The Parliamentary Contributory Pension Fund has introduced a new allocation to alternative credit to further diversify the scheme’s portfolio of return-seeking assets.

Alternative credit, which can be defined as credit that is not traditional investment grade, corporate or sovereign debt, has become an increasingly popular choice for defined benefit funds.

The key reason was to diversify the fund’s return-seeking assets further, by increasing the allocation to higher-yielding return-seeking assets

Lucy Tindal, Parliamentary Contributory Pension Fund

A demand for diversification and increased yield has boosted investor appetite for the asset class.

Back in 2014, the Transport for London pension scheme moved further into alternative credit investments, including mezzanine debt.

In 2016, trustees of Vodafone’s scheme reported a new 7.3 per cent allocation to alternative credit. That year, the Mineworkers Pension Scheme also announced a new allocation to the same asset class.

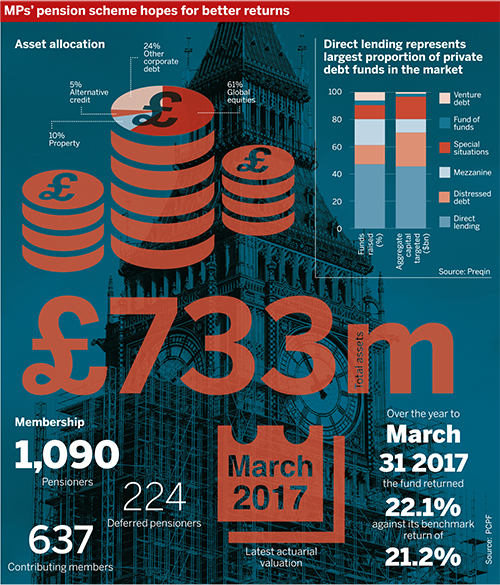

Now the £733m PCPF, the scheme for MPs, government ministers and other parliamentary office holders, has followed suit.

The fund has reduced its global equity allocation in favour of a new 5 per cent alternative credit allocation, introduced in Q2 2017.

Driving diversification

Lucy Tindal, secretary to the trustees for the PCPF, said: “The key reason was to diversify the fund’s return-seeking assets further, by increasing the allocation to [higher]-yielding return-seeking assets.”

In addition to increasing the level of diversification and acting as another source of income due to the cash flows associated with the underlying debt instruments, “the fund should also benefit from the illiquidity premium associated with this type of debt mandate”, states a report to members, published in February.

Petra Stassen, client portfolio manager, alternative credit, at fund manager NN Investment Partners, said that current opportunities in alternative credit span from short-dated trade finance and medium-term commercial real estate loans, to long-dated infrastructure debt.

A number of alternative credit opportunities have arisen from new regulations in the banking sector, where increased capital adequacy requirements have led to banks retreating from the loan market – freeing up more space for institutional investors to step in and lend directly.

“The lending gap still remains the most prevailing in [small and medium-sized enterprise] lending, especially in the smaller segment,” said Stassen.

She said: “The key question to ask is what features a pension fund is looking for in their portfolio – do they need long duration or do they prefer floaters; can they take a higher credit risk or do they want a conservative risk profile?”

Investors continue to seek higher yields

The way in which pension funds have been investing in alternative credit in recent years varies across Europe. Stassen said that it can be partially driven by different regulation, solvency levels and the way the local pension system works.

Generally, “the larger pension funds are increasingly looking at other alternative credit strategies, capturing the benefits of earning a yield pick-up as compensation for the lower liquidity and higher complexity”, Stassen said.

Smaller pension funds, on the other hand, “are only just starting to investigate the opportunities”, she added.

Daniel Fox, senior investment associate at consultancy P-Solve, echoed the view that, in the current environment of low yields and tight spreads, some areas of alternative credit look attractive in comparison with public markets.

Within alternative credit, “there remains the opportunity for skilled managers to generate strong risk-adjusted returns, harvesting a complexity and illiquidity premium,” he said.

Fox noted that alternative credit managers may be able to benefit from changing market dynamics, particularly the regulatory environment. “Those with strong origination and credit underwriting ability should be able to continue to perform well,” he added.

Schemes should be selective

However, while the asset class attracts institutional investors looking to take advantage of the illiquidity premium while diversifying their portfolios, pension funds should choose their managers carefully.

While there is value in some parts of the market, “this is certainly not true across the spectrum of alternative credit mandates, so investors need to be selective where allocating capital”, according to Fox.

He said he was wary of the amount that has recently been raised within certain parts of the market, pushing down yields and weakening credit terms. Fox added that, in addition, many new entrants to the market are untested during negative credit environments.

While locking up capital is not in itself a risk, “we are late in the credit cycle, so investors should also be cognisant of the opportunity cost of holding these assets were markets to turn”, he noted.

In terms of most popular alternative credit strategies, Niels Bodenheim, senior director, private markets at consultancy bfinance, said: “We have seen most investor appetite for senior direct lending, and it has been for those marking their first entry into the asset class.”

Bodenheim added that there has also been interest for real estate and infrastructure debt in the mezzanine space.

Generally, “private debt offerings have illiquidity premiums over traditional markets, which is attracting investor interest”, he said.

Diversifying away from equities

James Trask, investment partner at consultancy LCP, said “many pension funds are embracing alternative credit because the yields available are pretty attractive, despite them being lower than they were few years ago”.

The PCPF made space for the allocation by cutting down on its global equity exposure.

Trask said alternative credit can be a good way to diversify away from equities. If a pension scheme is heavily reliant on equities for growth, adding an alternative credit allocation may be a sensible move.

Similarly, Jonathan Daykin, partner at consultancy Barnett Waddingham, said that those moving away from equities are concerned about equity valuations, but are looking for a comparable level of returns elsewhere.

“If you’re looking for similar returns to equities within a credit space, you need to either be pushing out into more illiquid credit or into riskier credit,” or a bit of both, he said.

However, while the benefits of investing in the asset class include lower volatility and diversification away from equities, “these investments are not guaranteed by any means – you can lose money on them” and “you’re never going to get a… stellar return” compared with equities.

PCPF streamlines property allocation

The fund has also been taking steps to “rationalise” its property allocation, with the objective of moving from four underlying real estate managers to three. It was completed at the end of 2017, according to Tindal.

She said the main reason for the move was “so all the fund’s property holdings would have income distribution share classes”.

Tindal added: “There was also the benefit that it simplified the governance structure of this element of the fund”.

Daykin said he would be “very sympathetic to their direction of travel” in terms of reducing the number of managers from four to three – noting that it would be unusual to have an allocation of around 10 per cent to property spread across four managers.

Reducing the number of managers was implemented over time, as attractive opportunities arose to carry out transactions.

Daykin said transaction costs can be problematic when it comes to property. “It can cost about 5 per cent of your investment to transact on property if you just go in and out without being more careful about it,” so schemes should try to move when there is “an opportunity to get out at a better price”.

In terms of simplifying governance, he said it is “always going to be easier having three managers rather than four, or two managers rather than three, so I think it makes sense – it seems like a reasonable thing to be doing”.