From the blog: Anecdotal evidence says many UK pension schemes have earnestly considered LDI yet not actually invested. But why? Let’s look at some of the reasons that may be causing those schemes to sit on the sidelines.

‘Yields are too low and will go up’

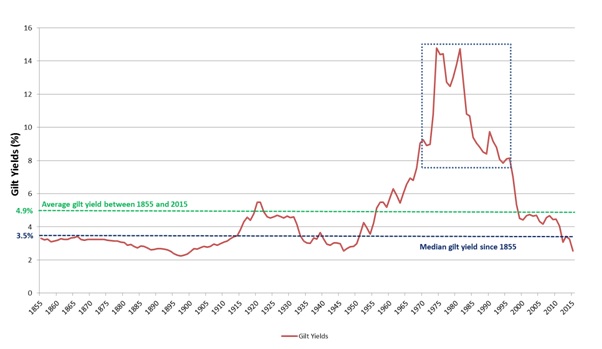

Despite the common view that yields are too low and will rise in due course, the long-term history of UK gilt yields shows a dramatically different possibility – that the high yields in the 1970s and 1990s were not the norm.

As shown in the illustration below, the downward trend in yields over the past 40 years may be less abnormal than commonly assumed.

Historical gilt yields: 1855 – 2015

Source: Axa Investment Managers

This poses an important question: as a generation exposed to yields from the 1970s to 1990s, do we expect higher yields? This could be an example of the ‘anchoring bias’ that is well documented in behavioural finance.

‘Our funding level is too low and we don’t want to lock this in’

Essentially, if the funding level is low, growth assets will be needed to reduce the deficit over time. But reducing the allocation to growth assets and investing in matching assets – or ‘derisking’ – is not consistent with an effort to close the deficit.

However, many pension schemes can increase the level of liability hedging without automatically reducing the allocation to growth assets. For example, many UK schemes are invested in government bonds – switching these assets into LDI may allow the scheme to hedge more liabilities without necessarily reducing expected returns.

‘LDI is too risky’

LDI solutions enable schemes to manage interest rate and inflation risk more effectively, but typically introduce other risks:

-

Counterparty default risk: To mitigate against counterparty default risk, pension schemes can use a number of techniques. Overall, these worked well in protecting schemes during the collapse of Lehman Brothers, for example.

-

Collateral shortfall risk: Should yields rise, the pension scheme’s available collateral will be depleted. The LDI assets will need to be topped up. This is not all bad news, however, as higher interest rates are likely to mean better funding levels.

Pension schemes that are currently sitting on the sidelines should examine their stance on these issues before making any decision on LDI.

Shajahan Alam is head of solutions research, UK LDI at Axa Investment Managers