On the go: Almost three out of every four defined benefit schemes in the UK are now cash flow negative, according to consultancy Mercer’s 2019 asset allocation survey.

The closure of many DB plans to future accrual makes increasing net cash outflows inevitable, but Mercer’s survey shows the speed at which this change is taking over. Where 66 per cent of schemes paid out more than they received in contributions in 2018, that figure has now risen to 73 per cent.

Evidence from the survey shows that huge numbers of schemes may be taking a risky approach to funding these increasing payouts.

Despite warnings over the risk of having to sell growth assets at inopportune moments and huge marketing efforts by managers of cash flow-driven investing strategies, only 9 per cent of schemes have adopted a matching fund to navigate their run-off. Ninety-one per cent will use divestment to fund cash payments, while 48 per cent of schemes will attempt to distribute income from their investment mandates where possible.

Having a robust, coherent plan in place for the DB endgame journey will be the best defence against any intervention from the Pensions Regulator

Nick Griggs, Barnett Waddingham

Matt Scott, investment consultant at Mercer, said: “Strong equity returns in 2017 and rising yields in 2018 have helped many DB plans move closer to their endgame. Investors should consider developing a strategy to meet cash flows to avoid relying solely on disinvestment, which can be complex and expensive.

“We believe that cash flow-matching techniques, where portfolios are specifically designed to align income and principal receipts, will be more widely adopted in the coming years as DB plans continue to mature.”

Source: Mercer

If UK trustee boards do not appear to have adopted formal CDI strategies, they are still focusing on broader de-risking, with 68 per cent of the market planning to de-risk over the next decade. The majority of schemes do not have formal triggers for this process.

Bulk annuity insurance also appears to be growing in popularity as a long-term objective. Some 27 per cent of schemes are targeting buyout, up from 24 per cent last year. Thirty-nine per cent say they still see self-sufficiency as their target, with full funding at a gilts plus 0.5 per cent discount rate the most common measure.

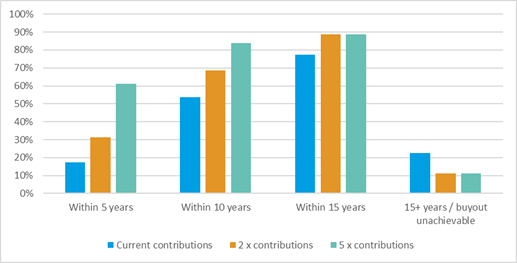

However, further analysis by Barnett Waddingham suggests an even greater proportion of the DB market could hand over liabilities to insurers.

More than half of FTSE 100 companies will be adequately funded to move to buyout in the next 10 years, it found, while one in five will be able to afford a transfer in the next five years.

Source: Barnett Waddingham

Profits and shareholder distributions have continued to rise among the UK’s blue-chip companies while contributions have remained flat, Barnett Waddingham found, leading it to suggest that with an extra 6 per cent of profits diverted to pension funds, 30 per cent would be ready for buyout in the next five years and 70 per cent over the next decade.

Nick Griggs, head of corporate consulting and a partner at Barnett Waddingham, said: “Following record dividends and recovering profits, many companies will also be coming under increasing pressure from the Pensions Regulator to adequately fund their DB pension schemes and strike a more even balance between payments to shareholders and those to plug scheme deficits.

“Having a robust, coherent plan in place for the DB endgame journey will be the best defence against any intervention from the regulator, as it will take comfort from the framework that has been put in place.”