BT Pension Scheme has again boosted its inflation-linked assets, moving towards a targeted allocation of almost a third of its portfolio, while investment experts have cautioned schemes may be paying a premium for protection.

Defined benefit schemes are increasingly looking to shore up portfolios against the prospect of rising interest and inflation rates.

“The strategic asset allocation was modified in April 2013 following extensive consultation with BT on the long-term investment strategy for the scheme,” said the scheme’s report for the six months ended June 30 2013.

The report showed 22.6 per cent of assets were inflation-linked. This is up from 21.7 per cent in December 2012, 20.6 per cent in 2011 and 15 per cent in 2010.

The £39.6bn scheme has a long-term target of 31 per cent of assets invested in inflation-linked assets, which include allocations to mature infrastructure and inflation-linked corporate bonds.

The changes to asset allocation also mean reductions to fixed interest, equities and alternative allocations.

The popularity of inflation-linked assets is at its peak as DB schemes look to match their liabilities, said Harris Gorre, head of financial products at Investec Bank.

This had led to a “exponential” increase in investment in real assets by schemes, said Gorre, such as infrastructure and property, which can provide inflation-linked income streams.

“Very importantly [schemes] have now gone from liquid to illiquid [investments]. If there is a liquidity event, you don’t want to be a forced seller of a shopping mall,” he said.

Protecting against liability risk

Long-lease property has been popular with pension schemes seeking a higher-yielding inflation-hedging alternative to index-linked bonds.

These funds typically target a return of inflation (as measured by RPI) plus 4 per cent a year.

Consultancy KPMG estimated UK pension schemes have invested approximately £3bn in long-lease property pooled funds out of an aggregate fund size worth between £3.8bn and £4bn.

While there has been an increase in demand for all products that help protect DB schemes against liability risk, there has been a greater focus on those that provide protection against rate rises, said Simon Hill, chief investment officer at Buck Global Investment Advisors.

Hedging inflation can be “tricky” for schemes as most products, including index-linked gilts and derivatives, are linked to RPI and not CPI, which is now the official inflationary measure.

“The hedging is indirect even at the best of times, with very few CPI-linked products,” said Hill. “The problem is, even for schemes that are trying to explicitly hedge inflation, one of the risks they are taking is the difference between RPI and CPI.”

Typically schemes have looked at both government and corporate linkers to hedge inflation, however, the low issuance of these bonds has made them very expensive.

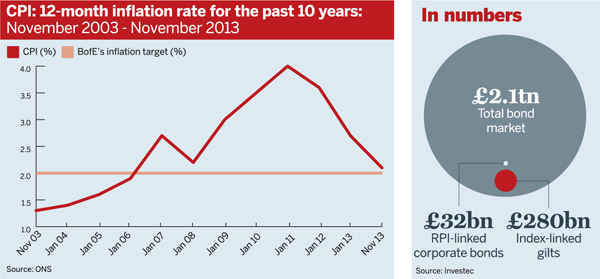

Of the £2.1tn UK bond market (including gilts) only 15 per cent is index-linked, of which £280bn are index-linked gilts and £32bn are corporate linkers, according to Investec (see graphic).

The index-linked gilt market is illiquid, with big institutions tending to buy and hold the asset.

The government has been issuing index-linked gilts at about a rate of about 25 per cent of its total gilt issuance in the past few years. “In terms of gilts that have been issued, index-linked gilts are about a third of the market. So they are issuing less than what is currently in the market,” said Hill.

The scheme declined to give further comment.