Data crunch: UK pension schemes continue to think globally with new allocations in the name of diversification, but are they managing their currency risk properly?

Our sister title tracked £12bn of activity (including mandates terminated) in global equities over the first quarter of this year, dwarfing any more specific geographies – emerging markets and UK stocks saw around £2.7bn each.

Those findings reflect well on the level of diversification in UK scheme assets, but the preference for assets denominated in foreign currencies does bring up the thorny issue of currency risk.

In the retail world, analysis of wealth portfolios by asset management giant BlackRock finds that foreign exchange ranks as the second-largest exposure. Interestingly, the level of Forex risk stays at a similar level whether portfolios fall into the aggressive, moderate or conservative categories.

If you haven’t done it already, you’ve probably done quite well out of that, so what better reason to lock in your gains and hedge at current levels

Simeon Willis, XPS Pensions

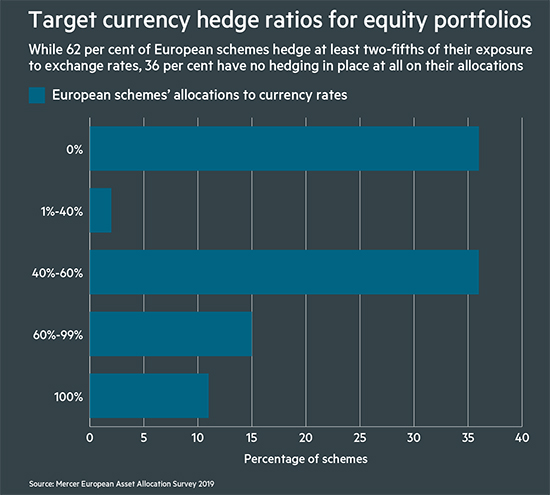

A significant minority of trustee boards carry this trend over to the institutional world. While 62 per cent of European schemes in Mercer’s 2019 asset-allocation survey hedge at least two-fifths of their exposure to exchange rates, 36 per cent of them have no hedging in place at all on their equity allocations.

With the UK institutional investment industry increasingly coming to the conclusion that risks like interest rate and inflation exposure are not worth running and should be hedged, leaving the door wide open to currency swings might look like a glaring oversight.

However, some elements of Forex risk can be seen as rewarded or risk premiums, explains Simeon Willis, chief investment officer at consultancy XPS Pensions.

As in equities and other markets, investors exposed to emerging market currency movements can profit from a carry trade, he says.

“When you have a high interest rate in a local currency, sometimes this is higher than the expected depreciation of the currency relative to other currencies,” Mr Willis says.

“In this instance, investors are being rewarded for taking on the risk of the currency – on average you will expect to earn more from interest than you will lose in depreciation.

“But you have to be exposed to the currency to earn this. If you hold it, but hedge using currency forwards you will end up paying the counterparty the extra return – because they are the ones taking the risk,” he adds.

Brexit boon for unhedged schemes

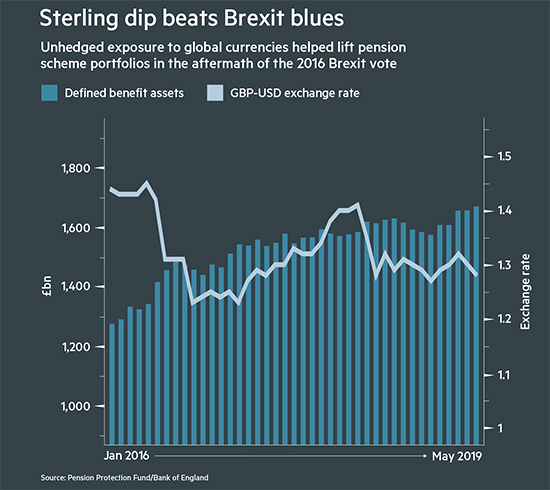

Developed market currency risk has also paid a significant dividend in recent years to globally diversified UK funds, which unexpectedly benefited from the UK’s decision to leave the EU.

The summer of 2016 saw a slump in the value of sterling relative to the US dollar, much to the dismay of any net importers in the business world.

However, pension schemes with overseas assets denominated in dollars and other currencies would have seen those investments’ value jump in pounds and pence. Pension Protection Fund data shows that asset values in UK defined benefit schemes remained remarkably resilient over the period.

However, what is not known is whether this was in any way predictable – currency rates see-sawed on the night of the UK referendum, suggesting that the market was far from certain. The risk has paid off in the short term for many UK pension schemes, but was this the result of trustees’ tactical nous, or merely blind luck?

“Nine times out of 10 I think pension fund trustees will conclude, entirely reasonably, that it’s pretty hard for them to persuade themselves that they know something about the trajectory of currency exchange rates,” says James Wood-Collins, chief executive of Record Currency Management.

“There is a belief that holding overseas currencies somehow diversifies,” he says, but stresses: “The concept of diversification if it’s not rewarded is not terribly helpful.”

Armit Bhambra, head of UK asset owners at BlackRock’s iShares exchange traded funds business, agrees. “Forex is a real risk in portfolios,” he says, explaining that few schemes now bother trying to generate active returns from currency.

“The majority of pension funds now see it as a risk that they need to mitigate. Now, how they do that and in which exposures they do that is something they really need to think about,” Mr Bhambra adds.

Half hedge makes sense

If currency risk is unrewarded over the long term, trustees might want to hedge their entire exposure. However, this introduces excessive costs, negating the benefits of reduced volatility.

Weighing up the volatility reduction benefits of different hedge ratios on an equity portfolio often produces a lopsided ‘smile’ graph – where hedging 100 per cent of an exposure actually delivers a slightly suboptimal volatility outcome.

Factor in the added cost of high hedge ratios for marginal gain, and Record has found that schemes can achieve around 80 per cent of the total volatility reduction possible with a hedge ratio of 50 per cent.

This logic is reflected in real strategy – Mercer’s survey finds that 36 per cent of European schemes hedge between 40 and 60 per cent of their risk.

With the UK’s political climate poised to provoke further currency swings in the coming months, now may be the time to join these ranks, says Mr Willis, who undertook a swathe of Brexit hedging with clients last year.

“If you haven’t done it already, you’ve probably done quite well out of that, so what better reason to lock in your gains and hedge at current levels,” he says.

OTC currency trades can be opaque

Another potential headache for trustees in Forex is transparency, where bundled fees are a source of opacity.

When pension funds come to allocate to overseas investments, they typically need to buy dollars or other currencies to do so. In theory, a market with as deep liquidity as Forex should provide efficient pricing, but its over-the-counter nature creates an opportunity for prices to wander from the market rate.

With transaction costs and explicit costs built into one rate available from a bank or other counterparty, “the size of that reward is frankly very opaque”, says Mr Wood-Collins.

“The Forex market can serve its users exceptionally well in terms of liquidity and transaction costs, but because it’s an OTC market participants benefit from having at least some understanding of how to get the best price,” he adds, pointing out that asset managers have a fiduciary duty to find this.

Mr Willis sounds a similar note of caution over banks rolling up fees and transaction costs. “If you’re having your currency hedging provided for free, you need to make sure that you’re getting your currency traded at the best price,” he says, comparing the risks to getting ripped off buying foreign currencies at a hotel on holiday.