Data Crunch: Corporate defined benefit schemes have been shifting allocations away from equities as a means of reducing funding volatility and focusing on assets that can deliver contractual cash flows.

Yet many underfunded schemes still require growth, and the existence of defensive or income-focused equity management styles may mean that equities will not disappear completely from DB investment portfolios.

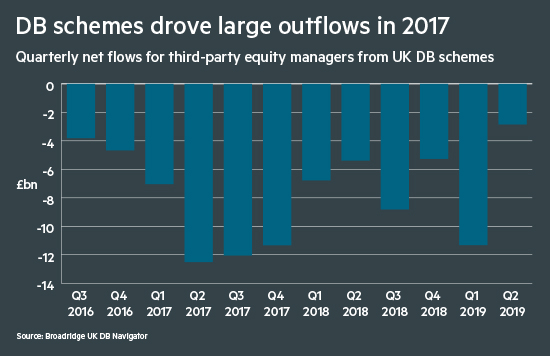

This movement out of equities has been large and persistent. In the two years to March 2019, schemes pulled more than £70bn of allocations from third-party equity managers, both active and passive.

One key reason behind this is that as schemes mature, they become more focused on matching liabilities and much less tolerant of equity market risk – liabilities are generally discounted relative to gilt yields, not expected equity returns.

Factor investing can reduce exposure risk

It should be noted, however, that there are several ways in which schemes can reduce their exposure to equity market risk without necessarily selling out of equities.

Within the long-only space, risk-weighted and low-volatility equity strategies aim to deliver a smoother return profile than traditional approaches. The recent growth of factor investing has made these approaches more prominent, and they are indeed popular in other European pensions markets, such as in the Netherlands and Germany.

It is also possible to use derivatives strategies such as collars to reduce downside risk in equity portfolios. These approaches have gained popularity among Local Government Pension Scheme participants keen to lock-in their funding positions ahead of last year’s valuations. Equity derivatives are also increasingly commonplace within the liability-driven investment portfolios of private sector schemes.

Certain asset managers have established long/short approaches that can provide some of the alternative return sources from equities while reducing exposure to equity market beta, especially in market downturns.

Examples include absolute return equity managers, who aim to provide positive returns through all market environments, and alternative beta managers, who use systematic approaches that seek to deliver returns through targeted exposure to specific factors – such as value or momentum – that are exhibited by different stocks.

Negative cash flows drive schemes to sell

A second driver of the sell-off has been due to schemes turning cash flow negative and therefore moving into assets such as bonds, which can deliver contractual income streams. It should be remembered, however, that many stocks pay regular, reliable dividends and, with a large number of schemes still being underfunded, equity income approaches can also offer growth potential.

Data from the Pension Protection Fund’s Purple Book shows that even the most solvent and mature pension schemes hold an equity allocation of approximately 10 per cent on average, and these defensive and income-generating strategies perhaps make it easier for these schemes to maintain that exposure.

The net outflows show little signs of abating, but given that equities remain such a significant part of the investment opportunity set, it would be disappointing to see this asset class disappear completely from scheme portfolios.

Jonathan Libre is principal in the Emea Insights team at Broadridge