The Pensions Regulator has bared its teeth to the pensions industry, citing the unacceptable scale of underperformance in small pension schemes, highlighting why they must improve or leave the market to protect savers.

I agree and, though I doubt this will be a universally welcome view, the core problem is that too much of the pensions industry serves its own interests rather than the interests of consumers.

Businesses that stay relevant and competitive are generally ruthlessly focused on what is right for the customer.

In this respect, some sections of the pensions industry have failed. How often do we stop and ask the hardest question: is this really the right thing for the member?

As consultants and pension scheme managers realised their defined benefit-centric world would dissolve, many made opportunistic forays into defined contribution.

A lot of those DC plans are now in the sights of TPR, whose intervention is both overdue and welcome.

The UK needs more similarly objective people who are bold enough to ask the tough question.

Lessons from Australia

DB gave way to DC in Australia wholesale nearly 20 years ago. The pension consulting and actuarial profession there, in the way we understand it in the UK, simply vanished.

Internal pension management teams within large corporates disappeared, and large ‘super’ schemes with homogeneous levels of contributions made pensions straightforward for employers and members.

Similarities with what is happening here are inescapable.

The Australian regulator started to raise the compliance and governance bar in order to regulate a smaller number of larger, better-managed plans.

There was simply no reason for an employer to ‘own’ its own scheme, or have its own internal pensions team, with smaller independent funds and corporate funds ‘merged’ into larger plans.

There are powerful yet conflicted forces at play in our own mastertrust market.

Where is the incentive for actuaries, consultants, auditors, independent trustees or pension managers to say their members will most likely be better off in one of the UK’s big mastertrusts’?

Having said this, TPR’s references to underperformance seem to be benchmarked to its own regulatory standards and not to actual outcomes achieved for members. Perhaps we can fill in some gaps.

Does good governance lead to better outcomes?

There is empirical evidence to support assertions that larger, well-governed pension schemes outperform.

Indeed, Keith Ambachtsheer, Canadian academic and co-founder of CEM Benchmarking, looked directly at the relationship between good governance and investment outcomes in two studies, in 1997 and 2008.

The 2008 study was based on responses from a group of 88 senior pension fund executives from some of the world’s top pension funds.

They and their organisations were analysed based on a number of important governance indicators. The results were cross-referenced to corresponding performance data in the CEM Benchmarking database.

Both studies suggested a widespread board competency problem. They also found ‘a positive correlation between governance quality and fund performance’ – better-governed plans produced higher net value-added.

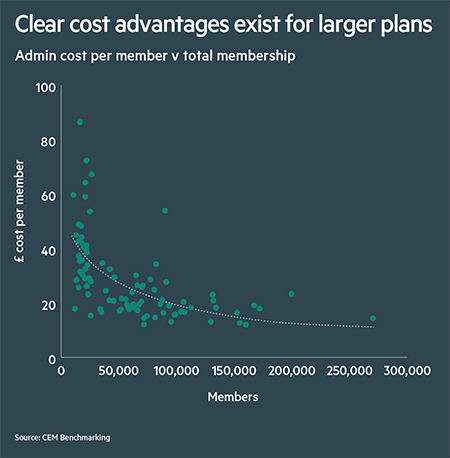

The CEM database, which includes an international universe of funds between £500m and £500bn, tells us that, on average, larger funds outperform.

There are two key reasons for this: asset mix and cost.

Larger funds tend to implement their strategies in a more cost-effective manner, and what they save flows straight through to performance.

Similarly, when it comes to serving members, there are clear cost advantages for larger plans.

Economies of scale

There is, of course, no right answer to minimum size, and large funds can certainly underperform, but DB funds get into a ‘maximum efficiency’ zone at around £50bn assets or 500,000 members.

This is true both in terms of investment outcomes and member service.

I recall meeting with the chief executive officer of an Australian super fund that had over 300,000 members. He explained that his board had just decided to ‘fold’ into another fund with over 1m members.

He said: “We just don’t have the scale needed to serve the members properly”.

Delivering value to members is about more than scheme costs

Low costs and charges alone do not guarantee good value for members’ pension savings, according to research by the Pensions Policy Institute. Read more.

Ultimately, his leadership team was able to put aside personal interests and focus on what it believed was right for the members.

The UK needs more similarly objective people who are bold enough to ask the tough question.

John Simmonds is client relationship manager at CEM Benchmarking