Trustees of the Scottish & Newcastle Pension Plan will be assessing the impact of a recent corporate acquisition made by the pension scheme’s parent company Heineken UK, as part of a full covenant review this year.

Employer covenant can change quickly, and the Pensions Regulator advises schemes to monitor it regularly between formal reviews.

We’ll carry out a full review of the strength of Heineken’s financial position following this acquisition

Robin Hoytema van Konijnenburg, Scottish & Newcastle Pension Plan

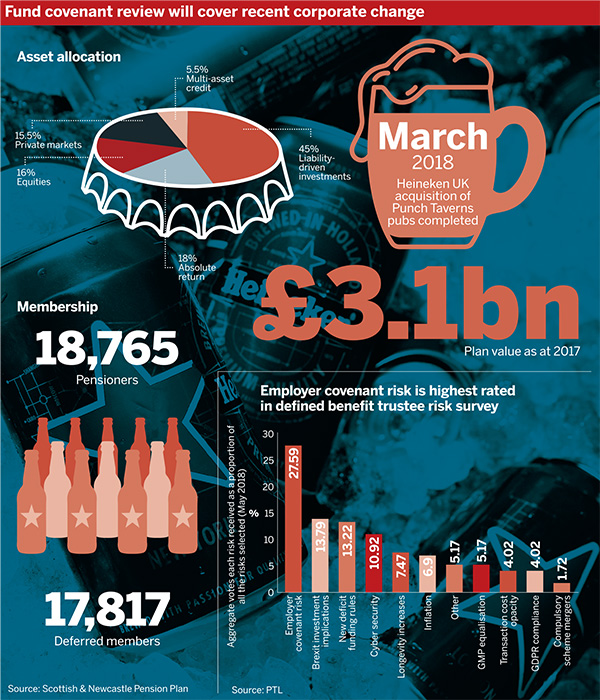

In August 2017, cider and beer business Heineken UK was given the green light by the Competition and Markets Authority to purchase approximately 1,900 pubs from Punch Taverns. The acquisition has now been completed.

Trustees of the circa £3.1bn plan are going to be taking the change into account in the upcoming covenant review, according to a spring 2018 newsletter to members of the Scottish & Newcastle scheme.

“We expect 2018 will be a busy year for the plan,” said chair of the scheme trustee board Robin Hoytema van Konijnenburg in the newsletter, adding that the trustees and the company continue to work on the strategy for the pension scheme’s investments and long-term funding.

“As part of the trustee’s ongoing work on the plan’s funding, we’ll carry out a full review of the strength of Heineken’s financial position following this acquisition,” Hoytema van Konijnenburg said.

The acquisition brings the total number of pubs in Heineken UK’s Star Pubs & Bars estate to around 2,900, making it the third-largest pub company in the UK.

The Scottish & Newcastle scheme’s next triennial actuarial valuation is due to start in autumn. The newsletter stated that “the trustee plans to carry out a full covenant review of Heineken UK this year to assess the impact of the acquisition”.

It added that regularly assessing and monitoring the convenant helps the trustees to decide the appropriate levels of risk when setting its investment strategy, funding target and, where applicable, the recovery plan.

According to the scheme’s latest summary funding statement, the plan had a shortfall of £586m at October 31 2016 – up from £436m in 2015.

This was mainly “due to a reduction in the assumption for future investment returns and an increase in market-implied inflation”, the statement read. It added that this had been partially offset by the higher than assumed investment return from the assets and the contributions paid by the company.

Based on the 2015 triennial valuation, the company renewed the funding plan – with an aim of removing the shortfall by May 31 2023.

It agreed to an annual company contribution of £35.8m in 2016, thereafter increasing by £1.7m a year. The contribution then drops to £19.9m in 2023.

Trustees have become smarter

The key risks concerning trustees of defined benefit schemes include funding volatility, the strength of the employer covenant and implementing an inappropriate investment strategy, according to a 2017 survey by Crowe Clark Whitehill.

A number of pension plans have hit the headlines in recent months in relation to corporate activity.

In February, Trinity Mirror announced the acquisition of Northern & Shell’s publishing assets, with the buyer agreeing measures to support its acquisition’s pension schemes.

“Trustees have always been cognisant of their dependence on the ongoing profitability of a defined benefit pension scheme sponsor,” said Alan Pickering, chair of professional trustee company Bestrustees.

Pickering said trustees have become smarter, using covenant advisers in a much more focused fashion.

He noted that trustees may well take a view on the covenant of the existing sponsor, but the extent to which they explicitly take that into account in the valuation process will vary from scheme to scheme.

“I’m one of those that believe that covenant doesn’t pay pensions,” said Pickering. He said he would rather have the money from the employer when the covenant is strong and the contributions are affordable, “rather than having complex covenant arrangements that will kick in if and when money is short”.

Put in place a plan of action

Trustees are often advised to consider scenario testing to ensure they are prepared and know how to react to a merger and acquisition event.

“The problem with scenario testing is that you never tested the scenario that actually came to pass, because it would usually emerge from left field,” Pickering said.

“What many trustees now do is put in place a mechanism that will be triggered if there is a stock exchange announcement,” for example.

He said that mechanism will involve someone – perhaps a covenant adviser, if there is one on standby – contacting the trustee chair, who will then activate a process that will kick off as quickly as possible.

This process may involve making use of some advisers who are not on the scheme’s current line-up, Pickering noted. This is because some of the advisers to the scheme or to the employer may also be in use by the other party involved in the corporate activity.

“You may well need to call in someone other than your ongoing adviser,” he said.

For schemes with a covenant adviser “on standby”, Pickering highlighted the importance of trustees getting used to working with them – even when there is no sign of corporate activity.

Ultimately, “as a trustee, I would place... more emphasis on having a plan of action that can be quickly implemented, should there be an unexpected piece of corporate activity, rather than doing lots of scenario testing”, Pickering said.

Any scheme where their sponsor goes through a material merger and acquisition transaction is now typically getting a pre and post-covenant assessment

Darren Redmayne, Lincoln Pensions

Discuss transactions as soon as possible

It is important that trustees and sponsors work together and share information as much as possible, said Jacqui Woodward, senior consultant at XPS Pensions.

“But sometimes, there are commercial considerations that mean that isn’t possible,” from the speed of the transaction, to concerns over confidentiality, she said.

Woodward added that, when it comes to confidentiality, trustees can sign confidentiality agreements, “so that shouldn’t be given as a primary reason from the sponsor”.

Talking about pensions issues as soon as possible is ideal, according to Woodward. But “often, trustees do find themselves on the back foot”.

The Department for Work and Pensions’ white paper on DB pensions proposed a requirement for sponsoring employers or parent companies to make a statement of intent, in consultation with trustees, prior to relevant corporate transactions taking place that they have appropriately considered the impacts to any DB scheme affected.

“Typically, it’s best practice anyway, that they’re talked about before the transaction goes ahead, but this seems to be kind of formalising that best practice,” Woodward noted.

Bring trustee subgroups into company confidence

Darren Redmayne, chief executive officer of Lincoln Pensions, said: “Any scheme where their sponsor goes through a material [merger and acquisition] transaction is now typically getting a pre and post-covenant assessment looking at how their employer covenant’s affected.”

One of the challenges though is, to do that, “you need information”, he said. It may be difficult for the scheme to get information on the transaction in terms of whether there is debt involved, or whether cash is coming in or leaving the sponsor, for example.

“All too often, pension trustees are told about the transaction or given information to analyse it far too late,” Redmayne said.

He echoed Woodward’s comments on many companies putting this down to the need for confidentiality, because they are concerned about potential leaks regarding transactions that may or may not happen.

But Redmayne stressed the importance of sponsors engaging with trustees sooner rather than later if they want “a transaction to go smoothly and... want to make sure there are no surprises”.

In terms of good practice, trustee subgroups “might be brought inside on particularly sensitive corporate transactions at an earlier stage”. This enables them to gauge whether there is going to be additional funding required as a consequence, for example.

At a later stage, that information can be shared with the broader trustee board, which can then take decisions from a position of fully understanding the situation, Redmayne noted.