The number of people saving into large defined contribution schemes has more than quadrupled since 2009, figures from the Pensions Regulator have shown, as signs of DC consolidation begin to appear.

The regulator has said before that consolidation into fewer, larger schemes would drive up governance standards.

Given the growing DC membership, driven by auto-enrolment, experts have long predicted consolidation of schemes – either through acquisition or member migration.

Consolidation [of DC schemes] is both necessary and inevitable

Darren Philp, The People's Pension

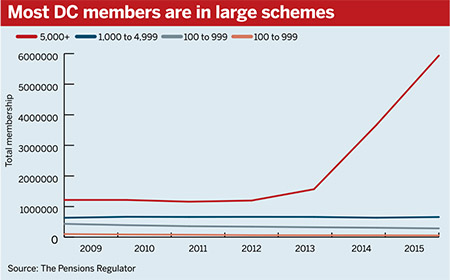

The regulator last week released DC Trust, its annual statistics on occupational DC schemes. It showed a huge growth in the population of larger DC schemes, defined as schemes with 5,000 or more members. There were 5.9m people in larger schemes as of December 2015, up from 1.2m in 2009.

Meanwhile, membership of smaller schemes has declined to 55,000 at the end of 2015, from 101,000 in 2009.

The overall number of schemes went down, from 4,560 to 2,740 over the same period.

However, 5,000-plus-member schemes were the only cohort to grow over the period, with 20 new schemes in the past year alone.

Auto-enrolment drives growth

Phil Duly, associate at consultancy Barnett Waddingham, said auto-enrolment was a key driver of the growth.

He said: “I don’t think it’s driven by brand new trust-based schemes – it’s probably existing schemes that have grown. It’s likely to have risen from auto-enrolment.”

In addition to this, the increased governance requirements have added costs to the running of small DC schemes, which has made alternative arrangements more appealing.

“The value-for-money assessment, reviewing the default strategy and reporting through the chair’s statement, all that is adding cost,” said Duly.

Darren Philp, director of policy at mastertrust the People’s Pension, said: “Consolidation [of DC schemes] is both necessary and inevitable. With the advent of auto-enrolment we’re moving into an era of mass-market pension provision. That will really come through strongly in the next few years.”

Efficiency and governance

As well as auto-enrolment, Philp said employers were moving towards larger schemes to reduce the burden of running multiple offerings and to improve governance.

“This ramping up will mean people will be looking at smaller schemes and asking whether they’re value for money,” he said. “In the main, scale within DC is a key driver for value for money.”

Despite this, he added, schemes will not disappear entirely.

“It’s not to say all small schemes are bad. Quite a lot of small schemes will be more niche. There is a place for them, but I don’t think it’ll be the provision of choice going forward.”

Morten Nilsson, chief executive at mastertrust Now Pensions, said further consolidation was needed.

“The regulator’s data demonstrates that the long-awaited consolidation in the DC market is finally beginning. But the UK pensions market remains incredibly crowded and further consolidation is needed to help drive down cost and improve outcomes for members.”

However, he pointed out that higher standards of governance at mastertrusts are not uniform.

“Not all mastertrusts are the same, and DWP and the regulator are right to look at turning up the regulatory heat on the industry.”