The news that 20 Aon Hewitt defined contribution schemes have left members exposed to investment risk due to a lifestyling failure is clearly the result of an unfortunate blunder.

But it got me thinking how many DC members are making their own derisking mistakes as a result of poor engagement or simple misunderstanding.

It is estimated that 400,000 people retire in the UK every year with a DC pension. It’s also estimated that somewhere between 80 and 90 per cent of those members will be invested in the default fund, which is predicated on derisking and buying an annuity at retirement.

But a survey by Towers Watson predicted just 40 per cent of retirees post-April will actually buy an annuity. So, it follows the rest shouldn’t be derisking to those safer asset classes. By my simple calculations, that’s more than half of people heading in the wrong direction with their pension fund investment.

Obviously that’s a lot of employees who will potentially be disadvantaged unless they are made aware of the problem – and helped to rectify it.

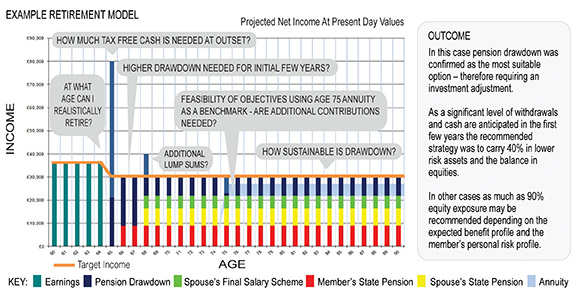

What do your retiring employees actually need?

From our experience, people start engaging approximately five years before retirement. And at that point they need to decide what retirement solution is right for them and then adopt the correct investment strategy.

Source: Intelligent Pensions

This sounds relatively simple and when the vast majority of people were buying an annuity at retirement, to some extent it was.

The default strategy – either lifestyling or target date funds – would actually be fit for purpose for the majority.

However, for the growing number of members now looking to use flexi-access drawdown, the existing default funds simply don’t work.

Adding alternative drawdown investment strategies to default funds isn’t much of a solution either. Not only will it give members the dilemma of choosing which solution is right for them, fundamentally it could result in some catastrophic member outcomes.

Wake-up packs have little choice but to cover every possible option and in most cases result in information overload and a confused and disengaged member

This is because drawdown, unlike an annuity, is constantly evolving as a result of the income taken, changes in personal circumstances and investment returns.

A more personalised approach is needed. But that can be tricky for DC schemes to adopt; employers don’t know what they don’t know.

They will have some personal and financial information about each member, but the chances are there will be far more they don’t know about them, including their objectives, other financial resources and personal circumstances.

As such, wake-up packs have little choice but to cover every possible option and in most cases result in information overload, and a confused and disengaged member.

Fortunately, the DC market is changing and innovative and cost-effective solutions are emerging.

Only by considering retirement income solutions from each member’s perspective can employers truly support their members and help them achieve the best possible retirement outcomes.

Andrew Pennie is marketing director at Intelligent Pensions