Trustees of the defined benefit schemes of Thomson Reuters have been updating members about the agreed sale of part of the business, as experts stress the fine line between saying too much or too little about a deal.

Headlines about companies like Toys R Us – which became insolvent this year having been sold to private equity firms in 2005 – have increased awareness of the impact corporate activity can have on pension benefits.

We are keen to reassure the members of RPF and SPS that we are exploring the impact of the Blackstone joint venture

Greg Meekings, RPF and SPS

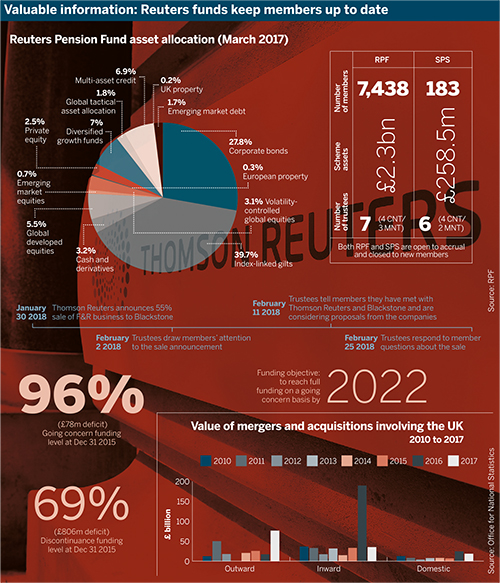

At the end of January this year, information company Thomson Reuters said it had signed an agreement to sell a 55 per cent stake in its financial and risk business to private equity funds managed by US investment company Blackstone Group. The Canada Pension Plan Investment Board and Singaporean sovereign wealth fund GIC are also investing for the transaction.

Twelve days after the agreed deal, trustees told members they had met with Thomson Reuters and Blackstone “to discuss and clarify some points in relation to the sale”.

Two weeks later, the trustee responded to member enquiries on how it plans to “support and represent” the long-term interests of the scheme members in its discussions with the sponsor.

The trustees cited the possible involvement of the Pensions Regulator early on in their statement: “As you would expect, if the trustees consider the proposed transaction negatively impacts the security of member benefits, they will ensure it is mitigated as much as possible (and involve the Pensions Regulator if necessary).”

They went on to explain that the role of trustees is not to demand continued accrual – something members have been concerned about – but to protect benefits already accrued. “The trustees will do all within their powers to maximise the protection of the accrued benefits of all members of the schemes,” it said.

There are 7,438 members in the Reuters Pension Fund and 183 in the company’s Supplemental Pension Scheme.

“But as regards the future accrual of benefits, this will be driven primarily by discussions between employees and their current or proposed future employer regarding the proposed terms and conditions that will apply to their employment,” the trustees explained.

Both the RPF and the SPS are closed to new members but currently open to benefit accrual.

Nonetheless, the trustees added that they will “maintain an ongoing dialogue with Thomson Reuters and Blackstone in order to ascertain and understand their proposals in relation to future service accrual”.

Risk of scrutiny keeps trustees on their toes

The interest of the Work and Pensions Committee in cases like BHS, Carillion and Toys R Us, and the perceived possibility of the regulator becoming involved have not gone unnoticed by trustees and members.

Chair of the RPF and the SPS, Greg Meekings, said: “A number of pension schemes have been subject to intense scrutiny over recent months regarding the actions that they have taken to protect member benefits adequately.”

He said the Reuters trustees were “keen to reassure the members of RPF and SPS that we are exploring the impact of the Blackstone joint venture involving the financial and risk business”.

The trustees have created subcommittees for each of the two schemes “to progress discussions through regular meetings both internally and with the sponsor” and are taking advice regarding the impact of the takeover on the sponsor covenant, he added.

Depending on how the covenant strength is affected, schemes often ask for extra funding or guarantees.

Meekings said: “We will discuss any change in the nature and strength of our covenant with the sponsor, including what level of mitigation may be appropriate.”

He stressed the “open and constructive channel of communication” the trustees have with the scheme sponsor, as well as Blackstone and the regulator.

How much information is too much?

Janine Wood, a director at Independent Trustee Services, said member communication during a sponsor takeover can be complex because the situation is “very fluid” with “things going on behind the scenes”.

Trustees also have a duty of confidentiality and might have signed non-disclosure agreements, she pointed out.

However, Wood was in favour of letting members know that the trustees are actively involved. “I think it should be more common than it is,” she said.

This has become more important “in light of Carillion and BHS”, she noted, as there is more concern among members, although she added that there was a “lack of understanding of how defined benefit works”.

For trustees, it would therefore be “enough to say we’re looking at it, we’re in negotiations with the company”.

Anne-Marie Winton, a partner in Arc Pensions Law, warned that trustees might want to reassure worried members but need to take care not to divulge too much about the details of the deal.

“The key question that members want answered is whether their pensions will be as secure after the sale as they were before. And that is the key analysis that trustees will need to do,” she said.

Mend the roof while the sun is shining

Winton said trustees who are faced with a takeover situation should request as much information as possible about the structure of the deal and how it will be funded – especially whether the scheme as an unsecured creditor will be pushed down the ladder by new security given to lenders.

The buyer’s financial strength and long-term plans for the business should also be looked at in detail.

“Be prepared to stand your ground and ask further questions if you are not satisfied with the initial responses received,” Winton advised.

Trustees looking for mitigation should consider extra securities in case of a worsening sponsor covenant, but Wood said that equally they might still seek more funding if the covenant strengthens, to improve the security of benefits while the sponsor can afford it.

These negotiations are time-sensitive and require trustees to be involved before it is too late, Wood said.

Trustees should therefore look to have a protocol in place with the employer about what information should be shared and when.

“That’s good practice,” she said, although “sometimes the real difficulty is getting the company to engage with you when nothing is going on”.

TPR was not always keen to get involved

Companies undergoing M&A activity can apply for voluntary clearance with the regulator. While trustees can ask sponsors to seek clearance, companies often do not.

But some trustees have levers at their disposal. According to Winton, “there can be some valuable powers in the trust deed and rules”.

These could include additional employer contributions having to be paid unilaterally, or even the winding up of the scheme being triggered.

“Some trusts still have so-called ‘poison pill’ triggers whereby a change of control of the sponsoring employer moves all the employer powers under the trust to the trustees,” she added. “If the trust says this, the trustees ought to know about it.”

Where trustees see some detriment in their sponsor’s activity, they can also write their own report to the regulator.

But while the regulator might have been more proactive since BHS, this was not necessarily true in the years before.

Wood said that sometimes the regulator could be “more standoffish”, adding: “I’ve seen a response where TPR will say, ‘If you and the sponsors are still talking then carry on talking’.”

Still, Wood said mandatory clearance – something that has been floated as part of the government’s DB green paper published last year – would not work in practice.

“From a trustee perspective that would be great,” she said. “But for UK plc it can’t work.”

This does not mean nothing should change, however. “I would like to see something in relation to dividends,” she said, “but my concern is corporate advisers will get around that”.

Winton echoed her reservations about making clearance mandatory.

“What could help is updated regulatory guidance and its current powers being used more, carefully publicised… and tested in court where appropriate to show their extent.”