Data analysis: ManyFTSE 350 defined benefit schemes are taking "a surprisingly high level of risk" in their investment strategies in spite of the Pensions Regulator's increased focus on sustainable growth, a recent report has warned.

Last year the regulator published its latest code on DB scheme funding, in which it encouraged schemes to take account of the potential effect of investment risk on the sponsoring employer and made minimising "any adverse impact on the sustainable growth of an employer" a central objective.

Higher investment risk can turn suddenly on schemes, especially with the volatile equity environment.

Data from consultancy Barnett Waddingham this week showed the deficit had been £65bn by the end of 2014, an increase of £11bn on the year before. But consultancy Mercer's Pensions Risk Survey data, also released this week, stated that the accounting deficit of the FTSE 350 DB schemes leapt 17 per cent to £95bn in the month to July 31 2015, up from £81bn on June 30.

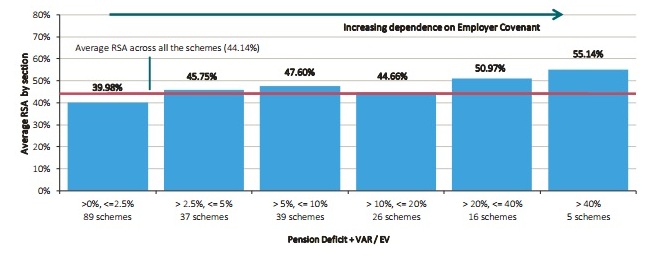

However, another recent report on FTSE 350 pension funds, from corporate adviser Lincoln Pensions, found schemes that were large in relation to their sponsoring employer typically had higher allocations to return-seeking assets, potentially creating more risk for both the employer and the scheme.

Higher reliance = higher risk

Source: Lincoln Pensions

The graph places pension schemes on a scale that shows their size relative to the enterprise value (market capitalisation plus net debt) of their sponsoring employer.

Schemes at the highest end of the spectrum – where value-at-risk plus pension deficit accounts for more than 40 per cent of the enterprise value – hold on average 55.14 per cent of their portfolio in return-seeking assets.

This is compared with an average 39.98 per cent for schemes that account for 2.5 per cent or less of the employer's enterprise value.

It is building up risk in the DB system by placing greater reliance on the employer to stand behind sometimes disproportionate investment risk

Lincoln Pensions

"The larger schemes in the context of their employer are taking the most risk, therefore potentially disproportionately relying on investment return," said Matthew Harrison, managing director at Lincoln Pensions.

He encouraged schemes to take an active role in understanding how financially robust their sponsor is.

"It is really helpful for trustees and employers to understand the risk and financial capacity of their employer to underwrite their risk," he said.

According to the report, there was little evidence the investment risk profile of FTSE 350 schemes was being set with much consideration of the employer covenant underlying it.

It said: "This may reflect certain pension schemes supporting 'sustainable growth' of the employer by leaving money with the sponsor rather than requiring funding for the pension scheme.

"But it is building up risk in the DB system by placing greater reliance on the employer to stand behind sometimes disproportionate investment risk."

This goes against the regulator's increased focus on "sustainable growth".

Risk to flexibility

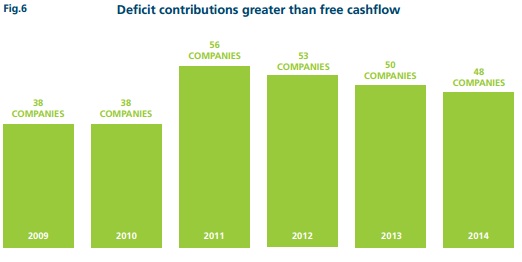

Consultancy Barnett Waddingham's most recent 'Impact of pension schemes on UK business' report, released this week, found levels of deficit contributions in some FTSE 350 companies were greater than free cash flow, stifling the potential for sustainable growth.

Source: Barnett Waddingham 2015

The report stated: "Our analysis once again shows that there are a significant number of companies paying deficit contributions higher than their free cash flow; the unfortunate consequence for these companies is the need to rely upon external sources of finance or to draw upon their cash reserves."

"This in effect represents the 'hidden cost' of pension provision, potentially having more widespread implications on the business."

Recovery plan: Hogg Robinson

Corporate travel company Hogg Robinson extended its deficit reduction plan after low interest rates stretched its shortfall to more than a quarter of a billion pounds.

The travel agency’s preliminary results in May showed its pension deficit had reached £258.6m, an increase of £78.2m on last year.

The company said: “We have noted in the past that inflation and discount rates are volatile and that the current low interest rate environment increases the accounting valuation of pension liabilities.”

Read the full story here.

However, 2014 analysis by consultancy Hymans Robertson found that for many employers funding their pension scheme was relatively affordable, with 71 per cent of companies paying less than one month's earnings into the scheme a year and 83 per cent able to pay off their deficit with less than six months' earnings.

The analysis also suggested combining stable lower cash contributions, longer recovery periodsand a simplified, lower-risk investment strategy to ensure recovery plans work well for both schemes and employers.

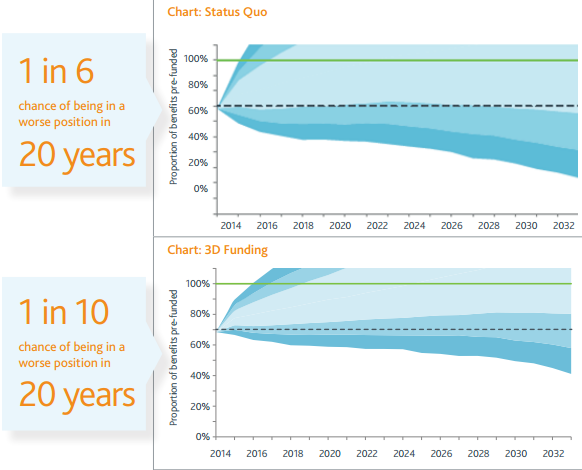

Last year the FTSE 350 was paying £10bn a year in deficit contributions for an average eight-year recovery period, with a third of investment going into matching assets, and two-thirds going into growth assets, the Hymans report found.

It suggests schemes could lower risk by:

reducing the aggregate contribution to £8bn a year, and;

over 15 years changing the asset allocation to one-third in growth assets and two-thirds in matching assets.

The Hymans Robertson graphic below shows the projected range of outcomes for the two strategies.