A High Court case involving Thales and trustees of its pension scheme has concluded it cannot move from the retail price index to the consumer price index for some benefits, highlighting how the wording in a scheme’s rules dictates the measure of inflation that is used.

Historically, CPI has produced a lower rate of inflation than RPI. Many schemes have RPI written into their scheme rules.

On the basis of fairness between schemes, fairness between members, fairness between employers, you would think it would be better just to say, 'Well it should be CPI for everybody'

Simon Tyler, Pinsent Masons

Various experts have called for the government to introduce a statutory override to allow schemes to switch from RPI to the lower CPI to reduce the burden on employers.

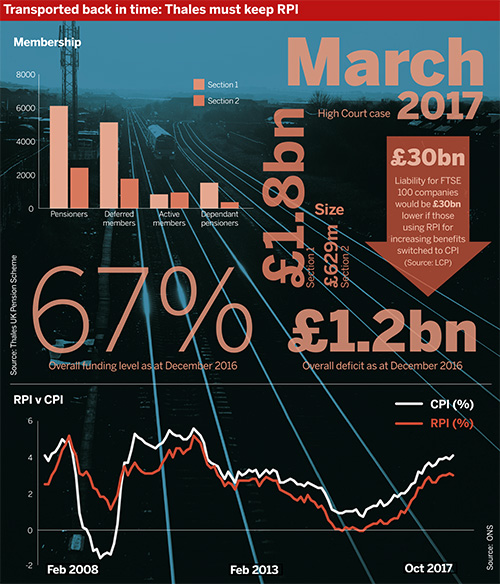

Transportation, aerospace and defence company Thales made a request to the trustees that, where legally possible, the index to which benefits are increased and revalued be switched from RPI to CPI, which would cost less to implement.

In a letter to members, chairman of trustees Peter Rowley said: “This was a complicated task given the fragmented nature of the scheme’s historic benefit structure, requiring detailed analysis of the rules, and in some areas the matter was determined by a ruling of the courts.”

The Thales UK Pension Scheme, which is split into two sections, comprises a career average revalued earnings scheme for benefits accrued from January 1 2008. It also contains the legacy benefits of various final salary pension arrangements, including the Thales Optronics Pension Scheme.

A High Court case in March 2017 considered the scheme rules to determine whether it was possible to move from RPI to CPI in relation to indexation of benefits already accrued for members with Care benefits earned in the scheme since 2008, and those with legacy TOPS benefits who left pensionable service in that scheme before April 1 1997.

Determining the ‘nearest alternative index’

Under the scheme’s rules for the Care section, trustees are permitted to change the method of indexation if RPI’s “compilation is materially changed”.

The rules state that the principal employer, with the agreement of the trustees, will need to “determine the nearest alternative index to be applied.”

The housing cost component of RPI used to be measured using the house price index, but in 2008 it changed to a tailored version of the index. Justice Warren concluded that the incorporation of the Office for National Statistics’ new UK HPI into RPI “does result in a material change to the compilation of the RPI”.

He said: “The ONS considered this change to be ‘non-routine’, which I find as a fact to be the case.”

This meant Thales was required to determine the nearest alternative index. In the judge’s view, “the nearest alternative index must be the one which most closely reflects the existing elements of the RPI”.

Despite the change in what is included in RPI, he did not consider that it should automatically be excluded as a candidate. “It may very well be that the RPI as so changed is, indeed, the nearest alternative index,” he said.

He concluded that, following the introduction of UK HPI, RPI was the nearest alternative index.

RPI most appropriate

The rules of the final salary TOPS state that if RPI “is revised to a new base or if that index is otherwise altered after a date which is relevant in respect of a pension in terms of this rule, all subsequent variations in that pension will be on a basis determined by the trustees having regard to the alteration made to the retail prices index”.

The focus here was on the meaning of whether RPI had been “otherwise altered”. As with the Care decision, Justice Warren concluded that the most material alteration is the introduction of UK HPI into RPI, meaning that with the tailored version of UK HPI, RPI was the most appropriate index.

“I consider that RPI as varied by the introduction [of UK HPI into the RPI] is the only basis which the trustees could properly determine, for the same reasons that it is the nearest alternative index under the Care rules,” the judge said.

Unusual wording

Earlier this year, the High Court denied BT the right to change the measure by which increases for the defined benefit scheme’s largest section are calculated – a decision the company is set to appeal.

And in the Buckinghamshire v Barnardo’s case in 2016, the Court of Appeal held that CPI could not be used under the fund’s existing rules without an amendment being made.

Despite having “kind of won on that point of [RPI] being materially changed”, the Thales outcome was “not the answer the employer wanted”, said Alice Honeywill, partner in law firm Burges Salmon, with the scheme continuing to use RPI.

Wording in scheme rules varies widely, but “that wording particularly about the ‘nearest alternative’ is fairly unusual in my experience”, Honeywill said.

In June 2010, the government said it planned to use CPI rather than RPI for public sector pensions from April 2011. A month later, it said CPI would also apply to private sector pensions from the same date.

However, when this legislation was introduced, the government did not introduce a statutory override to make the change automatic for schemes.

A scheme’s rules would have been written at a time when people were not expecting these sorts of changes, and “the wording can be quite random”, said Simon Tyler, legal director at law firm Pinsent Masons.

Tyler echoed Honeywill’s view that the nearest alternative wording in the Thales case “is unusual”. Comparing this with the Barnardo’s case, he said the wording in the latter might be more common; the Barnardo’s rules refer to RPI or any “replacement” adopted by the trustees.

A political ‘hot potato’

Last week, Bank of England governor Mark Carney called for a “deliberate and carefully timed” withdrawal of RPI from its use in government contracts, arguing that most would acknowledge that RPI “has no merit”.

According to the Department for Work and Pensions’ green paper on DB sustainability, about 75 per cent of pension funds have RPI written into their pension scheme rules.

While the government has acknowledged the existence of this ‘rules lottery’, further details on whether it will take action by providing some sort of statutory override remains to be seen in its white paper, which is due in spring.

“It’s a bit of a hot potato as a political issue,” said Tyler. “On the basis of fairness between schemes, fairness between members, fairness between employers, you would think it would be better just to say, ‘Well it should be CPI for everybody’.”

However, when it comes to introducing a statutory override, “you have to be quite a courageous government to do something which probably would result in members receiving lesser benefits than they otherwise would receive”, Tyler noted.

CPI for future benefits for some members

“The choice of measure for increasing pensions is governed by the specific rules of the pension scheme – it’s something of a legal lottery as to whether those rules dictate a specific index,” or whether the sponsor or trustee are permitted to use their judgment on a more respected measure, said Alex Waite, partner at consultancy LCP.

He added that sometimes the rules do allow choice, but place constraints on the circumstances when the judgment can be applied, or on the range of choice.

Waite said the purpose of the pension increase rule was typically either to comply with legislation, which would lean towards CPI, or to protect members from general inflation – perhaps leading to the use of CPIH, which is an additional measure of CPI including a measure of owner occupiers’ housing costs.

Generally, “it seems highly unlikely to me that [scheme] rules were ever intended to lock into a widely discredited measure, with a clear mathematical bias, such as RPI,” he added.

While the Thales High Court case concerned members with Care benefits earned since 2008 and those with legacy TOPS benefits who left pensionable service in that scheme before April 1997, others will see their benefits uprated in line with CPI going forward.

According to the Thales scheme, for members with legacy TOPS benefits who were in pensionable service in that fund on or after April 1 1997, “legal advice received from a leading pensions barrister was that the relevant rules meant that RPI had switched to CPI automatically from 2010”.

The trustee and the principal employer entered into a deed of amendment to provide that future service Care benefits earned on and from April 1 2017 would be indexed using CPI rather than RPI, and communications have been issued to this group to explain the implications of this change. Care members now have two parts to their Care benefits, before and after April 2017.