Data analysis: With gilt yields falling it has been a confusing period for investors – but what does it mean for derisking?

The provider’s view

Once again, the markets seem to be setting a conundrum for pension scheme trustees. A broadly consensual view not so long ago was that gilt yields would rise over time. They have not.

In fact, 10-year gilt yields declined over May to 2.57 per cent from 2.64 per cent.

It is not easy, but trustees should try to understand what is going on in order to protect against future downside risk.

It is not easy, but trustees should try to understand what is going on in order to protect against future downside risk.

Despite the UK economy showing signs of strong growth – with equity markets reaching highs – weakness persists in Europe, and some investors may be betraying an underlying uneasiness, or a view that ultra-low interest rates are here to stay.

Eurozone inflation is now down to just 0.5 per cent and it is possible that the region could tip into deflation, perhaps precipitating another round of the eurozone crisis, either political or economic.

But significantly, market volatility – as measured by the Vix index or ‘fear gauge’ as it has been dubbed – is at a seven-year low, suggesting that in the main, investors are disregarding or are complacent about risk.

Central bankers and others are now beginning to worry that what we are seeing is very similar, too similar for comfort in fact, to the disconnect between credit and equity markets in 2006-07.

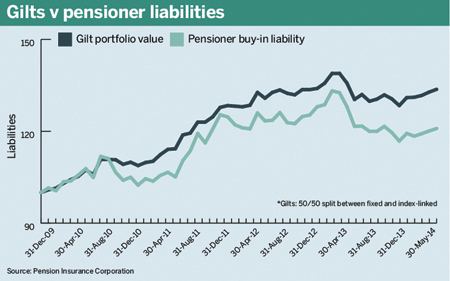

But for the moment, there is a record gap between the value of a portfolio of gilts and the cost of insuring pensioner liabilities, as the chart above shows.

With the recently announced £1.6bn buy-in of the Total UK Pension Plan building on the earlier £3.6bn ICI buy-in, it’s clear trustees are looking to take advantage of this opportunity while they still can.

Expect to see more this year.

David Collinson is co-head of business origination at Pension Insurance Corporation

The consultant’s view

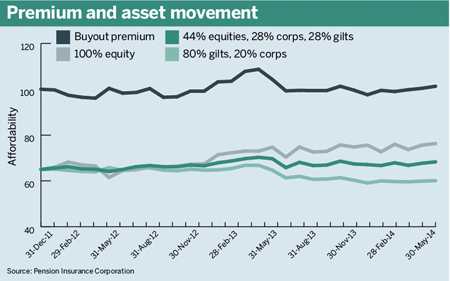

As the chart suggests, May proved to be a relatively benign month for investment markets, and consequently buyout pricing changed relatively little over the period.

Both nominal and real gilt yields fell marginally – this was slightly more pronounced at the short-dated end of the curve.

Gilt yields experienced downward movement around mid-May, due to disappointing European gross domestic product figures.

Gilt yields experienced downward movement around mid-May, due to disappointing European gross domestic product figures.

However, much of this move was eliminated by the end of May, with month-end yields on real and nominal gilts only slightly down on the start of the month.

The additional yield on corporate bonds over gilts also contracted slightly during the month, continuing the trend since the financial crisis.

Equity markets saw modest gains, with all major developed markets achieving positive low single-digit sterling returns.

It is apparent that markets are experiencing a steady couple of months after some good progress recently.

Although some economists are suggesting that conditions such as these – benign returns after a period of strong equity market growth – could be the backdrop for a single negative catalyst causing a downturn, stable conditions appear set for the present time.

This would suggest that now is a good time to derisk and lock in gains made over the past year. Indeed, the increased interest seen recently by insurers in full buyout transactions as well as pensioner buy-ins would support this view.

Clearly, as favourable conditions persist, there is a risk that demand could outstrip supply.

However, the recent Budget statement could see capital, previously available to support retail annuities, being redeployed to the bulk annuity market, helping to stabilise pricing at current levels.

Emma Watkins is a partner at LCP