Engineering company Centek has so far seen its defined ambition-like auto-enrolment investment set-up outperform the underpin it created to guarantee a minimum retirement outcome for its workforce of uninitiated savers.

Such guarantees were among the options suggested in the government’s 2012 green paper on risk sharing, but experts have raised concerns that upcoming legislation on the definition of money purchase benefits may force such structures to comply with tougher defined benefit regulatory requirements.

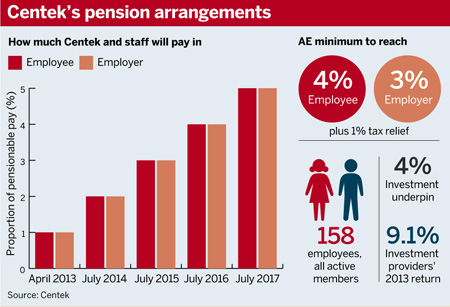

The employer is due to stage next month, but set up the benefit structure in April 2013, when it made the undertaking to employees.

Paul Cooper, financial controller, said: “If the pension scheme doesn’t achieve a 4 per cent return on the contributions made to it, Centek will make additional employer contributions, subject to certain conditions and limits, on behalf of the employee when the employee leaves the company’s service.”

The lack of investment choice with its mastertrust provider Now Pensions made underpinning the investment return possible, Cooper said, as the risk-return profile of the members was uniform.

“We could only really make it work with someone where there was no investment choice,” he said. “If [a member] chose a risky approach we might not be able to underpin it.”

Industry experts have raised concerns that such investment underpins can lead to schemes being classified as DB, making them subject to valuations and the pension protection levy.

The employer is looking into any impact from the money purchase changes.

Jeremy Goodwin, partner at law firm Eversheds, said it is likely that schemes with guaranteed underpins will become considered DB. He added: “The new definition will have a significant effect on schemes.”

Centek has set up contributions of 1 per cent from both the employer and employee, that will rise annually until they reach 5 per cent for each party in 2017.

“We tied it in with the pay review,” said Cooper. “Effectively, we’re ramping this up each year in line with the pay rise.”

The company made membership of the scheme a condition of employment and so all 158 employees are enrolled in the scheme, with no opt-outs.

Auto-escalation can be an effective way to bring employees to an adequate contribution rate while minimising the chances of opting out, said Martin Freeman, director at consultancy JLT.

“I think it’s a natural extension of auto-enrolment. [It] is all about harnessing the power of inertia.”