Nest’s CIO Mark Fawcett explains why investing beyond the UK matters to scheme portfolios, and how trustees could attack their global equity strategy to achieve diversification.

Sticking close to home can sometimes be a perfectly sensible thing to do. But when it comes to equities, adopting automatic positions that place a large amount of scheme members’ portfolios in the UK exposes them to risks.

It is common for investors across the globe to show a home bias, that is, they tend to invest in their domestic equity market rather than in global markets.

Key points

• Staying heavily invested in domestic stocks can leave members at risk of more dramatic volatility

• Concentration in one sector could mean missing out on valuable opportunities through diversification

• Global equity funds or smart beta indices could allow schemes to access global growth with less risk

For example, the UK market represents just 8 per cent of the FTSE World Index. However, a typical defined contribution default fund may have as much as 50 per cent invested in UK stocks.

Sticking with familiar local stocks can ultimately leave trustees, as well as the members on whose behalf they are investing, vulnerable to more dramatic volatility than they might be expecting.

Last year for example, the US market – represented by the S&P 500 and accounting for around half of the world index – rose around 10 per cent. This is compared with the FTSE All Stock, which rose around 2 per cent.

Well-managed global equity funds might help overcome objections some trustees may have in selecting a single-country market

Spreading equities across markets can help level out dramatic volatility and support long-term returns.

Concentration risk

Putting large proportions of a scheme’s equity allocation on the FTSE is not simply a step to invest in the familiar and visible. It is also making big bets on certain sectors.

The UK market is characterised by an over-representation of a handful of sectors, with banks and oil, gas and mining companies dominating.

Energy companies, for example, represent around 12 per cent of the FTSE UK All Share, compared with around 7 per cent of the FTSE All World Developed.

Being too concentrated in any one sector is rather like putting all your eggs in one basket. This approach also may see you fail to take advantage of the opportunities available through diversification.

Technology companies, for example, include some consistent outperformers. While they represent little more than 2 per cent of the FTSE UK All Share, they make up nearly 14 per cent of the FTSE All World.

How might schemes address the issues associated with home bias without straying into territory that feels too exotic and risky?

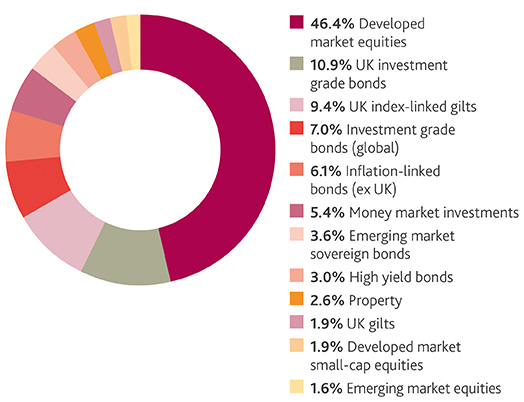

Nest’s 2040 fund asset split

Source: Nest

There are different ways of capturing the risks and rewards of global markets.

Well-managed global equity funds might help overcome objections some trustees may have in selecting a single-country market. For example, the US may look attractive, but the dominance of Apple in driving the growth of US equities could prove uncomfortable for some.

There are also ways of accessing the opportunities while tempering some of the risks in different global regions.

Alternatively weighted indices – often dubbed smart beta – are designed to create more efficient ways of weighting an index.

The broad idea is still to capture long-term growth, but also to reduce the risk of investing so much in the largest companies as measured by market capitalisation.

Nest has begun investing in smart beta in the emerging market allocations within its default range of 47 retirement date funds. In these we included one fund that weights companies in proportion to what they add to the economy.

In my view, with the various ways of accessing global growth available to trustees today, scheme members ought not to be exposed to the risks associated with home bias and poor diversification unless there is good reason.

Mark Fawcett is chief investment officer at Nest