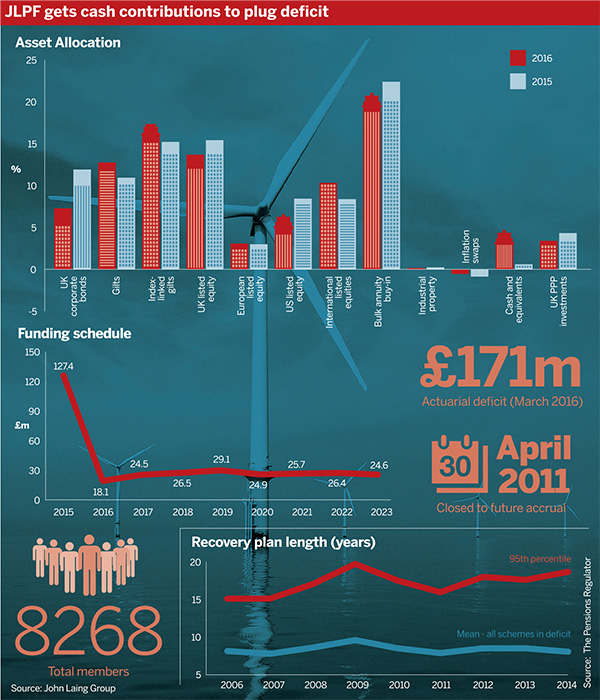

The John Laing Pension Fund has agreed a recovery plan worth £171m to be paid over seven years by its sponsor, infrastructure investor John Laing, following an actuarial valuation.

While average recovery plan durations have been steady in recent years, trustees increasingly have to tackle a double-edged sword on funding, where both strong and weak employers can justify longer recovery plans.

There’s a bit of a mindset issue around companies and trustees who believe we’re in an extraordinary market situation that will resolve in time

Charles Cowling, JLT Employee Benefits

An actuarial valuation of the JLPF as at March 2016 revealed a technical provisions deficit of £171m, equating to a funding level of 85 per cent.

That year also saw John Laing’s accounting deficit across its two schemes grow to £61.3m from £38.9m.

“The deficit (under IAS 19) has increased from last year primarily due... to the lower discount rate and higher long-term [retail price index], partly offset by cash contributions to JLPF of £18.1m,” concluded the company’s full year results.

In response, John Laing has promised to repay the technical provisions difference in seven years, with annual total payments ranging between £24.5m and £29.1m in cash.

Are long recovery plans a problem?

John Laing’s commitment to paying off the deficit relatively quickly is in contrast to a growing tail of schemes with far longer horizons. Recovery plans in the 95th percentile grew from 15 years in 2005 to 18.7 years in 2014, the regulator’s figures show.

A significant portion of these longer recovery plans have been driven by issues of affordability, said Charles Cowling, director at consultancy JLT Employee Benefits.

“There’s also a bit of a mindset issue around companies and trustees who believe we’re in an extraordinary market situation that will resolve in time,” he said.

While he accepted that phenomena such as quantitative easing have contributed to unusual market conditions, he was concerned that interest rates might not lift as quickly as some expect, meaning scheme funding needs would remain high.

Cowling suggested that a change in regulation to allow employers to recover surplus might alleviate concerns about overfunding schemes, and could be used by regulators to demand more aggressive funding strategies.

Cash funding a liability estimate, which may turn out to be excessive, in one payment would be “a waste of capital” from the company’s perspective, said Hugh Nolan, director at consultancy Spence & Partners and president of the Society of Pension Professionals.

But he was against the idea of relaxing surplus rules, saying the priority should be getting schemes to buyout: “Only at the point where you could secure the benefits would you want to let them get some money back.”

Longer recovery plans and underfunding, he said, might not be a bad thing as long as security can be provided in the form of contingent assets.

Asset-backed base

Alternative sources of funding have been instrumental in propping up the JLPF’s financial position. In 2015 the company contributed £127.4m to the pension scheme, comprised of cash, shares in the John Laing Environmental Assets Group, and public-private partnership assets.

Henderson agrees recovery plan after funding fall

Investment manager Henderson Group has agreed a recovery plan with its trustees after its defined benefit scheme fell out of surplus at the latest triennial valuation.

“The Company has guaranteed to fund any cumulative shortfall in forecast project yield payments for some of these PPP investments up until 2017, but considers it unlikely that a net shortfall will arise,” the report noted.

Trustee boards will always prefer to receive cash when undertaking funding negotiations, according to Matt Harrison, managing director at covenant specialist Lincoln Pensions.

However, he said it was unlikely the group could afford to pay such a significant sum in cash. While the scheme investing in the same assets as the company would increase risk, he said the trustees would have weighed this against the lower cash alternative.

“There’s a secondary market in PPP products, so they could be sold,” said Harrison. “Also, pension schemes generally quite like infrastructure assets like these.”