UK defined benefit pension schemes have removed nearly half of their funding level risk over the past decade, but new research has questioned whether asset derisking has gone too far.

Risk reduction played out strongly in the Pension Protection Fund and the Pensions Regulator’s 10th annual Purple Book, published last month, which showed a continued decrease in UK DB schemes’ aggregate allocation to equities.

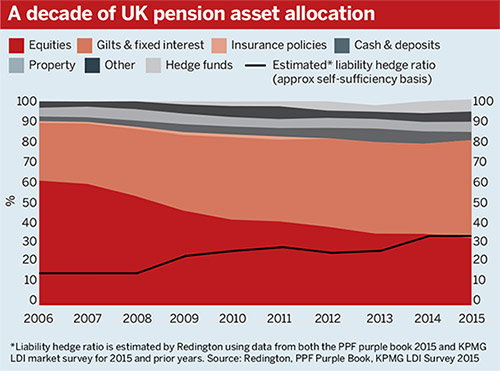

When the Purple Book first came out in 2006, equity holdings accounted for 60 per cent of UK DB schemes’ aggregate portfolio; in 2015, just 33 per cent of assets were held in equities.

Over the same period, UK schemes in aggregate removed nearly half of their funding level risk, according to a new report from consultancy Redington.

The key to this is to get your assets to do two jobs at the same time

Dan Mikulskis, Redington

However, the report says this has been achieved mainly through reducing asset-side risk, rather than by hedging liabilities, raising questions about schemes’ ability to generate sufficient returns to meet long-term funding targets.

The report urges schemes to seek out more rewarded risks in assets alongside hedging increased liability risk through more efficient liability-driven investment.

Dan Mikulskis, managing director at Redington and co-author of the report, said it was crucial for schemes to break out of an old world view of return-seeking and matching assets.

“The key to this is to get your assets to do two jobs at the same time,” he said. “To hedge liabilities and look for returns… getting trustees comfortable with what it takes to actually achieve that.”

Schemes may gravitate towards low-risk asset strategies, but many will also be low-returning, said Mikulskis.

“In some situations it can help to make smaller allocations to high-risk, high-return stuff that might be more efficient,” he said, adding that the use of overlays and leverage in LDI would allow schemes to hedge liabilities and generate returns at the same time.

Sponsors might have to fill funding gap

Using data from the Purple Book as well as consultancy KPMG’s 2015 Liability Driven Investment Survey, Redington estimates the return expected from schemes’ current allocation, cash plus 1.7 per cent, falls 0.7 per cent short of the return needed to reach full funding by 2030.

On average, schemes will need returns of between cash plus 2.4 per cent and cash plus 2.9 per cent to be fully funded by 2030, depending on ongoing levels of sponsor contributions, according to the report.

The report says to meet the shortfall, schemes have to either rely on sponsor contributions or hope for significant rises in long-dated interest rates, but notes schemes are still better off hedging out the latter.

Improving efficiency

Simeon Willis, head of investment strategy at consultancy KPMG, contested the view that asset derisking was the dominant driver behind aggregate risk reduction.

The volatility of liabilities presented in PPF 7800 index data does not capture LDI strategies, Willis said, which would “mirror liabilities to an extent”.

“Pension schemes have been taking massive amounts of risk off the table using LDI; the contribution that will have made to reduce their risk will have been very, very substantial,” he said.

While efforts to derisk liabilities via hedging drove bumper flows into LDI mandates between 2006 and 2015 – in 2014 assets under LDI increased by £146bn to £657bn, according to consultancy KPMG’s latest annual LDI survey – last year’s hedging levels still only account for around a third of total DB liabilities, despite liability risk continuing to outpace asset risk.

Willis agreed that there is significant scope for more schemes to hedge and improve the efficiency of existing structures.

“A large proportion of schemes aren’t hedged… there is still work to be done. There is plenty of scope for schemes to do more efficient LDI,” he said.

Giles Payne, director at professional trustee company HR Trustees, said trustees need to adopt a more “all-in-one” approach.

“It needs a more total look at the whole thing,” he said. “You need to look at your hedging, cash flow and growth all in one picture, rather than trying to segment them too simplistically.”