EMD survey: Returns have lured investors back into the asset class, but pension funds need to tread carefully.

EMD assets overall peaked in May 2013, but as soon as tapering started, outflows were registered.

“The tapering all of a sudden meant there was some sort of end of the amount of help the US would be giving the global economy. Our peak was exactly the day of tapering,” says Simon Lue-Fong, head of global emerging market bonds at Pictet Asset Management.

Most overseas fixed income assets including EMD have provided strong returns to a UK investor as sterling has collapsed

Simon Cohen, Spence & Partners

The sell-off continued for about two years, until the end of January this year, when EMD’s fate turned because investors started to expect slower and fewer rate hikes.

“Around that time there was a lot of short covering, and all of a sudden the returns in EMD started to get very strong,” Lue-Fong notes.

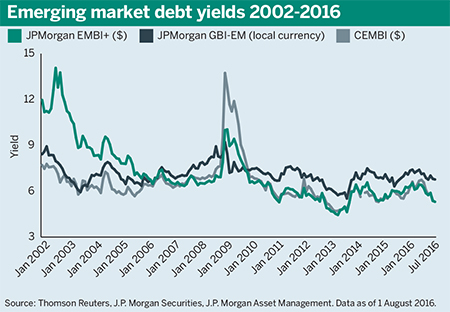

This compares with yields on UK 10-year gilts of just over half a per cent and negative yields in Europe and Japan.

Weak sterling bolsters returns

Celene Lee, principal and head of investment consulting at Xerox HR Services, says emerging markets previously had a hard time in terms of valuation, with currencies losing significant value.

However, a number of currencies have since bounced back. Lee says part of the strong returns produced by emerging market bonds is due to the weak sterling, “but part is also local currencies having strengthened”.

The current yield on the widely used Emerging Market Bond Index by JPMorgan, which tracks hard currency EMD, is about 5 per cent, while the JPMorgan Government Bond Index-Emerging Markets, for local currency debt, has a yield of roughly 6 per cent.

Head of investment consultancy services at Spence & Partners, Simon Cohen, also points out the effect a weakened pound has had on investments after Brexit, making overseas holdings return more than they would have done with a stronger pound. “Most overseas fixed income assets, including EMD, have provided strong returns to a UK investor as sterling has collapsed,” Cohen says.

You are getting most of the return of equities for a lower level of risk

Noel Collins, Mercer

But some believe the currency card has not been played fully yet. Aviva Investors’ head of emerging market debt Liam Spillane believes local currency EMD will become more interesting than hard currency next year.

“The simple reason for that is that over the past three to four years, local currency has significantly underperformed hard currency,” he says.

Yields may come down

Despite this, pension fund trustees should not be led to think EMD returns will remain the star of bond investment for the foreseeable future.

While returns so far have exceeded any expectations investors might have held at the start of the year, Spillane says it is unlikely they will stay this high.

“It would be difficult to suggest that we’d see returns of that magnitude for the remainder of this year. There’s been a very aggressive move earlier this year to get us to this point,” he cautions.

Apart from currency, one of the things that has helped EMD is that over the past few years, credit quality of the EMD universe has become better.

“There have been some recent uncertainties, but broadly speaking over the long term, the credit quality of the countries we invest in has improved,” he says.

Lee agrees: “There is obviously still a lot of risk buried in this asset class, but I think the majority of [emerging countries] are by now investment grade.”

But despite the stellar returns and improved credit quality, the inability to control risk exposure remains a possible barrier for institutional investors such as pension funds.

“It is important that pension scheme investors express and understand their risk appetite before going into an asset class like EMD,” Lee stresses.

Catching the next wave

It seems that although investors have over the past few months shown an appetite for risk, many are looking to take part in the EMD rally and are asking their consultants to find managers for an allocation.

Noel Collins, senior fixed income consultant at Mercer, says: “We’ve had a pick-up in search activity.”

EMD: Good diversifier or not the right time?

Nest’s recent move into EMD could signal an opportunity for other schemes following the summer sell-off, but choosing the right countries and managers is critical

The asset class is attractive, he maintains, because volatility tends to be “quite a bit lower” than equities.

“EMD gives you about 5 per cent to 6 per cent yield; that, broadly speaking, equates to an equity return that might be assumed over the long term,” he explains.

“You are getting most of the return of equities for a lower level of risk.”

And once returns in the current EMD universe do slow down, there will be other countries driving growth and returns, he adds.

“Frontier countries... will then become the next wave of standard EM countries,” he says.

About a quarter of clients express an explicit desire to have frontier countries in their allocations, he notes, as investors are trying to get into the next wave of returns.

Including frontier markets also helps diversify the EMD investments. Collins says: “There’s a feeling that it gives the manager a better universe to invest, so you’re giving the manager a better investment mandate.”