling in August last year, but this has since increased to a monthly average of 5-10 per cent (see graphic).

To combat the upward creep, Wolseley has planned a communication campaign over the next two months to remind non-members of the benefits of the scheme, and is currently planning how to engage future new joiners before they are auto-enrolled.

Neil McCawley, head of rewards and benefits at the company, which has 6,200 staff, said he thought the increase in opt-outs was partly due to the age demographic of new starters.

“Many are younger employees who aren’t sure they want to join a pension scheme at that point in their career,” he said.

During the staging process there was widespread government and media campaigning about the benefits of pensions saving, yet new employees will not have been exposed to the same level of information.

“When we do the first re-enrolment of our opted-out employees in May-June 2016 they will have been employed by us for at least three years. I would expect, at this point, that fewer people will choose to opt out again,” added McCawley.

Improving adequacy

Wolseley has been awarded the National Association of Pension Funds’ Pension Quality Mark Plus due to a contribution structure that, at its highest levels from both employer and employee, approaches almost a quarter of a worker’s pensionable salary.

Industry experts said that such high levels of saving would be more likely to deliver the two-thirds of salary required to achieve a comfortable retirement, but stressed that communication remained a crucial part of delivering the scheme to employees.

“Even fabulous parties need fabulous invitations,” said Adrian Boulding, pension strategy director at insurer and pension provider Legal & General, and chairman of the PQM. “If [employees] don’t take up employer contributions, it’s free money they’re losing if they’re opting out,” he said.

Industry observers suggested low contribution rates could even provide a disincentive to save.

Jamie Clark, business development manager at insurer Royal London said some employees may see little value in contributing just 1 per cent of their salary and that ongoing communication and education was necessary to help assist employees’ pensions decisions.

He said: “[It] could be psychological – although it will increase over time; the here and now seems very minimal.”

Wolseley also runs a flexible benefits programme providing employees with an additional 1 per cent of salary, taken either as pension or another employee benefit.

McCawley said: “This was something new for employees – we wanted to overcome the cost-of-joining barrier for our employees.”