Kingfisher Pension Scheme is planning to review member outcomes as it looks to make sure its default fund fits with the greater at-retirement flexibility opened up by the Budget.

The retailer’s default fund is currently under review as part of the £2.4bn scheme’s defined contribution governance cycle.

However, changes brought in by this year’s Budget – reducing the tax hit on savings taken as a lump sum and increasing the amount that can be taken as drawdown – have increased options for members, says Matt Fuller, investment manager at the scheme.

“We need to factor those changes into our thinking, recognising that fewer people will purchase annuities. At the top end they may prefer to consider drawdown, and at the lower end more will be able to take 100 per cent cash if they wish to do so,” says Fuller.

At the heart of deciding the structure of the default will be understanding what the majority of the scheme’s members want to do, and providing solutions which allow them to use any of the three options, says Fuller.

At the heart of deciding the structure of the default will be understanding what the majority of the scheme’s members want to do, and providing solutions which allow them to use any of the three options, says Fuller.

To do this it will be important to identify what each member is likely to achieve, as the majority of the scheme’s members are relatively low earners that are contributing the minimum required under auto-enrolment, he says.

For The Specialist full report on DC investment, click here for the PDF.

“On the member data side of things, we know how much each of our members is saving and the size of pots they have, so can use that data to help inform our decision making,” says Fuller.

Staying on-risk

At the dispatch box in March, chancellor George Osborne announced an increase in the trivial commutation levels, enabling members to take small pension pots worth up to £10,000 as a lump sum at retirement, up from £2,000, for up to three pension schemes.

Aside from the 25 per cent tax-free lump sum, from April of next year members that fully withdraw from DC at retirement will also be taxed at marginal income rates rather than the current 55 per cent.

As a result, traditional lifestyle strategies that derisk into gilts and cash either 10 or 20 years from retirement are no longer fit for purpose, industry experts say.

Some providers, including Legal & General Investment Management, Axa Life Invest and Friends Life, are responding by designing products that retain greater risk as a member approaches retirement.

Lifestyle make-up

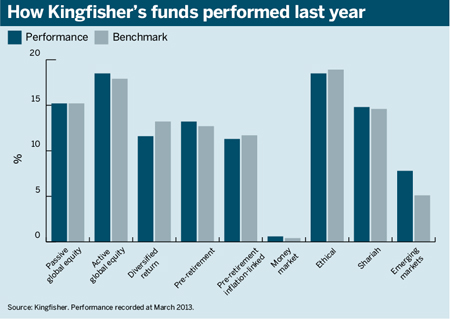

Members of the Kingfisher scheme are currently defaulted into the 10-year lifestyle option, which is invested equally in passive global equities and a diversified return fund at March 31 2013, according to its 2013 annual report.

The diversified return fund passively invests in a wide-range of assets including high-yield bonds, property, commodities and specialised alternative assets, according to the report.

The fund starts to derisk 10 years out from retirement, investing 75 per cent in gilts and UK corporate bonds, and the remainder in money market funds.

The company matches employee contributions up to 6 per cent, and will contribute 10 per cent if members pay in 7 per cent, and 14 per cent for 8 per cent member contributions.

For The Specialist full report on DC investment, click here for the PDF.

Members also have the choice to invest in two other five-year lifestyle funds, one of which has a cash target and invests completely in money market funds during the pre-retirement phase.

The scheme’s self-select funds include an active equity fund, an emerging markets fund and an ethical fund. However, more than 90 per cent of members are invested in the default fund, according to Fuller.

Laith Khalaf, head of corporate research at Hargreaves Lansdown, says: “The lifestyling strategies are out of the window because they’re based on people buying an annuity.”

The difficulty with default funds is there are lots of people who will want different outcomes, says Khalaf.

“We actually think the default setting is to derisk them into cash,” says Khalaf. “I think whatever the default, there are going to be risks involved in it and cash is probably the most material choice and carries the least risk.”

While derisking into cash carries inflation risk, investing in gilts is susceptible to inflation and interest rate fluctuations, adds Khalaf.

The 10-year lifestyle has always been the most popular option at Kingfisher, and formally became the default when the company staged for auto-enrolment in March 2013.

However, its asset allocation changed in 2009 with the introduction of the diversified return fund, says Fuller.

“The committee felt that members needed exposure to equities during the growth phase but also wanted to provide exposure to other asset classes and reduce some of the volatility,” he says. “Hence the 50 per cent allocation to the passive equity fund and a 50 per cent allocation to the diversified return fund.”

Ryan Taylor, senior DC investment consultant at Aon Hewitt, says his team has begun looking at the member make-up of scheme clients to assess the size of the pots they will be likely to achieve.

“The other thing that we would suggest is that they maintain the default they have got in place, introduce the alternative options and see what members want,” says Taylor.

“And if they see a much greater opt-in with one of the alternative options they can review and make that the default.”